In the complex landscape of personal finance, few terms are as ubiquitous—and as frequently misunderstood—as the Annual Percentage Rate, or APR. Whether you are applying for your first credit card, financing a new vehicle, or navigating the intricate process of securing a mortgage, the APR is the single most important metric for determining the true cost of borrowing money. While many consumers focus solely on the “interest rate,” the APR provides a more comprehensive picture, incorporating various fees and costs that interest rates alone do not account for.

Understanding APR is not merely an academic exercise; it is a fundamental skill for anyone looking to optimize their financial health, reduce debt, and make informed investment decisions. This guide explores the mechanics of APR, its various forms, and how it directly impacts your long-term financial trajectory.

Understanding the Mechanics: The Core of APR

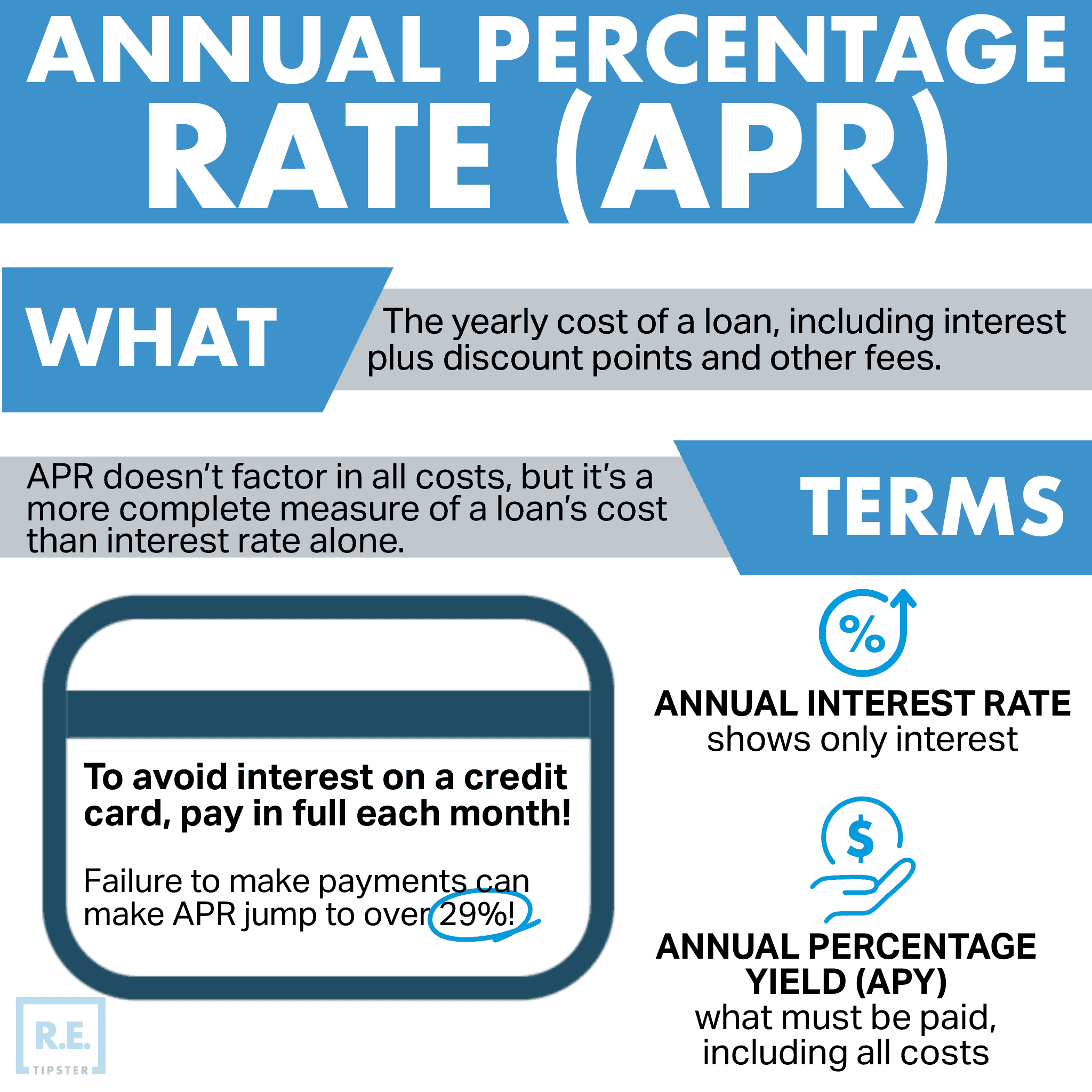

To truly grasp what an Annual Percentage Rate is, one must first distinguish it from the nominal interest rate. While the interest rate tells you the cost of borrowing the principal balance, the APR represents the total annual cost of the loan expressed as a percentage. This includes the interest rate plus any other fees or charges involved in procuring the loan, such as origination fees, mortgage insurance, or closing costs.

The Definition of Annual Percentage Rate

The APR serves as a standardized measure that allows consumers to compare different loan products on an “apples-to-apples” basis. Under the Truth in Lending Act (TILA) in the United States, lenders are required to disclose the APR to borrowers before they sign a contract. This transparency ensures that a lender cannot hide the true cost of a loan behind a low interest rate while padding the deal with exorbitant administrative fees. Essentially, the APR is the “bottom line” of a financial agreement.

Interest Rate vs. APR: Key Differences

The primary difference between a nominal interest rate and an APR lies in the inclusion of prepaid finance charges. For example, if you take out a $200,000 mortgage with a 6% interest rate but have to pay $5,000 in closing costs and fees, your APR will be higher than 6%—perhaps closer to 6.25%.

It is important to note that while APR includes these fees, it does not typically account for “compounding”—the process where interest is charged on top of interest that has already accumulated. For credit cards, which compound daily or monthly, the “Effective Annual Rate” (EAR) is often higher than the stated APR. However, for the purpose of comparison, APR remains the industry standard.

How APR is Calculated

The mathematical formula for APR is relatively straightforward, though it can become complex depending on the loan structure. Generally, it is calculated by adding the total interest paid over the life of the loan to any additional fees, dividing that sum by the principal amount, then dividing by the total number of days in the loan term, and finally multiplying by 365 and 100 to get a percentage. In simpler terms: it is the total cost of credit, averaged over the year, expressed as a percentage of the amount you borrowed.

Different Types of APR You Should Know

Not all APRs are created equal. Depending on the financial product, the APR may function differently, and understanding these nuances can save a borrower thousands of dollars over the lifetime of a loan.

Fixed vs. Variable APR

Loans generally come with either a fixed or a variable APR. A Fixed APR remains constant throughout the life of the loan or the duration of the agreement. This provides predictability, as your monthly payments will not change due to market fluctuations. Fixed rates are common in personal loans and many mortgages.

Conversely, a Variable APR is tied to an index, such as the U.S. Prime Rate. When the index moves up or down, your APR—and consequently your monthly payment—will follow. Many credit cards and Adjustable-Rate Mortgages (ARMs) use variable APRs. While these may start lower than fixed rates, they carry the risk of increasing if the economy shifts or the Federal Reserve raises interest rates.

Purchase APR vs. Cash Advance APR

If you carry a credit card, you likely have multiple APRs applied to different types of transactions. The Purchase APR is the rate applied to standard buys, like groceries or clothing. However, if you use your credit card to withdraw cash from an ATM, you are subject to a Cash Advance APR. This rate is almost always significantly higher than the purchase APR and usually begins accruing interest immediately, without the standard 21-to-25-day grace period offered for purchases.

Penalty APR and Introductory Rates

Many lenders offer an “introductory” or “teaser” APR—often 0%—to entice new customers. These rates are temporary and will eventually revert to a standard, higher APR. Furthermore, if you miss a payment or violate the terms of your agreement, a lender may trigger a Penalty APR. This is a much higher rate (often 29.99%) that can stay on your account indefinitely, making it much harder to pay down your balance.

The Impact of APR on Loans and Credit Cards

The APR is the engine that drives the cost of debt. A difference of even 1% in APR can lead to a staggering difference in the total amount paid over several years.

Mortgages and Auto Loans

In the context of long-term borrowing, such as a 30-year mortgage, the APR is the most critical factor. Because the loan amount is large and the duration is long, even a fractional increase in APR translates to tens of thousands of dollars in interest. For auto loans, which are shorter (typically 3 to 7 years), the APR determines how much “extra” you are paying for the vehicle. If you buy a $30,000 car at a 3% APR versus an 8% APR, you could end up paying nearly $4,000 more for the exact same vehicle.

Credit Card Debt and Compounding

Credit cards are revolving lines of credit, meaning the APR is applied to whatever balance you carry from month to month. Because credit card APRs are notoriously high (often averaging between 18% and 25%), carrying a balance can quickly lead to a debt spiral. If you only pay the “minimum amount” due each month, the high APR ensures that most of your payment goes toward interest rather than reducing the principal.

How APR Affects Your Monthly Payments

A higher APR directly increases your monthly debt obligation. This reduces your discretionary income—the money you have left over for savings, investing, or lifestyle expenses. By securing lower APRs, you effectively “give yourself a raise” by keeping more of your hard-earned money in your own pocket rather than handing it over to a financial institution.

Factors That Determine Your APR

Lenders do not assign APRs at random; they are a reflection of the risk the lender perceives in lending money to you. Several key factors influence the rate you are offered.

Credit Scores and Financial History

Your credit score is the most significant determinant of your APR. Lenders use scores from bureaus like Experian, Equifax, and TransUnion to gauge your reliability. A “prime” borrower with a score above 740 will almost always qualify for the lowest available APRs. Conversely, a “subprime” borrower with a score below 600 may be charged much higher rates to compensate the lender for the increased risk of default.

The Role of the Federal Reserve and Prime Rate

Macroeconomic factors also play a role. The Federal Open Market Committee (FOMC) sets the federal funds rate, which influences the Prime Rate—the base interest rate that commercial banks charge their most creditworthy corporate customers. When the Federal Reserve raises rates to combat inflation, APRs across the board—from credit cards to mortgages—tend to rise.

Debt-to-Income Ratio and Loan Terms

Beyond your credit score, lenders look at your Debt-to-Income (DTI) ratio. If a large portion of your monthly income is already committed to debt payments, a lender may charge a higher APR because you have less financial “wiggle room.” Additionally, the length of the loan matters; typically, shorter-term loans carry lower APRs than longer-term loans because the lender is exposed to risk for a shorter period.

Strategies to Secure a Lower APR

Navigating the world of finance requires a proactive approach. You do not have to accept the first APR you are offered.

Improving Your Credit Profile

The most effective way to lower your APRs is to improve your credit score. This involves paying all bills on time, keeping your credit utilization ratio (the amount of credit you use versus your limit) below 30%, and avoiding opening too many new accounts in a short period. As your score rises, you can often call your credit card issuers and request a rate reduction based on your improved creditworthiness.

Comparison Shopping and Negotiation

Never settle for the first loan offer. When shopping for a mortgage or auto loan, apply with multiple lenders within a 14-day window. This allows you to compare APRs without significantly damaging your credit score, as multiple inquiries for the same type of loan are often treated as a single event. Use the lowest offer as leverage to negotiate better terms with your preferred bank.

Refinancing and Balance Transfers

If you are currently stuck with a high-APR loan, consider refinancing. If interest rates have dropped or your credit has improved since you took out the loan, you can replace your current debt with a new loan at a lower APR. For credit card debt, a “Balance Transfer” card with a 0% introductory APR can be a powerful tool to pay off debt faster, provided you have a plan to clear the balance before the introductory period ends.

Conclusion

The Annual Percentage Rate is more than just a number on a statement; it is a vital indicator of your financial efficiency. By looking past the nominal interest rate and focusing on the APR, you gain a transparent view of the costs associated with borrowing. Whether you are managing daily expenses on a credit card or making the largest purchase of your life with a home mortgage, a deep understanding of APR empowers you to minimize costs and maximize your wealth. In the world of personal finance, knowledge is the most valuable asset, and mastering the concept of APR is a significant step toward achieving true financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.