In the rapidly evolving landscape of personal finance, the lines between traditional banking and digital convenience have blurred significantly. Cash App, owned by Block, Inc., has emerged as one of the most popular financial tools in the United States, boasting millions of active users who utilize the platform for everything from peer-to-peer payments to investing in Bitcoin. However, as users transition from simple transfers to more complex financial activities—such as setting up direct deposits or linking their accounts to external services—a common and vital question arises: “What is the Cash App bank name?”

The answer is not as straightforward as one might expect. Unlike JPMorgan Chase or Bank of America, Cash App is not a bank. Instead, it is a financial technology (fintech) platform that partners with established banking institutions to provide regulated financial services. To manage your money effectively within the Cash App ecosystem, it is essential to understand which banking entities are working behind the scenes.

The Architecture of Neobanking: Why Cash App Isn’t a Bank

To understand the financial identity of Cash App, one must first understand the concept of “neobanking” or “fintech.” Cash App functions as a digital interface—a highly sophisticated wallet that allows you to move money with ease. However, because Cash App does not hold a formal banking charter, it cannot legally provide certain services, such as holding deposits or issuing debit cards, on its own.

The Role of Financial Technology Companies

Cash App is essentially a service layer. Its primary goal is to provide a seamless user experience, intuitive design, and rapid transaction speeds. While you see the green interface and the “$Cashtag,” the actual movement of money through the federal banking system requires a regulated infrastructure. This is where the distinction between a “platform” and a “bank” becomes critical for personal finance management. By delegating the heavy lifting of regulatory compliance and ledger management to traditional banks, fintechs like Cash App can focus on innovation.

How Partner Banking Models Work

The partnership model, often referred to as “Banking as a Service” (BaaS), is the backbone of the modern digital economy. In this arrangement, a traditional bank provides the “back-end” services (like FDIC insurance eligibility and access to the ACH network), while the fintech provider manages the “front-end” (the app interface and customer service). For a Cash App user, this means that while you interact with Block, Inc., your funds are actually housed within a chartered financial institution.

Identifying Your Cash App Bank Name and Account Details

When you need to provide a bank name for a direct deposit form or to link your Cash App account to a third-party app like Mint or Rocket Money, you generally cannot simply write “Cash App.” Depending on the specific service you are using within the app, you may be interacting with one of two primary banking partners.

Sutton Bank vs. Lincoln Savings Bank

Historically, Cash App has utilized two main partners to handle different aspects of its financial offerings:

- Sutton Bank: This institution is the primary issuer of the Cash Card (the Visa debit card linked to your Cash App balance). If a merchant or a service asks for the bank name associated with your debit card, Sutton Bank is the entity responsible for those transactions.

- Lincoln Savings Bank: For many years, Lincoln Savings Bank provided the routing and account numbers for direct deposits. When users set up their paychecks to land in Cash App, they were technically opening a sub-account through Lincoln Savings Bank.

It is important to note that Cash App has recently begun diversifying its partnerships and, in some cases, providing these services through its own internal mechanisms via “Block, Inc.” or other subsidiary entities. However, for the majority of users, the “bank name” required for documentation will be one of these two institutions.

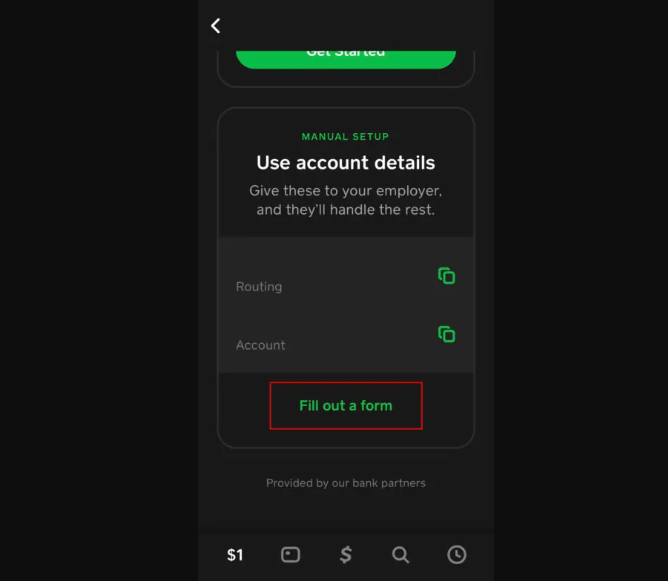

Step-by-Step: Finding Your Routing and Account Numbers

Because Cash App updates its partnerships periodically, the most accurate way to identify your specific bank name is directly through the app.

- Open Cash App and tap the Money tab (the bank icon or dollar amount) on the home screen.

- Tap the Direct Deposit option or the routing/account number display.

- Here, Cash App will explicitly list the routing number and the account number.

- Often, the app will also provide a “Get Bank Name” or “Copy Details” option that will confirm whether you should use Lincoln Savings Bank or another partner for your specific account.

The Financial Security of Your Funds

One of the most significant concerns for users moving their “real-world” money into a digital wallet is security. If Cash App isn’t a bank, is your money safe? In the realm of personal finance, safety is synonymous with FDIC insurance.

FDIC Insurance and Pass-Through Protection

The Federal Deposit Insurance Corporation (FDIC) typically insures deposits up to $250,000 per depositor, per insured bank. Since Cash App isn’t a bank, it doesn’t have FDIC insurance directly. Instead, it offers “pass-through” insurance. This means that when you store money in your Cash App balance, the funds are moved to the partner banks (like Sutton or Lincoln). Once those funds reach the partner bank, they become eligible for FDIC coverage.

However, there is a catch: to be eligible for this insurance, you must have a Cash Card. Without a registered Cash Card, your funds may not be covered by pass-through FDIC insurance in the same way, as the account might be treated as a general pool of funds rather than an individual deposit account.

Managing Risk in a Digital Wallet

While the partner banking model is secure, users must practice “digital hygiene.” Because Cash App transactions are often instantaneous and irreversible, they are frequent targets for scams. From a financial planning perspective, it is wise to treat Cash App as a “transitory” account—a place for spending money and quick transfers—rather than a primary savings vehicle. Keeping the bulk of your emergency fund in a traditional high-yield savings account (HYSA) provides an extra layer of separation and security.

Maximizing Cash App for Personal Finance

Beyond simply knowing the bank name, understanding Cash App’s utility as a financial tool can help you optimize your cash flow and budgeting.

Direct Deposits and Early Paycheck Access

One of the most compelling reasons users seek out the Cash App bank name is to set up direct deposits. Cash App offers a feature where users can receive their paychecks up to two days earlier than they would at a traditional bank. This occurs because Cash App (via its partner banks) credits the funds as soon as the employer initiates the transfer, rather than waiting for the funds to fully settle. For those managing tight monthly budgets, this 48-hour head start can be a powerful tool for avoiding late fees on bills.

Using the Cash Card for Everyday Budgeting

The Cash Card is more than just a piece of plastic; it is a budgeting tool. Through “Cash Boosts,” users can select specific merchants (like Starbucks, DoorDash, or grocery stores) to receive instant discounts. From a personal finance standpoint, this is an immediate return on investment. By knowing that Sutton Bank is the issuer, you can also link your Cash Card to budgeting apps to track your discretionary spending separately from your fixed costs (like rent or mortgage) paid from a traditional checking account.

Navigating Common Financial Questions

As you integrate Cash App into your broader financial strategy, a few practical considerations remain regarding its limitations and capabilities compared to traditional banking.

Can You Use Cash App as Your Primary Bank Account?

While it is possible to use Cash App for the majority of your banking needs—receiving income, paying bills, and spending—it lacks certain features of a “full-service” bank. For example, Cash App does not offer joint accounts, physical checkbooks, or robust wire transfer capabilities. Additionally, while you can deposit paper cash at participating retailers (like Walgreens or 7-Eleven), there is usually a fee involved, which can eat into your savings over time.

Understanding Transfer Limits and Fees

A key part of business and personal finance is managing transaction costs. Cash App is free for standard transfers to a linked bank account (which take 1–3 business days). However, if you need your money immediately, there is an “Instant Transfer” fee (typically 0.5% to 1.75%). Furthermore, unverified accounts have strict weekly sending and receiving limits. To increase these limits, you must provide your full legal name, date of birth, and the last four digits of your Social Security number—information that is then shared with the partner banks to comply with “Know Your Customer” (KYC) laws.

In conclusion, while the “Cash App bank name” might be Sutton Bank or Lincoln Savings Bank depending on the context, the true value lies in understanding the synergy between the app and these institutions. By recognizing how these partnerships work, you can confidently navigate direct deposits, ensure your funds are insured, and leverage the platform’s unique features to improve your overall financial health. Cash App represents a new era of money management—one where the bank is no longer a building on the corner, but a sophisticated network of partners accessible from the palm of your hand.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.