For most individuals, a home is the most significant purchase they will ever make. Consequently, the mortgage used to finance that purchase is the most consequential financial contract they will ever sign. At the heart of this contract is the interest rate—a percentage that dictates not only your monthly payment but the total cost of your home over several decades.

When people ask, “What is an average mortgage interest rate?” they are often looking for a simple number. However, the “average” is a fluid concept, shaped by macroeconomic forces, lender risk assessments, and the personal financial profile of the borrower. Understanding how this rate is determined is essential for any savvy investor or homebuyer looking to optimize their personal balance sheet.

The Macroeconomic Drivers of Mortgage Averages

The average mortgage interest rate is not set by a single entity. Instead, it is the result of a complex interplay between government policy and the global bond market. While the news often focuses on the Federal Reserve, the relationship between the “Fed” and your mortgage is more nuanced than many realize.

The Influence of the Federal Reserve

The Federal Reserve does not directly set mortgage rates. Instead, it sets the federal funds rate—the interest rate at which commercial banks borrow and lend to each other overnight. When the Fed raises this rate to combat inflation, it becomes more expensive for banks to borrow money. To maintain their profit margins, banks pass these costs on to consumers in the form of higher interest rates on credit cards, personal loans, and mortgages. Conversely, when the economy slows, the Fed may lower rates to encourage borrowing and spending, which generally leads to a decrease in mortgage averages.

The 10-Year Treasury Yield and the Secondary Market

In the financial world, mortgage-backed securities (MBS) are a primary driver of mortgage rates. Most lenders do not keep your mortgage on their books; they package it with other loans and sell it to investors on the secondary market. Because mortgages are seen as relatively safe long-term investments, they compete directly with the 10-year U.S. Treasury note.

Historically, there is a strong correlation between the 10-year Treasury yield and the 30-year fixed mortgage rate. Usually, there is a “spread” or a gap of about 1.5 to 2 percentage points between the two. If the yield on government bonds rises, mortgage rates must rise as well to remain attractive to investors. When you see the “average” rate reported in the media, you are seeing the equilibrium point where investors are willing to buy these loans in the current economic climate.

Personal Variables: Why Your Rate May Differ from the Average

National averages, such as those reported by Freddie Mac or Fannie Mae, are based on “prime” borrowers—individuals with high credit scores and substantial down payments. If your financial profile differs from this archetype, the rate you are offered may be significantly higher or lower than the published average.

The Weight of Credit Scores

In the realm of personal finance, your credit score is your most valuable currency. Lenders use FICO scores to categorize borrowers into risk tiers. A borrower with a score of 760 or higher is considered low-risk and will likely receive a rate at or below the national average.

For those with scores in the 620 to 680 range, lenders perceive a higher “risk of default.” To compensate for this risk, they add a premium to the interest rate. Over the life of a 30-year loan, the difference between a 3.5% rate and a 4.5% rate can amount to tens of thousands of dollars in interest. This is why financial advisors emphasize credit repair as a prerequisite for homebuying.

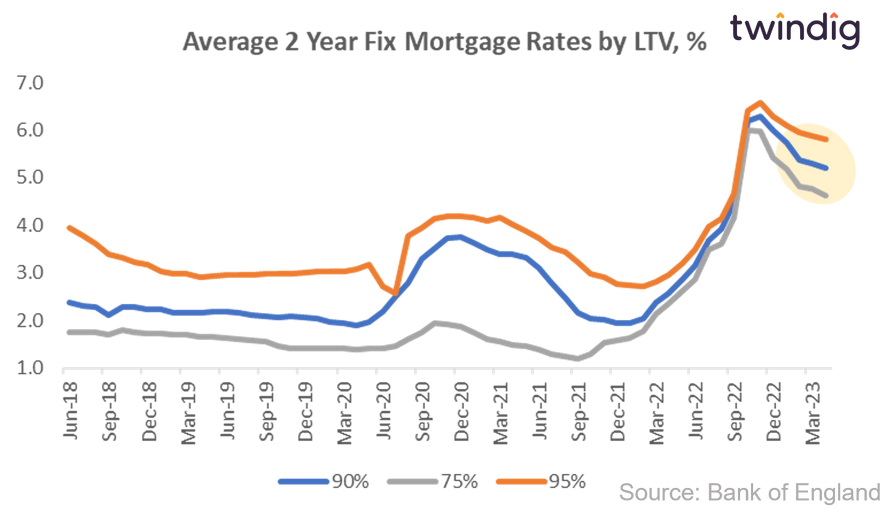

Loan-to-Value (LTV) and Down Payments

The amount of equity you put into the home upfront also dictates your rate. The Loan-to-Value (LTV) ratio measures the amount of the loan against the value of the property. A standard 20% down payment results in an 80% LTV.

Lenders prefer lower LTVs because the borrower has more “skin in the game.” If a borrower provides only a 3.5% down payment (common with FHA loans), the lender takes on more risk. To mitigate this, the lender may charge a higher interest rate or require Private Mortgage Insurance (PMI), which increases the effective cost of the loan even if the nominal interest rate remains near the average.

Analyzing Different Mortgage Products and Their Rates

The “average mortgage rate” usually refers to the 30-year fixed-rate mortgage, but this is only one of many financial instruments available to borrowers. Each product carries a different risk profile and, consequently, a different average rate.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

A fixed-rate mortgage offers stability; the interest rate remains the same for the entire duration of the loan. This is the gold standard for long-term financial planning because it protects the homeowner against future inflation.

An Adjustable-Rate Mortgage (ARM), however, usually offers a lower “teaser” rate for an initial period (typically 5, 7, or 10 years). After this period, the rate adjusts based on market indices. The average rate for a 5/1 ARM is almost always lower than the 30-year fixed rate because the borrower is taking on the risk of future rate hikes. For a short-term investor who plans to sell the property within five years, an ARM can be a superior financial strategy, offering lower monthly costs and higher cash flow.

15-Year vs. 30-Year Terms

When comparing averages, the 15-year fixed-rate mortgage consistently sits lower than its 30-year counterpart. From a lender’s perspective, a 15-year loan is less risky because the principal is paid down much faster, and there is less time for the borrower’s financial situation to deteriorate. For the borrower, while the monthly payments are higher due to the shorter amortization schedule, the total interest paid over the life of the loan is drastically reduced. Choosing a 15-year mortgage is a common tactic for high-net-worth individuals looking to build equity rapidly.

Strategies to Secure a Below-Average Rate

Securing a mortgage rate that is lower than the national average requires a proactive approach to financial management. It is not merely about timing the market, but about positioning your finances to be “rate-ready.”

The Concept of Buying Points

One of the most effective tools for reducing an interest rate is the purchase of “discount points.” One point typically costs 1% of the total loan amount and generally reduces the interest rate by 0.25%.

This is an upfront investment in your future financial stability. To determine if this is a wise move, a borrower must perform a break-even analysis. By dividing the cost of the points by the monthly savings on the mortgage payment, you can determine how many months you need to stay in the home to recoup the investment. If you plan to keep the home for twenty years, paying for points can yield a massive return on investment.

Comparison Shopping and Lender Overlays

The “average” rate is often a composite of many different lenders, from large commercial banks to small credit unions and online mortgage fintechs. Not all lenders use the same criteria; some have “overlays,” which are additional requirements on top of standard federal guidelines.

By obtaining “Loan Estimates” from at least three different lenders, a borrower can leverage competition. In many cases, a lender will match or beat a competitor’s rate to win the business of a well-qualified borrower. In the world of business finance, this is known as competitive bidding, and it is just as effective in personal mortgage shopping as it is in corporate procurement.

The Long-Term Financial Impact of Interest Rates

To truly understand what an average mortgage interest rate represents, one must look at the math of amortization. On a $400,000 loan, the difference between a 4% and a 6% interest rate is roughly $500 per month. Over 30 years, that 2% difference results in an additional $180,000 in interest payments.

When interest rates are high, the “average” can feel like a barrier to entry. However, real estate is a long-term asset. Savvy investors often utilize a “refinance strategy,” purchasing a home at a higher current average with the intention of refinancing into a lower rate when the economic cycle shifts.

In conclusion, the average mortgage interest rate is a benchmark—a snapshot of the current economic climate and the collective risk appetite of the financial markets. By understanding the levers that move this average, from the Federal Reserve’s policies to the specifics of your own credit profile, you can navigate the mortgage market not just as a consumer, but as a sophisticated financial strategist. Whether you are looking for your first home or adding to an investment portfolio, the rate you secure today will define your financial trajectory for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.