A budget is far more than just a dry spreadsheet filled with numbers; it is a meticulously crafted financial blueprint, a strategic roadmap that guides individuals, families, businesses, and even governments towards their monetary goals. At its core, a budget is an estimation of revenue and expenses over a specified future period. It’s a forward-looking plan designed to ensure that income is sufficient to cover expenditures, with a surplus ideally allocated towards savings, investments, or debt reduction. Understanding “what is a budget” is the foundational step for anyone seeking to gain control over their finances, make informed economic decisions, and ultimately achieve financial stability and prosperity.

In essence, budgeting is about conscious allocation – deciding where every dollar comes from and where it goes. It transforms abstract financial aspirations into concrete, actionable steps. Without a budget, financial management can feel like sailing without a compass, leaving one vulnerable to unexpected expenses, mounting debt, and missed opportunities for growth. Whether you’re navigating personal finances, steering a small business, or managing a large corporate entity, the principles remain consistent: clarity, control, and a commitment to your financial future.

The Core Components of a Budget

To truly grasp what a budget entails, one must dissect its fundamental elements. These components are universal, irrespective of the budget’s scale or complexity, and provide the framework for effective financial planning.

Income Sources

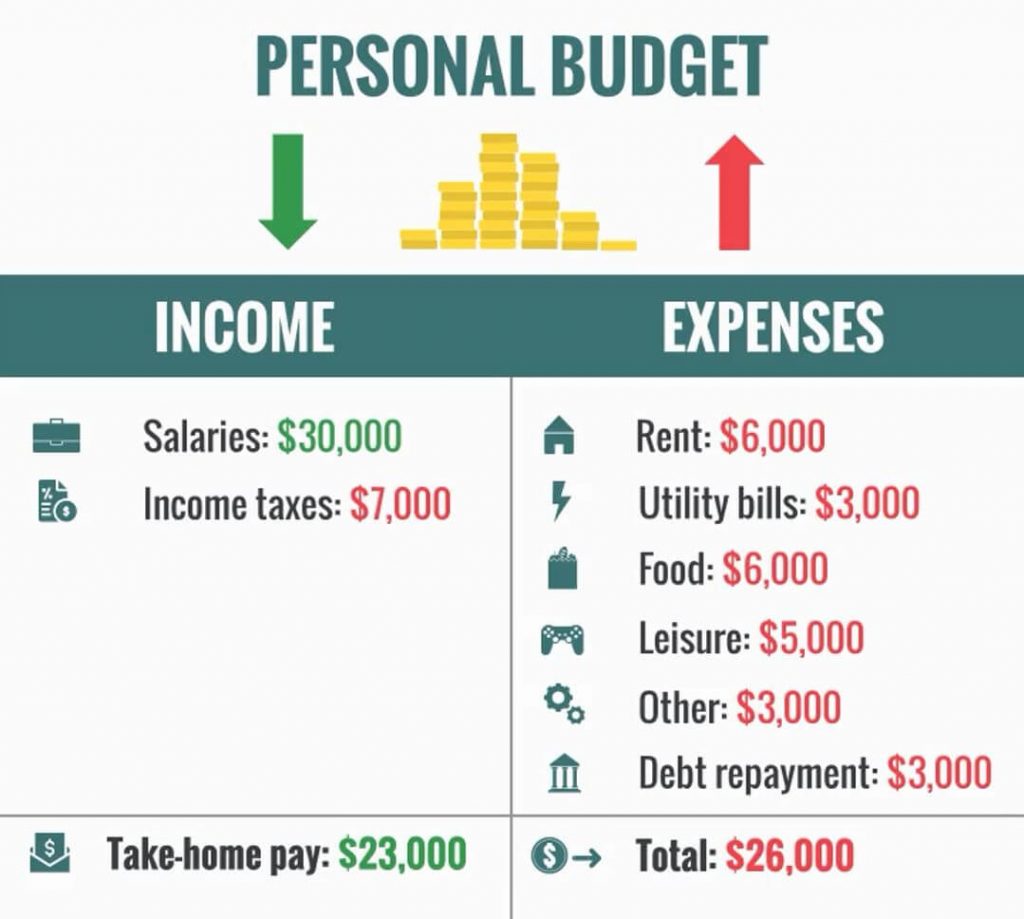

The starting point of any budget is identifying and quantifying all incoming funds. This represents the total financial resources available for allocation. For individuals, income typically includes salaries, wages, freelance earnings, rental income, investment dividends, or even gifts. For businesses, income stems from sales of goods or services, interest earned, or other revenue streams. A clear and accurate understanding of your total net income (after taxes and deductions) is paramount, as this figure dictates the parameters of your spending and saving. Failing to account for all income, or overestimating it, can quickly derail a budget before it even begins.

Expenses (Fixed vs. Variable)

Once income is established, the next critical step is to categorize and track outgoings. Expenses are broadly categorized into two types, each requiring a different approach to management:

- Fixed Expenses: These are costs that largely remain the same month after month and are generally non-negotiable or difficult to change in the short term. Examples include rent or mortgage payments, loan installments (car loans, student loans), insurance premiums, and subscription services (internet, streaming). Fixed expenses provide a stable baseline for your budget, as their predictability makes them easier to plan for.

- Variable Expenses: These costs fluctuate based on usage, lifestyle choices, or external factors, making them more challenging to predict accurately but also offering more flexibility for adjustment. Groceries, utilities (electricity, water, gas), transportation (fuel, public transport fares), dining out, entertainment, and clothing fall into this category. Managing variable expenses effectively is often key to finding savings and staying within budget, as they offer the most opportunities for discretionary cuts.

A comprehensive budget requires meticulously listing all expenses, both fixed and variable. This process not only reveals where money is currently going but also highlights areas where spending might be excessive or misaligned with financial goals.

Savings and Debt Repayment Goals

A truly effective budget doesn’t just balance income and expenses; it intentionally allocates funds towards future financial well-being. This involves setting clear goals for savings and debt repayment.

- Savings: This includes setting aside money for an emergency fund (typically 3-6 months’ worth of living expenses), retirement, a down payment on a house, a child’s education, a vacation, or any other future aspiration. Treating savings as a non-negotiable “expense” and automating contributions ensures consistent progress towards these goals.

- Debt Repayment: For those carrying debt, especially high-interest consumer debt like credit card balances, a budget must prioritize a strategic repayment plan. Allocating extra funds beyond minimum payments can significantly reduce interest paid and accelerate debt freedom, freeing up more money for savings and investments in the long run.

Integrating savings and debt repayment into the core of your budget transforms it from a mere tracking tool into a powerful instrument for building wealth and achieving long-term financial security.

Why Budgeting Matters: Benefits and Impact

The discipline of budgeting offers a myriad of benefits that extend far beyond simply knowing your numbers. It fundamentally reshapes one’s financial landscape, fostering security, control, and peace of mind.

Achieving Financial Goals

Perhaps the most compelling reason to budget is its efficacy in realizing financial aspirations. Whether your goal is to save for a down payment on a home, fund a child’s college education, retire comfortably, or embark on a dream vacation, a budget acts as the tactical plan. It allows you to assign specific amounts of money to these goals, track your progress, and make adjustments as needed. Without a clear financial plan, these dreams often remain just that – dreams – never translating into actionable steps. Budgeting turns intentions into reality by providing the structure necessary for consistent progress.

Reducing Financial Stress

One of the most immediate and profound impacts of budgeting is the significant reduction in financial stress. Uncertainty about money is a leading cause of anxiety. A budget eliminates much of this uncertainty by providing a clear picture of your financial situation. Knowing exactly how much income you have, where your money is going, and that you have a plan for future expenses (including emergencies) instills a powerful sense of control. This proactive approach prevents the panic that often accompanies unexpected bills or an unclear financial outlook, allowing for more peaceful and confident decision-making.

Identifying Overspending and Waste

The act of meticulously tracking income and expenses often serves as an eye-opening experience. Many individuals are surprised to discover how much money they spend on discretionary items or recurring, forgotten subscriptions. A budget provides a stark, objective view of spending habits, highlighting areas of potential overspending or unnecessary waste. This insight empowers individuals and businesses to make conscious choices about where to cut back, reallocate funds, and align their spending with their values and goals. It’s not about deprivation, but about intentionality and optimizing resource allocation.

Improving Financial Discipline and Habits

Budgeting is a consistent exercise in financial discipline. It encourages a shift from impulsive spending to thoughtful decision-making. By regularly reviewing your budget and making choices about where your money goes, you cultivate healthier financial habits. This discipline extends beyond mere spending; it fosters a mindset of delayed gratification, prioritization, and long-term planning. Over time, these habits become ingrained, leading to a more responsible and effective management of all financial resources, building a strong foundation for sustainable wealth creation.

Different Budgeting Methods and Approaches

There isn’t a single, universally perfect budgeting method. The best approach depends on an individual’s personality, financial situation, and preferences for detail and flexibility. Exploring various methods can help you find the one that resonates most effectively with your lifestyle.

The 50/30/20 Rule

Popularized by Senator Elizabeth Warren, this simple yet effective rule suggests allocating your after-tax income into three main categories:

- 50% for Needs: These are essential living expenses like housing, utilities, groceries, transportation, and minimum loan payments.

- 30% for Wants: This category includes discretionary spending that improves your quality of life but isn’t strictly necessary, such as dining out, entertainment, hobbies, and vacations.

- 20% for Savings & Debt Repayment: This portion is dedicated to building an emergency fund, retirement savings, investing, and paying down debt beyond the minimums.

The 50/30/20 rule offers a straightforward framework, making it an excellent starting point for those new to budgeting, as it prioritizes simplicity and flexibility.

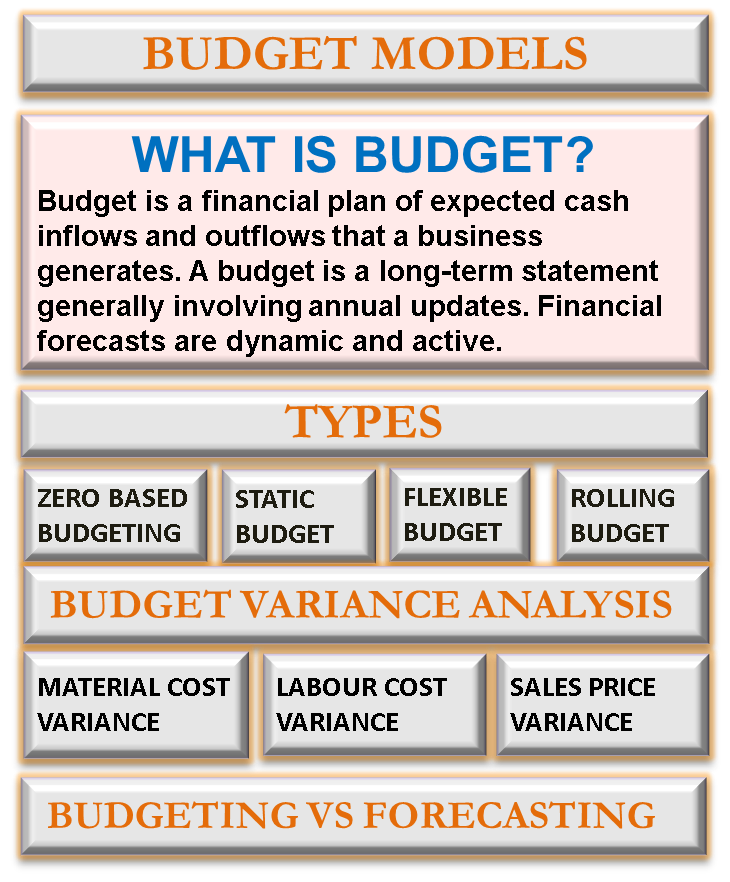

Zero-Based Budgeting

With zero-based budgeting, every dollar of income is assigned a specific job. This means that income minus expenses (including savings and debt payments) should equal zero. Instead of having money left over at the end of the month without a purpose, every dollar is intentionally allocated. This method demands meticulous tracking and planning but offers unparalleled control and ensures full accountability for every penny. It’s particularly effective for individuals or businesses who want to maximize every dollar and eliminate wasteful spending, though it can be more time-consuming to set up and maintain initially.

Envelope System

The envelope system is a classic, cash-based budgeting method that is particularly effective for controlling variable spending. At the beginning of each budget period (e.g., month or bi-weekly), you withdraw cash for your variable expenses (like groceries, entertainment, personal care) and divide it into physical envelopes labeled for each category. Once the cash in an envelope is gone, you stop spending in that category until the next budget period. This method makes overspending tangible and immediate, helping to curb impulse purchases. While less practical for all expenses in a digital age, it remains powerful for categories where overspending is common.

Budgeting Apps and Tools

In the digital era, a plethora of apps and online tools have revolutionized budgeting. Platforms like Mint, YNAB (You Need A Budget), Personal Capital, and countless others offer automated expense tracking, categorization, goal setting, and visual reports. Many can sync directly with bank accounts and credit cards, making the process significantly less manual. These tools provide convenience, real-time insights, and often incorporate features like bill reminders and net worth tracking, making budgeting more accessible and engaging for tech-savvy users. They democratize sophisticated financial management, putting powerful analytical capabilities into the hands of everyday users.

Implementing and Maintaining Your Budget

Creating a budget is the first step; consistently implementing and maintaining it is where the real work—and rewards—lie. A budget is a living document that requires ongoing attention and adaptation.

Tracking Income and Expenses Diligently

The cornerstone of successful budgeting is diligent tracking. Whether you use a spreadsheet, a dedicated app, or even pen and paper, consistently recording all income and expenses is non-negotiable. This means reviewing bank statements, credit card transactions, and cash receipts regularly. Consistency provides the accurate data needed to assess your financial health, identify trends, and ensure you’re sticking to your plan. Inaccurate or inconsistent tracking renders any budget ineffective, as it masks the true financial picture. Many budgeting apps automate this process, significantly easing the burden and improving accuracy.

Regular Review and Adjustment

A budget is not a static document; it’s a dynamic financial tool that needs regular review and adjustment. Life happens: income changes, unexpected expenses arise, and financial goals evolve. It’s crucial to schedule regular check-ins—monthly or quarterly—to assess your budget’s performance. During these reviews, compare your actual spending against your budgeted amounts. Identify areas where you overspent or underspent, and then adjust your allocations for the next period. This iterative process ensures your budget remains realistic, relevant, and effective in guiding you toward your financial objectives. Flexibility is key to long-term budgeting success.

Overcoming Common Budgeting Challenges

Budgeting comes with its share of challenges. Many people struggle with a lack of discipline, feeling deprived, or encountering unexpected expenses that throw their plan off course. To overcome these:

- Be Realistic: Set achievable spending limits rather than overly restrictive ones that lead to burnout. Include “fun money” in your budget to avoid feeling deprived.

- Automate: Automate savings transfers and bill payments whenever possible to reduce the reliance on willpower.

- Plan for the Unexpected: Build an emergency fund to cover unforeseen costs, preventing them from derailing your budget entirely.

- Forgive Yourself: If you overspend in a category, don’t abandon the entire budget. Adjust for the next month and learn from the experience. Consistency, not perfection, is the goal.

The Role of Financial Education

Effective budgeting is greatly enhanced by continuous financial education. Understanding principles of personal finance, investing, debt management, and economic trends empowers you to make more informed budgeting decisions. Learning about compound interest, different investment vehicles, and strategies for accelerating debt repayment can transform your budget from a simple spending plan into a powerful wealth-building engine. Resources are abundant, from books and podcasts to online courses and financial advisors, all contributing to a more nuanced and strategic approach to managing your money.

Beyond Personal Budgeting: Business and Project Budgets

While commonly associated with personal finance, the principles of budgeting are equally critical—and often more complex—in the corporate world, extending to business operations and specific projects.

Business Budgeting Fundamentals

For businesses, a budget is an indispensable tool for strategic planning, resource allocation, and performance measurement. A business budget forecasts revenues, operating expenses, capital expenditures, and cash flow over a specific period, typically a fiscal year. It serves multiple vital functions:

- Resource Allocation: Ensures funds are directed to areas that generate the most value or are critical for operations.

- Performance Benchmarking: Provides a standard against which actual financial results can be compared, highlighting variances and informing corrective actions.

- Cash Flow Management: Helps prevent liquidity crises by anticipating periods of surplus or deficit.

- Decision Making: Guides decisions on investments, hiring, marketing campaigns, and product development.

- Accountability: Assigns financial responsibility to various departments or cost centers.

Business budgeting requires a deeper dive into financial statements, market analysis, and economic forecasts to ensure accuracy and strategic alignment.

Project Budgeting

Project budgeting is a specialized form of business budgeting focused on the financial planning and control of a specific project. Each project, whether developing a new product, constructing a building, or launching a marketing campaign, requires its own budget.

- Defining Scope: Clearly outlining the project’s objectives and deliverables is the first step, as it dictates the resources needed.

- Estimating Costs: This involves breaking down the project into individual tasks and estimating the cost of labor, materials, equipment, and overhead for each. Contingency funds are often included for unforeseen issues.

- Monitoring Expenditures: Throughout the project lifecycle, actual spending is rigorously tracked against the budget to ensure adherence. Variances are analyzed, and corrective actions are taken to keep the project on track financially.

- Resource Management: Project budgets help allocate human, material, and financial resources efficiently, minimizing waste and maximizing return on investment.

Effective project budgeting is crucial for delivering projects on time, within scope, and within financial constraints, directly impacting profitability and organizational success.

In conclusion, “what is a budget” unravels into a multifaceted concept encompassing foresight, discipline, and strategic allocation of resources. It is not merely a restrictive list of don’ts, but rather an empowering financial roadmap that illuminates your path to achieving monetary goals, reducing stress, and building lasting wealth. Whether for personal well-being or organizational success, embracing the discipline of budgeting is the single most powerful step towards financial mastery. It’s an ongoing journey of learning, adjusting, and continuously aligning your financial actions with your deepest aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.