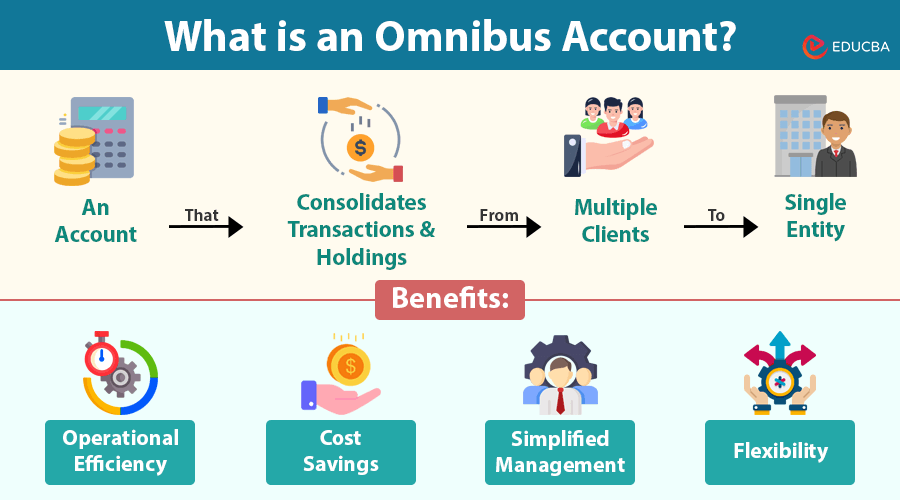

An omnibus account is a financial holding that consolidates multiple individual client accounts into a single account held by a third party, typically a broker-dealer or an investment advisor. This consolidation offers significant operational and administrative efficiencies for the firm managing the assets, while also providing a streamlined experience for the underlying clients. While the concept might seem complex, understanding omnibus accounts is crucial for anyone involved in investment management, especially those working with or through financial intermediaries.

This structure allows for a single point of contact and a unified reporting system, simplifying the management of a large number of client portfolios. Instead of each individual client’s trades and holdings being tracked and reported separately, they are aggregated. This doesn’t mean individual ownership is lost; it simply means the administrative burden of managing these individual positions is centralized. The article will delve into the mechanics of how these accounts operate, the advantages they offer to various stakeholders, and the regulatory considerations that govern their use.

The Mechanics of an Omnibus Account

At its core, an omnibus account operates on a principle of aggregation. A financial institution, acting as the intermediary, opens a single account with a custodian, such as a large bank or clearing house. This single account, the omnibus account, then holds the securities and cash for a multitude of underlying client accounts. The intermediary is responsible for maintaining the records of which assets belong to which individual client within this aggregated account.

How Positions are Held and Managed

The key to understanding an omnibus account lies in differentiating between the beneficial owner and the record owner. The client is the beneficial owner of the assets within the account, meaning they retain all rights and economic benefits associated with those assets. However, the intermediary (e.g., the broker-dealer) is often the record owner on the custodian’s books. This means the custodian sees only one account – the omnibus account – and its holder, the intermediary.

When an investment decision is made for an individual client, the intermediary executes the trade through the omnibus account. For instance, if a financial advisor instructs their firm to buy 100 shares of Stock X for Client A and 50 shares of Stock X for Client B, the firm will execute a single order for 150 shares of Stock X through the omnibus account. Once the trade settles, the intermediary then internally allocates those 100 shares to Client A’s sub-account and the 50 shares to Client B’s sub-account. This internal record-keeping is critical and is the responsibility of the intermediary.

The Role of the Intermediary

The intermediary – which can be a registered investment advisor (RIA), a broker-dealer, a hedge fund, or even a mutual fund – plays a pivotal role in the omnibus account structure. They are the entity that interfaces directly with the custodian and is responsible for the overall administration and reconciliation of the omnibus account. Their duties include:

- Trade Execution: Placing trades on behalf of all their clients.

- Settlement: Ensuring trades are properly settled with the custodian.

- Reconciliation: Regularly reconciling the omnibus account holdings with the individual client account records to ensure accuracy.

- Reporting: Providing consolidated reports to the custodian and individual statements to clients.

- Compliance: Adhering to all regulatory requirements related to holding client assets.

Without the intermediary’s robust internal systems and processes, the omnibus account structure would be unmanageable and prone to errors.

Advantages of Using Omnibus Accounts

The adoption of omnibus accounts by financial institutions stems from a clear set of benefits, primarily centered around efficiency and cost-effectiveness. These advantages ripple through to the operational capabilities of the intermediary and, indirectly, to the client experience.

For Financial Intermediaries

For firms managing client assets, omnibus accounts are a cornerstone of efficient operations.

- Operational Efficiency: The most significant advantage is the reduction in administrative overhead. Instead of processing thousands of individual trades, settlements, and reporting tasks for each client, the intermediary handles these operations in bulk. This streamlines back-office functions, requiring fewer personnel and less time for manual tasks.

- Cost Savings: Reduced operational workload directly translates to lower costs. Fewer staff are needed for administrative duties, and economies of scale are achieved in areas like trading fees and custodial charges, as these are negotiated on a larger, consolidated basis.

- Simplified Reporting: Consolidating client data into a single omnibus account simplifies the process of generating internal reports and statements for the custodian. While individual client statements still need to be generated, the underlying data aggregation is more manageable.

- Enhanced Trading Capabilities: By aggregating client orders, intermediaries can often achieve better execution prices through bulk trading. This can lead to improved investment performance for clients, as trades are executed at more favorable market prices.

For Underlying Clients

While clients may not directly interact with the concept of an omnibus account, they benefit from its existence in several ways.

- Potentially Lower Fees: The cost savings realized by the intermediary due to operational efficiencies can sometimes be passed on to clients in the form of lower management fees or trading commissions.

- Smoother Account Opening and Management: The administrative simplification for the intermediary can translate to a smoother onboarding process for new clients and a more seamless overall account management experience.

- Access to Sophisticated Investment Management: Omnibus accounts are a key enabler for many investment vehicles, such as mutual funds and hedge funds, which pool capital from numerous investors. Without this structure, offering such investment products at scale would be significantly more complex and costly.

- Consolidated Reporting (Indirectly): While clients receive individual statements, the underlying consolidation by the intermediary ensures that their holdings are accurately tracked and reflected, even if they are part of a larger pool.

Regulatory and Compliance Considerations

The use of omnibus accounts, while offering significant benefits, is subject to strict regulatory oversight to protect investors and maintain market integrity. Regulatory bodies like the Securities and Exchange Commission (SEC) in the United States have established rules that govern how these accounts are established, managed, and reported.

Key Regulations and Investor Protection

- Customer Protection Rules: Regulations such as the SEC’s Rule 15c3-3 (Customer Protection Rule) are designed to safeguard customer securities and cash held by broker-dealers. When using omnibus accounts, intermediaries must demonstrate compliance with these rules by clearly delineating and segregating customer assets, even within the consolidated account.

- Disclosure Requirements: Intermediaries are required to provide clear and comprehensive disclosures to their clients about how their assets are held, including the use of omnibus accounts. Clients should understand who holds their assets, how they are managed, and what rights they retain.

- Reporting and Audit Trails: Robust record-keeping is paramount. Regulators require detailed audit trails of all transactions within the omnibus account, including the allocation of trades and other activities to individual client accounts. This ensures transparency and facilitates regulatory investigations if necessary.

- Best Execution Obligations: When executing trades through an omnibus account, the intermediary must still adhere to its “best execution” obligations, meaning they must strive to obtain the most favorable terms reasonably available for their clients’ orders. This is particularly important when aggregating orders, as the intermediary must ensure that the aggregated order execution benefits all participating clients.

- Segregation of Assets: Even though assets are held in a single omnibus account, they must be segregated from the broker-dealer’s own assets. This is a critical protection in the event of the intermediary’s insolvency, ensuring that client assets can be returned to their rightful owners.

The Role of the Custodian

The custodian, such as a large bank or clearing firm, also plays a crucial role in the regulatory framework. They are responsible for:

- Holding Assets: Safekeeping the securities and cash held within the omnibus account.

- Confirming Holdings: Providing regular confirmations of the assets held in the omnibus account to the intermediary.

- Monitoring for Suspicious Activity: While not directly managing individual client accounts, custodians are often involved in identifying and reporting any anomalies or suspicious activities within the omnibus account structure.

The regulatory landscape surrounding omnibus accounts is dynamic and subject to change. Financial intermediaries must remain vigilant in their adherence to these rules to ensure the continued trust and protection of their clients.

When are Omnibus Accounts Typically Used?

The efficiency and scalability offered by omnibus accounts make them a preferred choice in various financial contexts. Their application spans across different types of financial products and service providers, highlighting their versatility in the modern financial ecosystem.

Investment Funds and Pooled Investments

- Mutual Funds: A primary user of omnibus accounts. When you invest in a mutual fund, your purchase is typically recorded within an omnibus account held by the fund’s administrator or transfer agent at a custodian. This allows the fund to manage millions of dollars from thousands of investors as a single entity, streamlining operations and making it easier to calculate net asset value (NAV).

- Hedge Funds: Similar to mutual funds, hedge funds pool capital from accredited investors. Their trading and asset management are often facilitated through omnibus accounts, enabling sophisticated trading strategies and efficient management of diverse portfolios.

- Exchange-Traded Funds (ETFs): While ETFs trade on exchanges, the underlying creation and redemption process, as well as the holding of assets by the fund, often involves omnibus accounts at the custodian level.

Broker-Dealers and Financial Advisors

- Direct-Investing Brokerages: Large online brokerages that allow individual investors to buy and sell securities often use omnibus accounts at clearing firms. This centralizes the clearing and settlement processes for all their customers’ trades.

- Independent Financial Advisors (RIAs): RIAs who manage client portfolios through a custodian may utilize omnibus accounts. This allows them to manage multiple client accounts with a single point of contact for trading and reporting with the custodian, simplifying their operational workflow.

- Retirement Plans (e.g., 401(k)s): The assets held within large employer-sponsored retirement plans are often aggregated into omnibus accounts managed by a plan administrator or record keeper. This facilitates the administration of contributions, withdrawals, and investment options for a large number of employees.

Other Financial Services

- Introducing Brokers: These brokers introduce clients to a carrying broker (a larger firm that handles the clearing and settlement). The carrying broker will often hold the client assets in an omnibus account.

- Prime Brokerage Services: For hedge funds and other institutional clients, prime brokers offer a suite of services including lending, clearing, and custody. Omnibus accounts are a fundamental component of prime brokerage operations, consolidating the assets and trading activity of multiple clients.

In essence, any scenario where a financial institution needs to manage a large number of individual investment accounts efficiently and cost-effectively is a potential candidate for the utilization of omnibus accounts. They are a silent but critical infrastructure supporting many of the investment vehicles and services that individuals and institutions rely on daily.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.