In the realm of personal finance, few concepts hold as much transformative power as compound interest. Often referred to as the “eighth wonder of the world” by Albert Einstein, compound interest is the engine that drives modern wealth creation. Whether you are saving for retirement, investing in the stock market, or simply trying to understand how your savings account grows, mastering this concept is essential for financial literacy.

At its core, compound interest is the interest calculated on the initial principal, which also includes all of the accumulated interest from previous periods on a deposit or loan. While simple interest is calculated only on the principal amount, compound interest grows at an accelerated rate because it builds upon itself. This article explores the mechanics of compound interest, the variables that influence its growth, and how you can harness its power to achieve financial independence.

The Mechanics of Growth: How Compound Interest Functions

Understanding how compound interest works requires a shift from linear thinking to exponential thinking. Most people are accustomed to simple arithmetic where 1 + 1 equals 2. In the world of compounding, however, your money does not just add up; it multiplies.

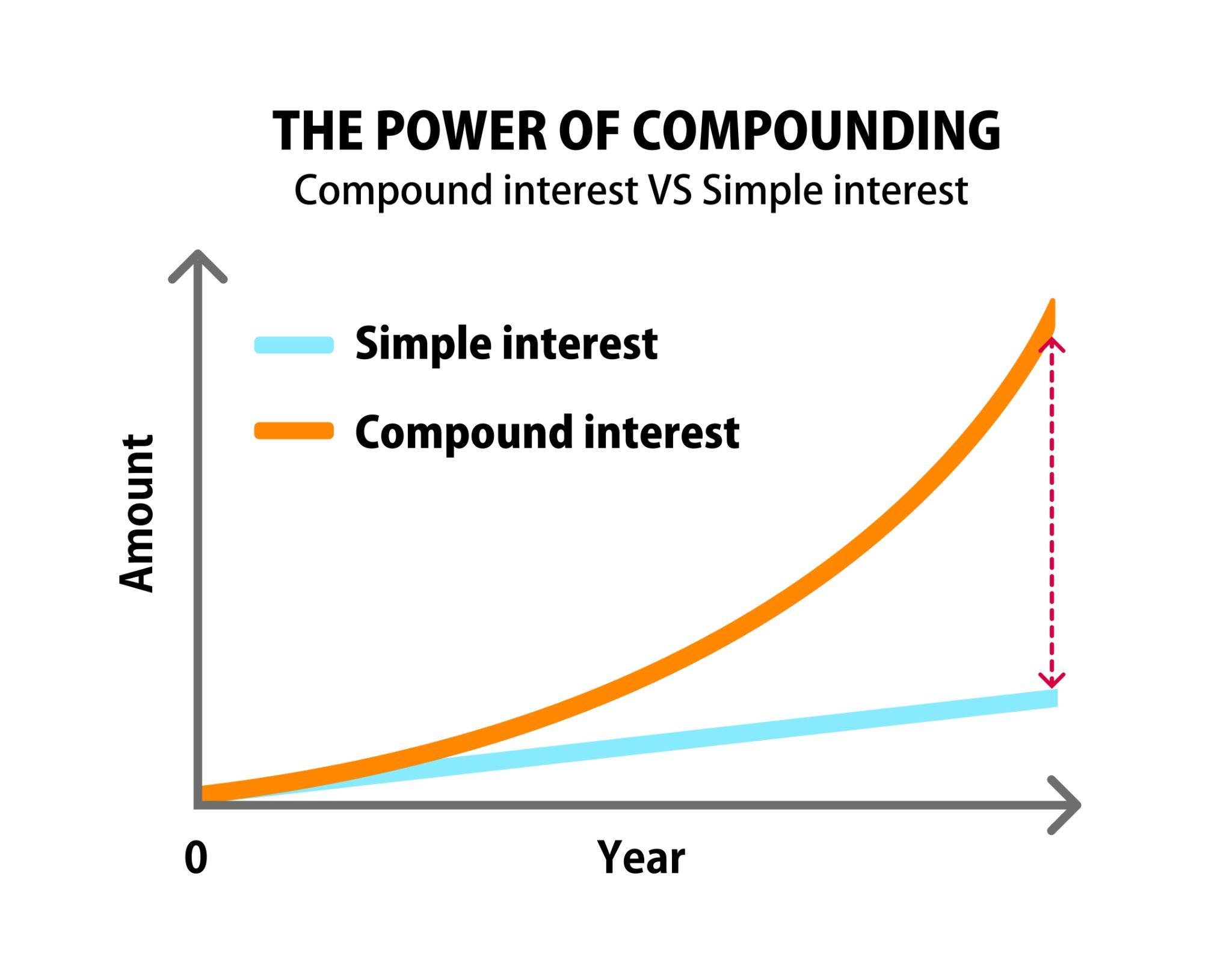

The Difference Between Simple and Compound Interest

To appreciate compound interest, one must first understand simple interest. Simple interest is determined by multiplying the daily interest rate by the principal by the number of days that elapse between payments. For example, if you invest $1,000 at a 5% simple interest rate for three years, you would earn $50 each year, totaling $150 in interest.

Compound interest, however, reinvests those earnings. In the first year, you earn $50, bringing your total to $1,050. In the second year, the 5% interest is calculated on the new total of $1,050, yielding $52.50. By the third year, you are earning interest on the interest. Over short periods, the difference seems negligible, but over decades, the divergence between simple and compound growth becomes a vast chasm.

The Compound Interest Formula

While modern financial calculators and spreadsheets handle the math for us, understanding the underlying formula provides clarity on how wealth is generated. The standard formula for compound interest is:

A = P (1 + r/n)^(nt)

- A = the future value of the investment/loan, including interest.

- P = the principal investment amount (the initial deposit).

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per unit t.

- t = the time the money is invested or borrowed for.

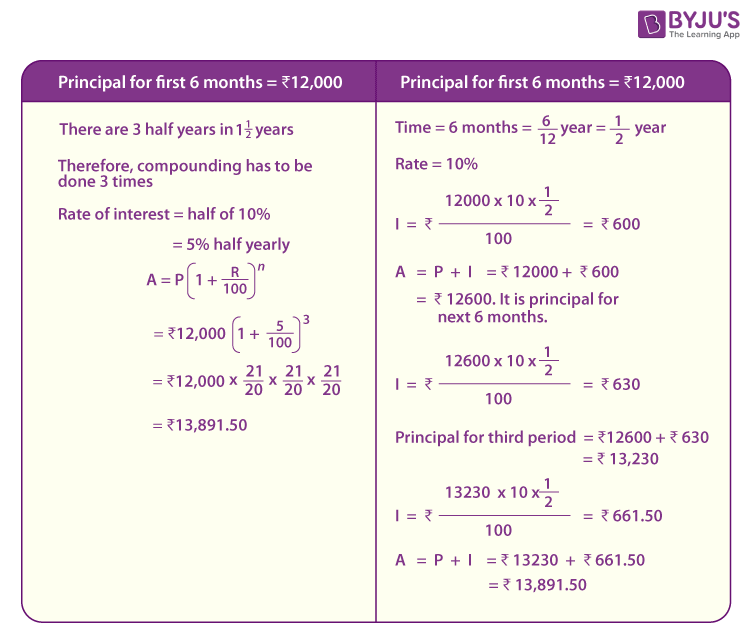

The Impact of Compounding Frequency

The frequency with which interest is compounded—daily, monthly, quarterly, or annually—has a significant impact on the final balance. The more frequently interest is added to the principal, the faster the total grows. For instance, a savings account that compounds daily will yield a slightly higher return than one that compounds annually, even if the annual percentage yield (APY) is the same. This is because the interest earned today starts earning its own interest tomorrow.

The Vital Variables: Time, Rate, and Consistency

The magic of compounding does not happen overnight. It is a slow-burn process that requires specific conditions to reach its full potential. There are three primary levers you can pull to increase your wealth: the amount of time you stay invested, the rate of return you achieve, and the consistency of your contributions.

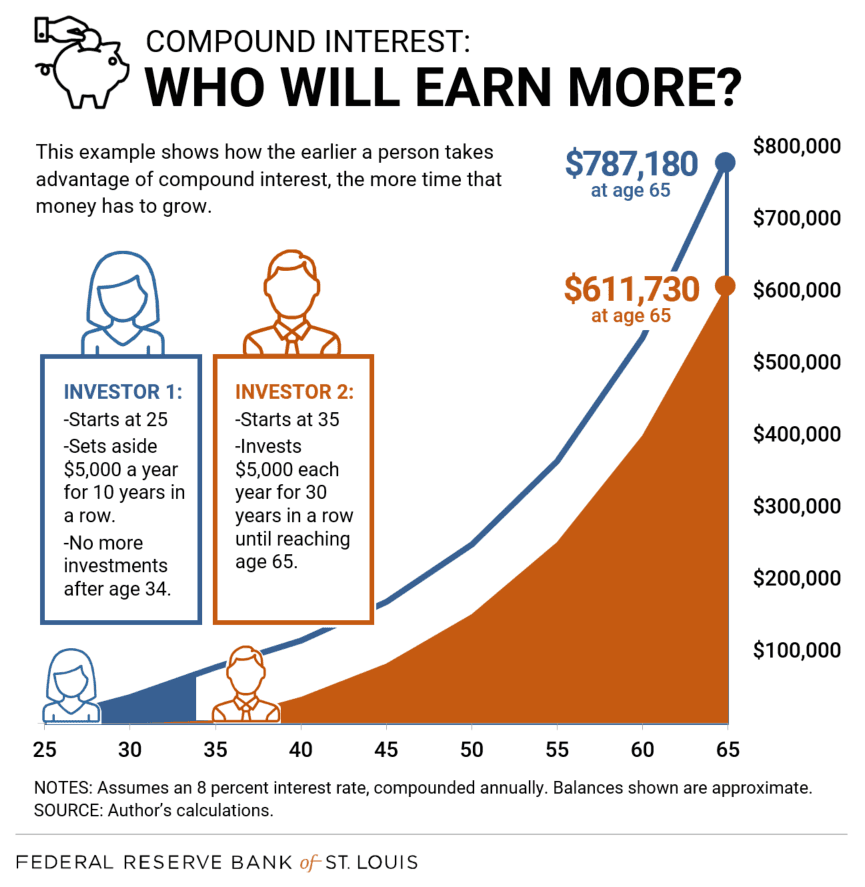

The “Time” Factor: Why Starting Early is Everything

Time is the most critical ingredient in the compounding recipe. Because the growth is exponential, the most significant gains occur in the final years of the investment period. This leads to a phenomenon where an individual who starts investing small amounts in their 20s can easily outperform someone who invests much larger amounts starting in their 40s.

Consider two investors: Susan starts investing $200 a month at age 25, while David starts investing $500 a month at age 45. Even though David is contributing more than double the amount monthly, Susan’s 20-year head start gives her money more time to compound. By age 65, Susan will likely have a significantly larger portfolio than David, despite having contributed less total principal.

Understanding the Rule of 72

A professional and quick way to estimate the power of compounding is the “Rule of 72.” This is a simplified formula used to determine how many years it will take for an investment to double, given a fixed annual rate of interest. By dividing 72 by the annual rate of return, investors can get a rough estimate of their money’s growth timeline. For example, at a 6% return, your money will double every 12 years (72 / 6 = 12). If you can increase that return to 9%, your money doubles every 8 years.

The Power of Consistent Contributions

While the initial principal is important, the “turbocharger” for compound interest is regular, consistent contributions. By adding to your investment portfolio monthly or yearly, you are increasing the base upon which the interest is calculated. This creates a dual-layered growth effect: your existing money is compounding, and your new money is entering the cycle to begin its own compounding journey.

Practical Applications in Personal Finance and Investing

Compound interest is not just a theoretical concept; it is the foundation of almost every financial product on the market. From the debt we owe to the assets we build, compounding is always at work.

Retirement Accounts and Wealth Building

Vehicles such as the 401(k), 403(b), and Individual Retirement Accounts (IRAs) are designed specifically to take advantage of long-term compounding. When these accounts are paired with tax-advantaged status—meaning your investments grow tax-deferred or tax-free—the compounding effect is even more pronounced. Without the “drag” of annual taxes on gains, 100% of your earnings stay in the account to generate more wealth.

Dividend Reinvestment Plans (DRIPs)

In the stock market, compound interest often manifests through dividends. When a company pays a portion of its profits to shareholders, savvy investors use a Dividend Reinvestment Plan (DRIP) to automatically use those payouts to buy more shares. Over time, you own more shares, which pay more dividends, which buy even more shares. This is compounding in its most physical form within an investment portfolio.

The Dark Side: Compound Interest in Debt

It is vital to recognize that compound interest is a double-edged sword. While it builds wealth for savers, it can destroy financial stability for borrowers. Credit cards are the most common example of compound interest working against the consumer. Most credit card companies compound interest daily. If you carry a balance, you are paying interest on the interest from the previous day. This is why credit card debt can feel impossible to escape; the “snowball” is rolling downhill toward you rather than away from you.

Strategies to Maximize the Compounding Effect

To truly leverage compound interest, one must move beyond understanding and into strategic action. Maximizing these returns requires discipline and a long-term perspective.

Automating the Process

The greatest enemy of compound interest is human inconsistency. To combat this, financial professionals recommend automating your savings and investments. By setting up automatic transfers from your paycheck to your brokerage or savings account, you ensure that the compounding process never stops. Automation removes the emotional temptation to “skip a month,” which can have a massive negative impact on the long-term total.

Minimizing Fees and Expenses

In the world of investing, what you pay in fees is money that is not compounding for you. High-expense-ratio mutual funds or excessive management fees act as “negative compounding.” A 1% fee might seem small, but over 30 years, it can eat away nearly a third of your potential wealth. Opting for low-cost index funds or ETFs ensures that the lion’s share of the compounding returns stays in your pocket.

Patience and the Avoidance of Interference

The hardest part of compound interest is doing nothing. The “boring” middle years of an investment journey—where the growth is steady but not yet explosive—are when many people make the mistake of withdrawing funds or changing strategies. To see the vertical part of the exponential curve, you must leave the principal and the interest untouched. Every time you withdraw money, you “reset” the compounding clock on those dollars, losing the future gains they would have generated.

Conclusion: Embracing the Long View

Compound interest is a testament to the rewards of patience and discipline. It is a mathematical certainty that rewards those who start early, stay consistent, and keep their hands off their growing capital. While the initial stages of compounding may seem slow and underwhelming, the long-term results are nothing short of life-changing.

By understanding the mechanics of the formula, recognizing the importance of time, and applying these principles to retirement accounts and debt management, you can position yourself on the right side of the wealth equation. In the landscape of personal finance, you don’t need to be a genius to build wealth; you simply need to understand compound interest and give it the time it needs to work its magic.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.