Understanding what constitutes “income” in the eyes of the Internal Revenue Service (IRS) is the cornerstone of effective personal finance and tax planning. For many, income is simply the number printed on a bi-weekly paycheck. However, the legal definition of taxable income is far broader, encompassing almost everything of value you receive throughout the year. As the digital economy evolves and side hustles become the norm, the lines between hobbies, gifts, and taxable earnings have blurred.

In the world of money management, failing to accurately identify taxable income can lead to more than just a surprise bill in April; it can result in audits, penalties, and missed opportunities for legal tax avoidance. This guide breaks down the various categories of income, from traditional wages to the complexities of digital assets and bartering.

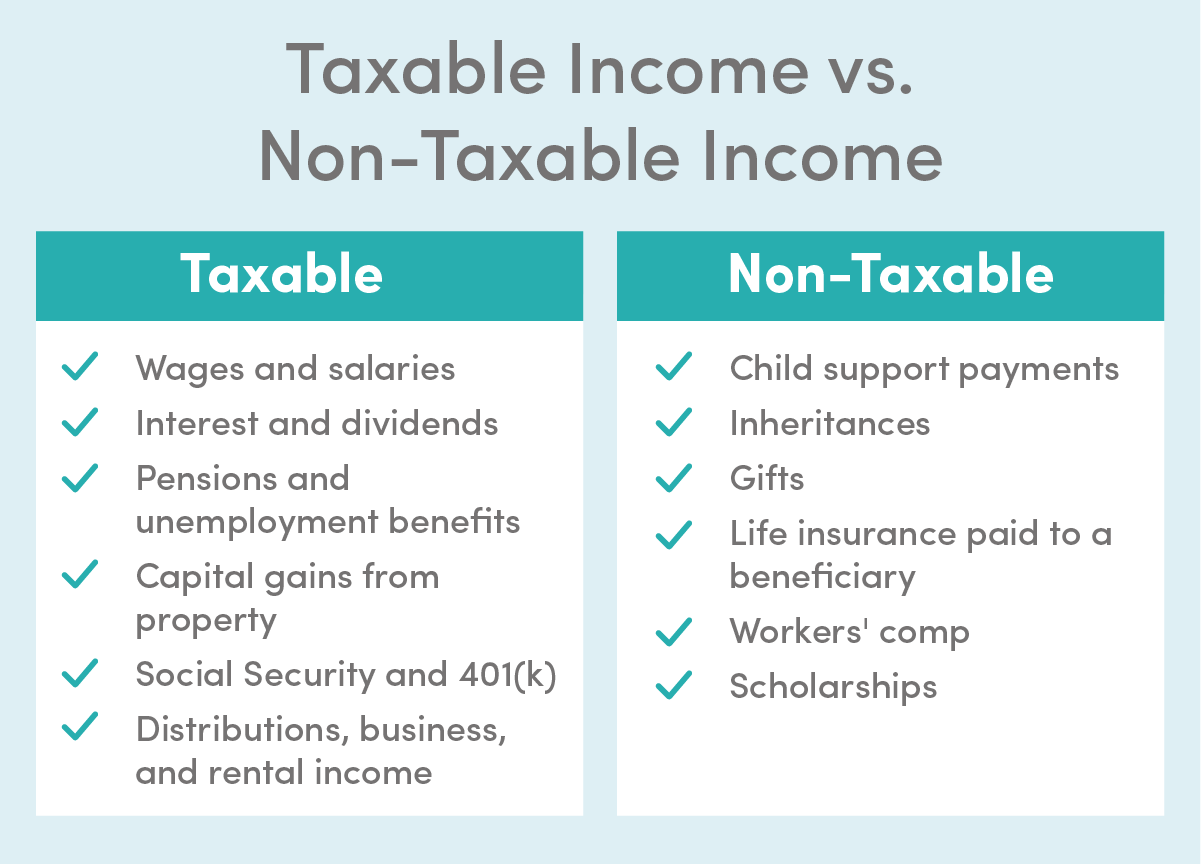

The Broad Definition of Gross Income

The IRS operates under a foundational principle: all income is taxable unless specifically excluded by law. This “Gross Income” is the starting point for calculating your tax liability. It is not limited to cash; it includes money, property, and services.

Earned Income: Wages, Salaries, and Tips

For the majority of Americans, earned income is the primary source of wealth. This includes your base salary, hourly wages, and any overtime pay. However, it also extends to bonuses, commissions, and tips. Many service-industry workers mistakenly believe that cash tips are “off the record,” but the IRS requires all gratuities to be reported. If you receive a year-end bonus or a performance-based commission, these are treated as supplemental wages and are subject to withholding, though often at a different flat rate than your standard pay.

Self-Employment and Freelance Earnings

The rise of the “solopreneur” has changed the landscape of taxable income. If you operate as a freelancer, independent contractor, or small business owner, your income is not just what you “take home,” but the total gross receipts of your business. Because there is no employer to withhold taxes on your behalf, you are responsible for paying both the employer and employee portions of Social Security and Medicare taxes, commonly known as the self-employment tax. This applies even if your business is a side hustle performed in the evenings.

Fringe Benefits and Non-Cash Compensation

Sometimes, income isn’t paid in dollars. If your employer provides you with a company car for personal use, pays for your gym membership, or gives you a vacation package as a reward, the fair market value of these benefits may be considered taxable income. While many employer-provided benefits like health insurance are specifically excluded from taxes, “fringe benefits” that are not explicitly exempt must be added to your total gross income.

Investment and Passive Income Streams

In the pursuit of financial independence, many individuals turn to investments to grow their wealth. While these streams are “passive,” they are very much active in the eyes of the tax authorities.

Interest and Dividends

Money sitting in a high-yield savings account or a Certificate of Deposit (CD) generates interest. This interest is generally taxable as ordinary income. Similarly, if you own stocks or mutual funds that pay dividends, that money is considered income. Dividends are categorized as either “qualified” or “ordinary.” Qualified dividends are taxed at the lower capital gains rates, while ordinary dividends are taxed at your standard income tax bracket. Understanding this distinction is vital for long-term portfolio strategy.

Capital Gains from Property and Assets

When you sell an asset—be it a stock, a piece of real estate, or a vintage collectible—for more than you paid for it, the profit is considered a capital gain. The IRS distinguishes between short-term gains (assets held for one year or less) and long-term gains (assets held for more than a year). Short-term gains are taxed at higher ordinary income rates, whereas long-term gains enjoy preferential lower rates. This creates a significant incentive for investors to adopt a “buy and hold” strategy to minimize their tax burden.

Rental Income and Royalties

If you own a rental property, the rent you receive is taxable income. However, this is one of the most complex areas of tax law because you can deduct various expenses—such as mortgage interest, property taxes, and depreciation—against that income. Royalties, which are payments received for the use of your intellectual property (like a book, a patent, or a song), are also taxable and are typically reported on Schedule E of your tax return.

Modern Income Sources: Digital Assets and Side Hustles

As technology reshapes how we trade value, the IRS has tightened its grip on modern income streams that were once considered “under the radar.”

Cryptocurrency and Virtual Currency Transactions

The IRS treats cryptocurrency as property, not currency. This means that every time you trade one coin for another, sell crypto for USD, or use Bitcoin to buy a cup of coffee, you have triggered a taxable event. If the value of the coin increased from the time you acquired it to the time you spent or traded it, you owe capital gains tax. Furthermore, if you are “mining” or “staking” cryptocurrency, the fair market value of the coins at the time they are earned is considered ordinary income.

The Gig Economy and Platform-Based Earnings

Whether you are driving for a ride-share service, delivering groceries, or selling handmade crafts on a digital marketplace, those earnings are taxable. Many platforms are now required to issue Form 1099-K to users who exceed certain transaction thresholds. However, even if you do not receive a form, you are legally required to report every dollar earned. The benefit here is that gig workers can often deduct business-related expenses, such as mileage or home office costs, to reduce their taxable total.

Often Overlooked and Miscellaneous Taxable Income

There are several sources of money that taxpayers frequently forget to report, often because the payment feels like a windfall or a government benefit rather than “work.”

Unemployment Benefits and Jury Duty Pay

It is a common misconception that government assistance is tax-free. Unemployment compensation is, in fact, taxable at the federal level. While some states exempt it from state taxes, the IRS expects its share. Similarly, if you are paid for jury duty, that money is considered income. If you are required to hand that jury pay over to your employer because they continued to pay your salary, you can usually deduct that amount from your gross income so you aren’t taxed on money you didn’t keep.

Prizes, Awards, and Gambling Winnings

If you win a car on a game show, a lottery jackpot, or $500 at a casino, the IRS considers that income. The “fair market value” of physical prizes must be reported as “Other Income.” For gambling, you are required to report all winnings, though you may be able to deduct gambling losses up to the amount of your winnings if you itemize your deductions.

Bartering and Non-Cash Exchanges

Bartering occurs when you exchange services or goods without the use of money. For example, if a web designer creates a site for a mechanic in exchange for car repairs, both parties have received “income” equal to the fair market value of the services received. While difficult for the IRS to track, it is legally required to be reported, especially when conducted through a formal bartering exchange.

What Is Generally Not Considered Taxable Income?

To manage your finances effectively, it is just as important to know what the IRS cannot touch. Certain inflows of wealth are protected by law to encourage specific social or economic behaviors.

Gifts and Inheritances

In most cases, if someone gives you money or you inherit an estate, it is not considered taxable income to the recipient. The donor may be responsible for a gift tax if the amount exceeds an annual threshold, but the person receiving the gift generally owes nothing. This allows for the tax-free transfer of wealth between generations.

Child Support and Life Insurance Proceeds

Payments received for child support are not taxable to the recipient (and are not deductible by the payer). This ensures the full amount of the support goes toward the child’s needs. Additionally, money received from a life insurance policy upon the death of the insured person is typically tax-exempt, providing a crucial safety net for grieving families without the added burden of a tax bill.

Scholarships and Grants

If you receive a scholarship or grant for higher education, the portion used for tuition, fees, books, and required equipment is generally tax-free. However, any portion of the funds used for room and board or incidental expenses is considered taxable income.

Strategies for Managing Tax Liability

Understanding what is income is only the first step. The second step is learning how to protect your wealth through legal deductions and strategic planning.

Deductions and Credits

The difference between your “Gross Income” and your “Adjustable Gross Income” (AGI) is determined by deductions. Contributions to traditional 401(k)s or IRAs, student loan interest, and certain business expenses can lower your AGI. Furthermore, tax credits—such as the Earned Income Tax Credit (EITC) or Child Tax Credit—provide a dollar-for-dollar reduction of your actual tax bill, which is even more valuable than a deduction.

Record-Keeping Best Practices

In the world of personal finance, documentation is your best defense. Whether you are tracking mileage for a side hustle, saving receipts for a home office, or logging cryptocurrency trades, maintaining meticulous records ensures that you only pay what you owe. Utilizing financial tools and apps to categorize income as it arrives can prevent a chaotic scramble during tax season and provide a clearer picture of your overall financial health.

By viewing “income” through the lens of the IRS, you can navigate your financial life with greater confidence. Whether you are climbing the corporate ladder, building a portfolio of dividend stocks, or navigating the volatile world of digital assets, knowing the tax implications of every dollar is the hallmark of a savvy financial mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.