For high-net-worth investors, corporate executives, and early employees of successful startups, the “problem” of wealth is often concentrated in a single stock. While having a significant position in a high-performing company is the foundation of many fortunes, it also presents a precarious financial paradox: you are wealthy on paper, but your portfolio is dangerously undiversified. Selling the stock to diversify triggers a massive capital gains tax bill, potentially eroding 20% to 30% of your wealth instantly.

This is where the exchange fund, often referred to as a “swap fund,” becomes a critical instrument in the sophisticated investor’s toolkit. An exchange fund is a private investment vehicle designed to help investors diversify concentrated stock positions without triggering an immediate tax event. By pooling their shares with other investors holding different stocks, participants gain exposure to a diversified basket of assets while deferring capital gains taxes.

Understanding the Mechanics of an Exchange Fund

The concept of an exchange fund is rooted in the principle of “like-kind” exchanges, though it operates under specific sections of the Internal Revenue Code (primarily Section 721). Unlike a traditional Mutual Fund or ETF, which you purchase with cash, you “buy” into an exchange fund by contributing your highly appreciated shares.

The Swap Mechanism Explained

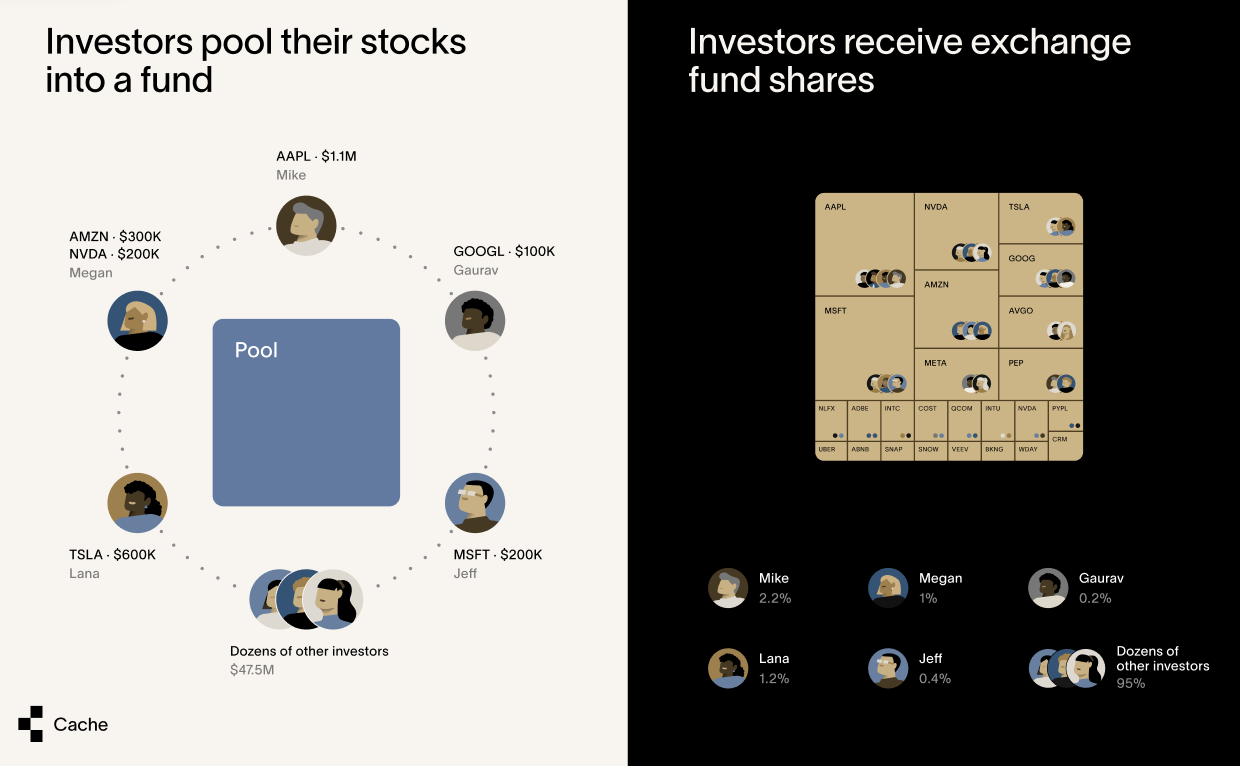

In a typical exchange fund, an investment bank or a specialized fund manager assembles a group of investors. Each investor contributes a concentrated position of a publicly traded stock. In return, each participant receives a pro-rata interest in the fund’s total portfolio.

For example, an executive with $5 million in Apple stock might join a fund where other participants have contributed similar amounts of Microsoft, Amazon, Tesla, and ExxonMobil. Instead of owning one volatile asset, the executive now owns a slice of a diversified portfolio containing dozens of different blue-chip stocks. Because this is structured as a contribution to a partnership rather than a sale, the IRS does not recognize it as a taxable event at the time of the swap.

Tax Deferral vs. Tax Avoidance

It is important to distinguish that an exchange fund is a tax-deferral strategy, not a tax-avoidance strategy. Your original “cost basis” in your concentrated stock carries over to your interest in the fund. If you eventually exit the fund and receive a basket of diversified stocks, your basis remains the same. You only pay the capital gains tax when you finally sell those diversified shares for cash. The power of this strategy lies in the “time value of money”—by keeping the 20-30% of your wealth that would have gone to the IRS, you allow that money to continue compounding within a diversified environment for years or even decades.

Why Investors Use Exchange Funds

The primary driver for using an exchange fund is the mitigation of “idiosyncratic risk.” While the broad market may be stable, an individual company can face unforeseen regulatory hurdles, management scandals, or technological disruptions that cause its stock price to plummet.

Mitigating Concentration Risk

Many investors find themselves “locked” into a position because the tax consequences of selling are too painful to stomach. This is often called the “tax trap.” An exchange fund provides an escape hatch. It allows the investor to move from a high-risk, single-stock position into a diversified portfolio that mirrors a broad index (like the S&P 500) without losing a third of their investment to the government. This shift stabilizes the investor’s net worth and protects their lifestyle from the volatility of a single company’s performance.

Estate Planning and Long-Term Wealth Transfer

Exchange funds are frequently used as long-term estate planning tools. Under current U.S. tax law, assets held until death receive a “step-up in basis” to their fair market value. If an investor holds their exchange fund interest until they pass away, their heirs inherit the diversified portfolio at its current value, effectively eliminating the deferred capital gains tax entirely. This makes the exchange fund one of the most powerful ways to transition concentrated corporate wealth into a diversified family legacy.

Regulatory Requirements and Structure

Because of the significant tax advantages, the IRS has established strict rules regarding how exchange funds must be structured. If these rules are not followed, the fund could be classified as an “investment company,” which would trigger the very taxes the investors are trying to avoid.

The 20% Rule for Illiquid Assets

To qualify for tax-deferred treatment, an exchange fund cannot consist entirely of “marketable securities.” According to IRS regulations, at least 20% of the fund’s assets must be “non-marketable” or illiquid assets.

Typically, fund managers satisfy this requirement by investing 20% of the fund’s capital into private real estate, timberland, or other illiquid investments. While this adds a layer of complexity to the fund, it also provides an additional layer of diversification. However, it means that the performance of the exchange fund will not perfectly track the S&P 500, as it is influenced by the performance of these private holdings.

Eligibility: Are You a Qualified Purchaser?

Exchange funds are not available to the general public. They are structured as private placements under Regulation D of the Securities Act. To participate, an investor must usually meet the “Qualified Purchaser” standard, which generally requires owning at least $5 million in investable assets (excluding their primary residence).

Furthermore, the fund manager must “accept” the stock you wish to contribute. If a fund already has a high concentration of a specific tech stock, they may decline further contributions of that stock to maintain the fund’s internal diversification.

Key Risks and Considerations

While the benefits are substantial, exchange funds are not without their drawbacks. They are sophisticated financial instruments that require a long-term commitment and a high tolerance for illiquidity.

The Seven-Year Holding Period

To solidify the tax-deferred status, investors must generally remain in the fund for at least seven years. If you withdraw your assets before this period ends, you may trigger the capital gains tax you sought to defer, or you may be forced to take back your original concentrated shares, defeating the purpose of the diversification. This “lock-up period” means that exchange funds are only suitable for capital that you do not expect to need for liquidity in the near future.

Fee Structures and Management Costs

Managing a private partnership that holds hundreds of millions of dollars in stock and 20% in private real estate is expensive. Exchange funds typically charge an upfront “load” or placement fee, as well as an annual management fee (often ranging from 0.50% to 1.5%). When compared to the virtually zero cost of holding a single stock or a low-cost S&P 500 ETF, these fees can eat into the total return over time. Investors must weigh these costs against the massive “alpha” provided by the tax deferral.

Comparing Exchange Funds to Other Strategies

An exchange fund is just one way to manage a concentrated position. Depending on an investor’s specific goals, other “Money” strategies might be more appropriate.

Direct Indexing vs. Exchange Funds

Direct indexing involves buying the individual components of an index in a taxable account and using “tax-loss harvesting” to offset the gains from selling a concentrated position. This offers more control and liquidity than an exchange fund but usually takes much longer to achieve full diversification without paying taxes. In contrast, an exchange fund provides “instant” diversification the moment the swap occurs.

Hedging with Derivatives

Some investors choose to use options strategies, such as “zero-cost collars,” to protect the downside of their concentrated stock. While this protects against a price drop, it does not achieve diversification, and it does not solve the long-term tax problem. It is often used as a temporary measure while waiting for an opening in an exchange fund.

Opportunity Zones and 1031 Exchanges

For investors with a high appetite for real estate, reinvesting capital gains into a Qualified Opportunity Zone (QOZ) can provide tax deferral and potential tax elimination. However, QOZs require the investor to sell the stock first and then reinvest the cash into specific geographic areas. An exchange fund is unique because it allows for the swap of equities for equities, keeping the investor within the stock market.

Conclusion

The exchange fund remains one of the most effective wealth management tools for individuals facing the “concentration conundrum.” By navigating the intersection of tax law and portfolio theory, these funds allow investors to transform a risky, single-stock gamble into a disciplined, diversified investment strategy.

For the modern investor, the decision to enter an exchange fund should be made in consultation with tax advisors and financial planners. While the seven-year lock-up and the strict eligibility requirements are significant hurdles, the ability to defer taxes while immediately lowering your risk profile is a powerful advantage in the pursuit of long-term financial security. In the world of high-stakes investing, the exchange fund is the ultimate bridge between the wealth you have built and the legacy you wish to protect.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.