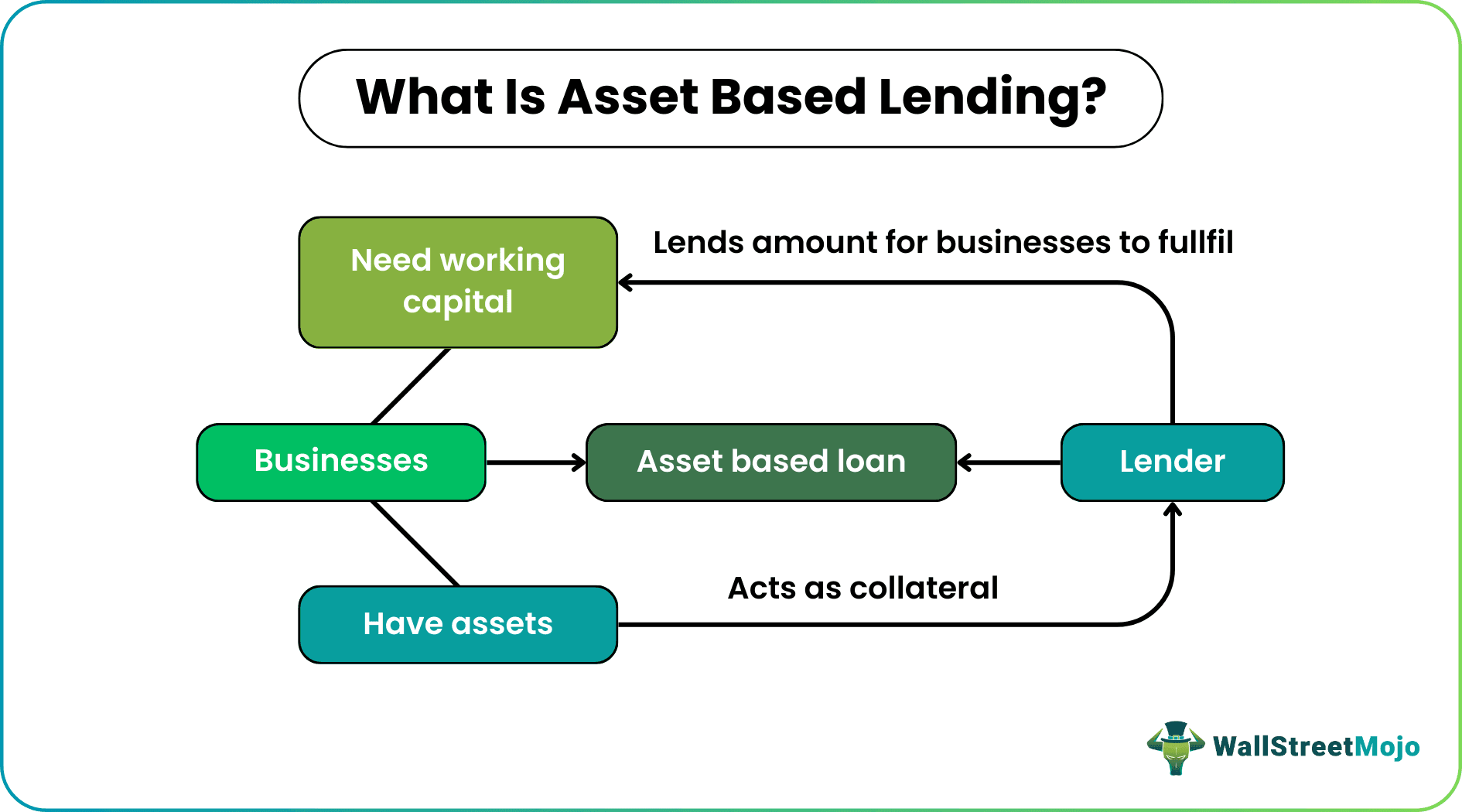

Asset-based lending (ABL) is a powerful financial tool that offers businesses a flexible and often substantial source of capital by leveraging their existing assets. Unlike traditional term loans or lines of credit that primarily rely on a company’s creditworthiness and historical cash flow, ABL arrangements treat a business’s tangible and intangible assets as the primary collateral securing the loan. This fundamental difference opens up unique avenues for financing, particularly for companies that may not qualify for conventional lending due to their stage of growth, industry, or cyclical cash flow patterns.

The core principle of an asset-based loan is straightforward: the lender provides capital based on a percentage of the value of specific assets owned by the borrower. These assets act as security, reducing the lender’s risk and allowing them to offer higher loan amounts than might otherwise be available. This makes ABL an attractive option for businesses seeking working capital, expansion funds, or even bridge financing during periods of transition or rapid growth.

Understanding the intricacies of ABL is crucial for any business owner or financial manager considering this financing method. It involves a nuanced approach to asset valuation, collateral management, and ongoing monitoring by the lender. While offering significant advantages, it also requires a clear understanding of its structure, benefits, drawbacks, and the types of businesses that can best utilize it.

The Mechanics of Asset-Based Lending

At its heart, asset-based lending functions by providing businesses with access to funds that are directly tied to the value of their underlying assets. This approach fundamentally shifts the focus of lending from a company’s profitability to the realizable value of its possessions. The process typically involves several key components that define how the loan is structured and managed.

Asset Valuation and Eligibility

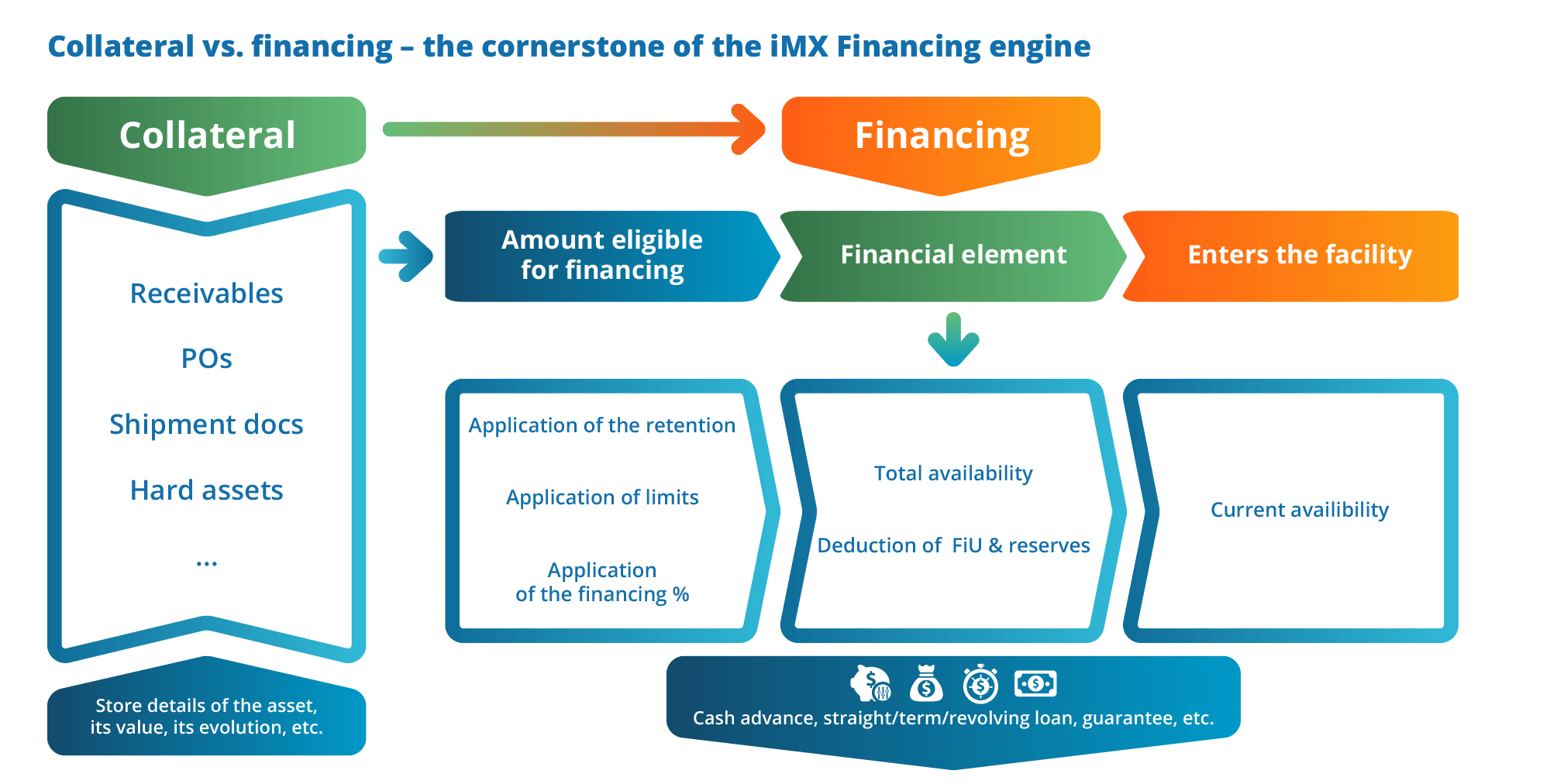

The cornerstone of any ABL facility is the rigorous assessment of the assets that will serve as collateral. Lenders employ a conservative valuation methodology, often referred to as a “borrowing base,” which determines the maximum amount that can be borrowed against those assets. Not all assets are treated equally, and the eligibility and valuation of each asset class are critical.

- Accounts Receivable (AR): This is perhaps the most common and liquid asset used in ABL. Lenders will typically advance a percentage (e.g., 80-90%) of eligible accounts receivable, with eligibility often determined by factors such as the age of the invoice, the creditworthiness of the customer, and whether the invoice is disputed. Only “current” AR, usually within 30-90 days of the due date, is typically considered.

- Inventory: The value of inventory can also be a significant component of the borrowing base. However, lenders are more cautious with inventory due to its potential for obsolescence, seasonality, or damage. They typically advance a lower percentage (e.g., 50-75%) of the cost or market value, and specific types of inventory (e.g., raw materials, finished goods) may be valued differently. Obsolete, slow-moving, or highly specialized inventory may be excluded entirely.

- Machinery and Equipment: For businesses with substantial fixed assets, machinery and equipment can serve as collateral. Valuation here is based on depreciated book value or appraised market value, with a loan-to-value ratio typically ranging from 60-80%. The condition, age, and specialized nature of the equipment will influence its valuation.

- Real Estate: While less common as the sole collateral in a typical ABL facility (which often focuses on current assets), commercial real estate owned by the business can be included in the borrowing base, usually at a lower advance rate.

- Other Assets: In some cases, other assets like marketable securities, intellectual property, or even specific contractual rights might be considered, though these are generally more complex to value and collateralize.

The lender will typically conduct thorough due diligence, including appraisals and audits, to verify the existence, ownership, and condition of the collateral. The borrowing base is not static; it fluctuates as the value of the underlying assets changes.

The Borrowing Base Calculation

The borrowing base is the dynamic ceiling on the amount a business can borrow at any given time. It is calculated by taking the eligible value of each asset category and applying the lender’s advance rate.

Borrowing Base = (Eligible AR x Advance Rate for AR) + (Eligible Inventory x Advance Rate for Inventory) + (Eligible Machinery & Equipment x Advance Rate for M&E) + …

For example, if a company has $1 million in eligible accounts receivable and the lender advances 85%, that component contributes $850,000 to the borrowing base. If they have $500,000 in eligible inventory with a 60% advance rate, that adds $300,000. The total borrowing base would then be $1.15 million. The actual loan amount available will be a percentage of this borrowing base, often a bit lower to provide a buffer for the lender.

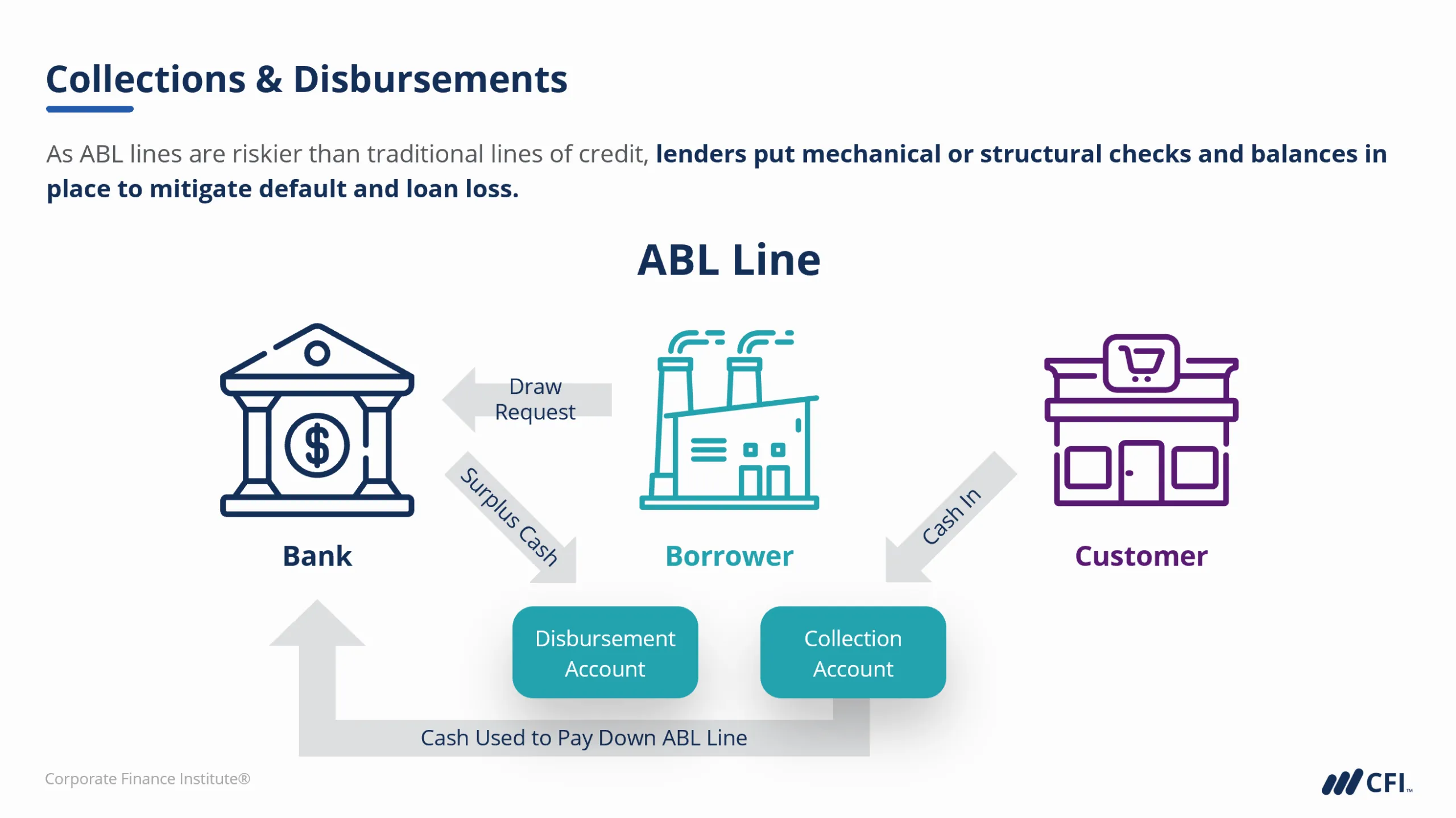

Collateral Management and Reporting

A critical aspect of ABL is the ongoing management and reporting of the collateral. Borrowers are typically required to provide regular reports to the lender, detailing their accounts receivable aging, inventory levels, and other relevant asset information. This allows the lender to monitor the borrowing base and ensure the collateral remains sufficient to support the loan.

- Accounts Receivable Reporting: Businesses must provide detailed AR aging reports, listing individual customer balances, invoice dates, and payment status.

- Inventory Reporting: Periodic physical inventory counts and valuations are often required, along with reports on inventory turnover and obsolescence.

- Field Exams: Lenders may conduct periodic “field exams,” which are in-depth audits of the company’s financial records and physical collateral to verify accuracy and assess risk.

This continuous oversight is fundamental to the asset-based lending model, providing the lender with real-time visibility into the value and condition of their security.

Benefits of Asset-Based Loans

Asset-based lending offers a distinct set of advantages that can be particularly impactful for businesses facing specific financial needs or growth opportunities. Its flexibility and capacity to unlock capital from a company’s balance sheet make it a strategic financial tool.

Enhanced Liquidity and Working Capital

One of the most significant benefits of ABL is its ability to unlock substantial working capital. Many growing businesses, especially those in industries with long production cycles or seasonal sales, can experience cash flow gaps. ABL provides a mechanism to convert illiquid assets, like inventory and accounts receivable, into readily available cash. This improved liquidity allows businesses to:

- Meet Payroll and Operating Expenses: Ensure smooth day-to-day operations without the stress of cash shortages.

- Take Advantage of Supplier Discounts: Offer early payment discounts to suppliers, which can lead to cost savings.

- Invest in Growth Opportunities: Fund new projects, marketing campaigns, or research and development without waiting for sales to generate cash.

- Manage Seasonal Fluctuations: Bridge periods of low sales or high inventory accumulation with readily accessible funds.

The fact that the loan amount is tied to asset value, rather than solely credit history, means that businesses with strong collateral but perhaps a less established credit record can still qualify for significant funding.

Flexibility and Scalability

ABL facilities are inherently flexible and scalable, adapting to the changing needs and asset levels of the business. As a company’s accounts receivable or inventory grows, its borrowing base increases, potentially allowing for larger loan amounts. Conversely, if asset levels decrease, the borrowing capacity also adjusts. This dynamic nature is a stark contrast to fixed-term loans.

- Adaptability to Business Cycles: The ability to draw more funds when sales are high and assets are abundant, and less when they are low, aligns perfectly with the ebb and flow of many businesses.

- Accommodating Growth: Rapidly growing companies can use ABL to fund their expansion without needing to undergo repeated loan application processes.

- Tailored Structures: Lenders can often structure ABL facilities to accommodate unique business models and asset types, offering a more customized solution than traditional lending products.

This adaptability makes ABL a powerful tool for businesses that experience significant growth, seasonality, or volatility.

Access to Capital for Underserved Businesses

ABL can be a lifeline for businesses that may not qualify for traditional bank loans. This includes:

- Startups and Early-Stage Companies: Businesses with limited operating history or profitability may still have valuable assets that can be collateralized.

- Companies in Cyclical Industries: Businesses in sectors like manufacturing, wholesale, or retail, which often have high inventory levels and fluctuating sales, can benefit from the ABL structure.

- Companies Undergoing Turnarounds or Restructuring: Businesses in distress may find that their assets can still be leveraged to provide the necessary capital for recovery and reorganization.

- Companies with Limited Credit History: For businesses that haven’t had the opportunity to build a strong credit score, ABL provides an alternative pathway to financing based on tangible assets.

By focusing on the value of collateral, ABL lenders are often more willing to take on a certain level of risk that traditional lenders might avoid.

Potential Drawbacks and Considerations

While asset-based lending offers significant advantages, it’s not without its complexities and potential downsides. Businesses considering ABL must be aware of these aspects to ensure it’s the right fit for their financial strategy and operational capabilities.

Higher Costs and Fees

Asset-based loans typically come with higher interest rates and a more complex fee structure compared to traditional bank loans. This reflects the increased risk undertaken by the lender, the administrative burden of monitoring collateral, and the specialized expertise required for ABL.

- Interest Rates: Rates are often expressed as a spread over a benchmark rate (like the prime rate or LIBOR/SOFR) and can be several percentage points higher than those for conventional loans.

- Fees: Borrowers may encounter various fees, including:

- Origination fees: Charged at the inception of the loan.

- Servicing fees: For ongoing management of the loan and collateral.

- Audit fees: For field exams and collateral verification.

- Monitoring fees: For the lender’s oversight of the borrowing base.

- Waiver fees: If the borrower requests an exception to certain loan covenants.

These costs can add up and should be factored into the overall cost of capital analysis.

Stringent Covenants and Reporting Requirements

The collateral-monitoring aspect of ABL leads to more stringent covenants and reporting obligations for the borrower. Lenders need to maintain close control over the assets, which translates into demanding requirements for the borrower.

- Detailed Reporting: As mentioned previously, borrowers must provide frequent and detailed reports on their accounts receivable, inventory, and other collateral. Failure to do so can lead to a default.

- Restrictions on Asset Sales: Selling or disposing of assets that serve as collateral may require lender consent or be subject to specific procedures outlined in the loan agreement.

- Performance Covenants: While ABL focuses on collateral, lenders may still impose performance covenants related to financial ratios, such as minimum tangible net worth or maximum debt-to-equity ratios, to ensure the overall financial health of the business.

- Operational Scrutiny: The lender’s ongoing monitoring can sometimes feel intrusive, as they are deeply involved in understanding the operational flow of the business as it relates to collateral management.

Adhering to these requirements necessitates strong internal financial controls and a commitment to transparency.

Potential for Misalignment and Control Issues

The close oversight by an ABL lender can, in some instances, lead to misalignment in strategic decision-making or create a sense of diminished control for the business owner.

- Pace of Decision-Making: The need for lender approval for certain asset-related transactions can slow down the pace of business operations or strategic initiatives.

- Focus on Collateral: The lender’s primary concern is the value of the collateral. This focus might sometimes diverge from the borrower’s broader strategic goals, especially if those goals involve divesting certain assets or undertaking activities that the lender perceives as increasing risk to their collateral.

- Risk of Default: The dynamic nature of the borrowing base and the stringent reporting requirements mean that businesses can inadvertently breach loan covenants if their asset management or reporting falters, potentially leading to a default even if the underlying business is otherwise performing well.

Businesses must be prepared for a more collaborative, and at times, constrained relationship with their ABL lender, where open communication and proactive management are paramount.

When is an Asset-Based Loan the Right Choice?

The decision to pursue an asset-based loan hinges on a business’s specific circumstances, financial needs, and its ability to leverage its assets effectively. ABL is not a one-size-fits-all solution but rather a strategic financial instrument best suited for certain situations.

Businesses with Significant Tangible Assets

The most obvious candidates for ABL are businesses that possess substantial amounts of tangible assets that can be readily valued and collateralized. This typically includes:

- Manufacturing Companies: With significant investments in machinery, equipment, and raw materials or finished goods inventory.

- Wholesale Distributors: Holding large inventories of goods for sale.

- Retailers: With substantial inventory on hand and accounts receivable from credit customers.

- Companies with Strong Accounts Receivable Portfolios: Businesses that have a consistent stream of receivables from creditworthy customers.

- Resource-Based Industries: Such as those involved in commodities or extraction, where raw materials and equipment are key assets.

These companies can unlock a significant portion of their balance sheet’s value through ABL, providing capital that might be unavailable through other means.

Businesses Seeking Growth Capital or Expansion Funding

ABL is an excellent tool for businesses aiming to accelerate their growth. When a company needs capital for expansion, such as acquiring new equipment, increasing inventory to meet demand, or funding larger orders, ABL can provide the necessary working capital.

- Orderly Growth: It allows businesses to finance the expansion of their asset base in line with growing sales and operational needs.

- Bridging Investment Gaps: Companies investing heavily in new fixed assets or expanding inventory might experience a temporary cash flow crunch. ABL can bridge this gap until the new assets generate revenue or the inventory is sold.

- Mergers and Acquisitions: ABL can provide crucial funding for acquisitions, allowing a company to leverage its existing assets to finance the purchase of another business.

The ability to scale borrowing with the growth of assets makes ABL ideal for dynamic expansion plans.

Businesses Experiencing Cash Flow Challenges or Turnarounds

For companies facing temporary cash flow difficulties, seasonal downturns, or undergoing a turnaround, ABL can be a critical lifeline.

- Working Capital Enhancement: It can provide the necessary liquidity to manage operations, meet payroll, and service debt during periods of reduced sales or delayed customer payments.

- Reorganization and Restructuring: In situations of financial distress, ABL can provide the capital needed to stabilize operations, fund restructuring efforts, or bridge the gap until a more permanent solution is found.

- Avoiding Insolvency: By providing access to funds when traditional lenders might withdraw support, ABL can help businesses avoid insolvency and achieve a successful recovery.

The key here is that the business still possesses valuable assets that can be leveraged, even if current profitability is impaired.

In conclusion, asset-based lending is a versatile and powerful financing option that offers a unique pathway to capital for a wide range of businesses. By understanding its mechanics, benefits, and potential drawbacks, business leaders can strategically employ ABL to enhance liquidity, fuel growth, and navigate financial challenges, ultimately contributing to the long-term health and success of their enterprise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.