In the dynamic world of finance, few concepts hold as much power and intrigue as compounding. It’s often referred to as the “eighth wonder of the world” for its ability to generate wealth over time. While most people are familiar with interest being compounded annually, semi-annually, quarterly, or monthly, a less intuitive yet profoundly significant form exists: continuous compounding. This advanced financial concept represents the theoretical maximum limit of how frequently interest can be calculated and added to an investment or loan. Understanding it is crucial for anyone seeking a deeper insight into investment growth, loan obligations, and sophisticated financial modeling.

Continuous compounding is not just an academic exercise; it underpins various financial theories and derivative pricing models. It describes a scenario where interest is calculated and reinvested infinitely many times over a given period, rather than a discrete number of times. While purely theoretical in its absolute form, it provides a powerful benchmark and a robust framework for understanding the relentless growth potential of capital. This article will demystify continuous compounding, exploring its mechanics, its mathematical foundations, its implications for personal finance and investing, and how it compares to more conventional compounding frequencies.

The Foundation of Growth: Understanding Compounding

Before diving into the specifics of continuous compounding, it’s essential to grasp the fundamental principle of compounding itself. At its core, compounding is the process of earning returns on previously accumulated returns. It’s the snowball effect for your money. Instead of just earning interest on your initial principal, you start earning interest on your principal plus any accumulated interest from previous periods.

Simple vs. Compound Interest

To appreciate the power of compounding, let’s briefly differentiate it from simple interest. Simple interest is calculated only on the original principal amount. If you invest $1,000 at a 5% simple interest rate for five years, you earn $50 per year, totaling $250 over five years. The principal remains $1,000 for each calculation.

Compound interest, however, changes the game. With compound interest, that $50 earned in the first year is added to your principal, making your new principal $1,050 for the second year. In the second year, you earn 5% of $1,050, which is $52.50. This amount is then added, and the process continues. This seemingly small difference creates a significant divergence in wealth accumulation over time. The more frequently interest is compounded, the faster your money grows, because you’re earning interest on a larger and larger base.

The Impact of Compounding Frequency

The frequency with which interest is compounded dramatically affects the total return. Imagine an investment with an annual interest rate of 5%.

- Annually: Interest is calculated once a year.

- Semi-annually: Interest is calculated twice a year (e.g., 2.5% every six months).

- Quarterly: Interest is calculated four times a year (e.g., 1.25% every three months).

- Monthly: Interest is calculated twelve times a year.

- Daily: Interest is calculated 365 times a year.

As the compounding frequency increases, the effective annual rate (EAR) — the actual annual rate of return an investment earns — also increases, albeit at a diminishing rate. This phenomenon sets the stage for continuous compounding, which explores the ultimate limit of this frequency.

The Mechanics of Continuous Compounding

Continuous compounding represents the theoretical maximum where interest is compounded an infinite number of times over a given period. Instead of discrete intervals like days or hours, the interest is constantly being calculated and added to the principal. This concept is deeply rooted in calculus and the properties of a special mathematical constant known as Euler’s number.

Introducing Euler’s Number (e)

Central to understanding continuous compounding is the mathematical constant e, an irrational number approximately equal to 2.71828. e naturally arises in situations involving continuous growth or decay, from population dynamics to radioactive decay, and, crucially, in finance. In the context of compounding, e emerges when we consider what happens as the number of compounding periods approaches infinity.

Let’s look at the general compound interest formula:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

As n (the number of compounding periods per year) approaches infinity, the expression (1 + r/n)^(nt) approaches e^(rt). This mathematical limit is what defines continuous compounding.

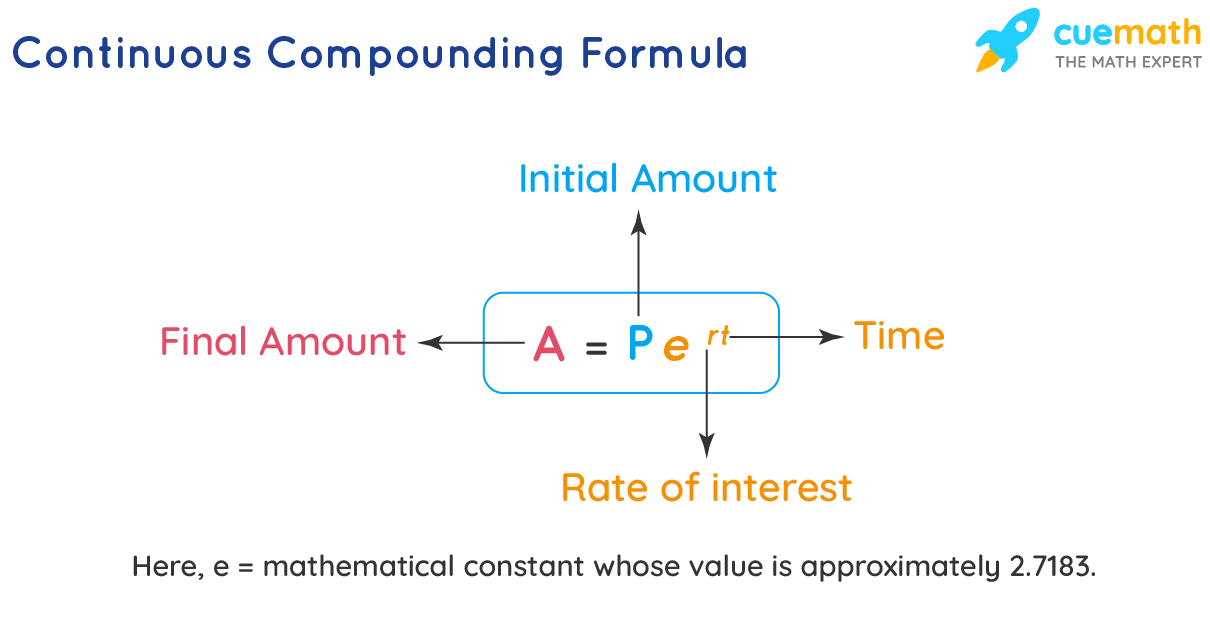

The Continuous Compounding Formula Explained

Given the derivation above, the formula for continuous compounding simplifies to:

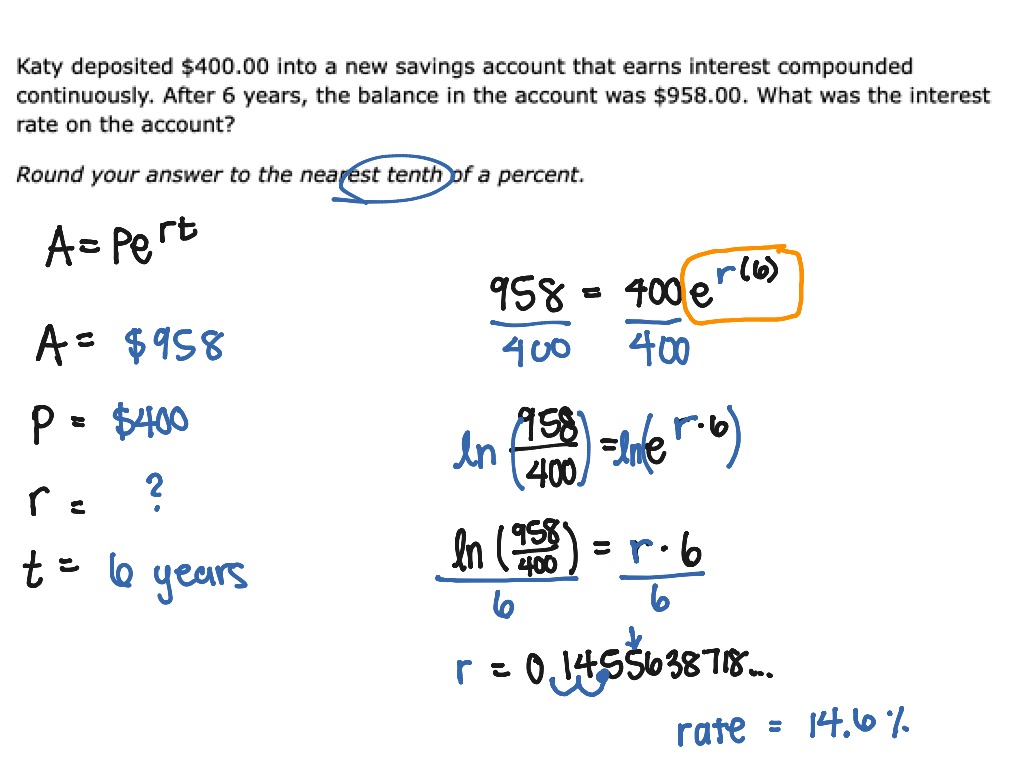

A = Pe^(rt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount

- e = Euler’s number (approximately 2.71828)

- r = the annual interest rate (as a decimal)

- t = the number of years the money is invested or borrowed for

This elegant formula allows us to calculate the maximum possible future value for a given principal, rate, and time, assuming the most frequent compounding possible. It’s a powerful tool for financial analysis because it provides an upper bound for investment growth and loan interest accumulation.

Why Continuous Compounding Matters in Finance

While actual financial products rarely compound truly continuously in practice (daily compounding is often the practical limit), the concept of continuous compounding holds immense theoretical and practical importance across various facets of finance.

Benchmarking and Effective Annual Rate (EAR)

For investors, continuous compounding provides a benchmark for the maximum theoretical return. When evaluating different investment opportunities, understanding the maximum possible growth helps in assessing the relative attractiveness of an offer. If an investment offers a high nominal annual rate but compounds infrequently, its true EAR might be lower than another investment with a slightly lower nominal rate but higher compounding frequency. Continuous compounding sets the absolute ceiling for the EAR for a given stated annual rate. The Effective Annual Rate for continuous compounding is calculated as EAR = e^r – 1. This allows for a direct comparison across different compounding conventions.

Derivatives and Valuation Models

Perhaps the most significant application of continuous compounding is in the world of advanced finance, particularly in derivative pricing models. Models like the Black-Scholes formula for options valuation heavily rely on continuous compounding because it simplifies the mathematics of stochastic processes that describe asset price movements. These models assume that asset prices change continuously over time, and interest rates, dividends, and other factors are also compounded continuously.

- Options Pricing: The Black-Scholes model, for instance, uses the continuously compounded risk-free rate to discount future cash flows. This assumption allows for the modeling of price changes over infinitesimally small time intervals, which is crucial for accurately pricing complex financial instruments.

- Futures Contracts: Pricing futures contracts often involves considering the cost of carry, which can be modeled using continuously compounded interest rates.

- Bond Valuation: While bonds typically pay interest discretely, continuous compounding can be used in some theoretical models for valuing bonds or interest rate swaps, especially when considering the continuous accumulation of interest over various periods.

Risk-Free Rate and Theoretical Calculations

In financial theory, the “risk-free rate” (the return on an investment with zero risk, often approximated by government bonds) is frequently discussed in terms of continuous compounding. This allows financial professionals to compare returns and discount future cash flows on an equivalent basis, stripping away the complexities of different compounding conventions. When discussing expected returns or the cost of capital, stating rates in continuously compounded terms simplifies calculations and ensures consistency in theoretical models.

Comparing Continuous Compounding to Other Frequencies

Understanding how continuous compounding stacks up against more common discrete compounding frequencies is key to appreciating its implications. While continuous compounding yields the highest future value for a given rate and time, the difference often becomes marginally smaller as compounding frequency increases.

Marginal Gains and Diminishing Returns

Let’s consider an example: an initial investment of $1,000 at an annual interest rate of 5% over 10 years.

- Annually (n=1): A = 1000 * (1 + 0.05/1)^(1*10) = $1,628.89

- Semi-annually (n=2): A = 1000 * (1 + 0.05/2)^(2*10) = $1,638.62

- Quarterly (n=4): A = 1000 * (1 + 0.05/4)^(4*10) = $1,643.62

- Monthly (n=12): A = 1000 * (1 + 0.05/12)^(12*10) = $1,647.01

- Daily (n=365): A = 1000 * (1 + 0.05/365)^(365*10) = $1,648.66

- Continuously (n→∞): A = 1000 * e^(0.05*10) = $1,648.72

As you can see, the difference between daily compounding and continuous compounding is minimal ($1,648.66 vs. $1,648.72). The largest jumps in future value occur when moving from annual to semi-annual, or semi-annual to quarterly. As the frequency becomes very high (e.g., daily), the additional gains from further increases in frequency become incrementally smaller. This illustrates the concept of diminishing returns in compounding frequency. The “power” of continuous compounding is less about vastly superior returns in everyday accounts and more about providing a theoretical maximum and simplifying complex financial models.

Implications for Loans and Debt

While beneficial for investors, continuous compounding can be less favorable for borrowers. If a loan were compounded continuously, it would accumulate interest at the fastest possible rate, leading to the highest potential repayment amount. Fortunately for consumers, most loans (mortgages, car loans, credit cards) compound interest on a discrete basis, typically monthly or daily. However, understanding the theoretical maximum interest accumulation provided by continuous compounding can highlight the importance of paying down high-interest debt quickly to mitigate the exponential growth of interest.

Conclusion

Continuous compounding is a profound concept in finance that represents the theoretical limit of interest accumulation. While rarely encountered as a literal practice in everyday banking, its mathematical elegance and predictive power make it indispensable in advanced financial modeling, particularly in the valuation of derivatives and complex securities. By understanding Euler’s number and the formula A = Pe^(rt), individuals gain a deeper appreciation for the mechanics of growth in financial markets.

For personal investors, continuous compounding serves as a valuable benchmark, illustrating the maximum potential growth of an investment and highlighting the diminishing marginal returns of increasing compounding frequency beyond a certain point. For financial professionals, it’s a cornerstone for theoretical models that underpin much of modern financial engineering. Ultimately, “what is compounded continuously?” leads us to a fascinating intersection of mathematics and money, revealing the ultimate power of time, rate, and frequency in wealth creation and financial analysis.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.