In the world of finance, clarity is the most valuable currency. Whether you are a small business owner, an aspiring investor, or a corporate executive, the way you record and interpret financial data dictates the quality of your decision-making. At the heart of professional financial management lies a concept that often confuses beginners but provides the most accurate picture of economic reality: accrual.

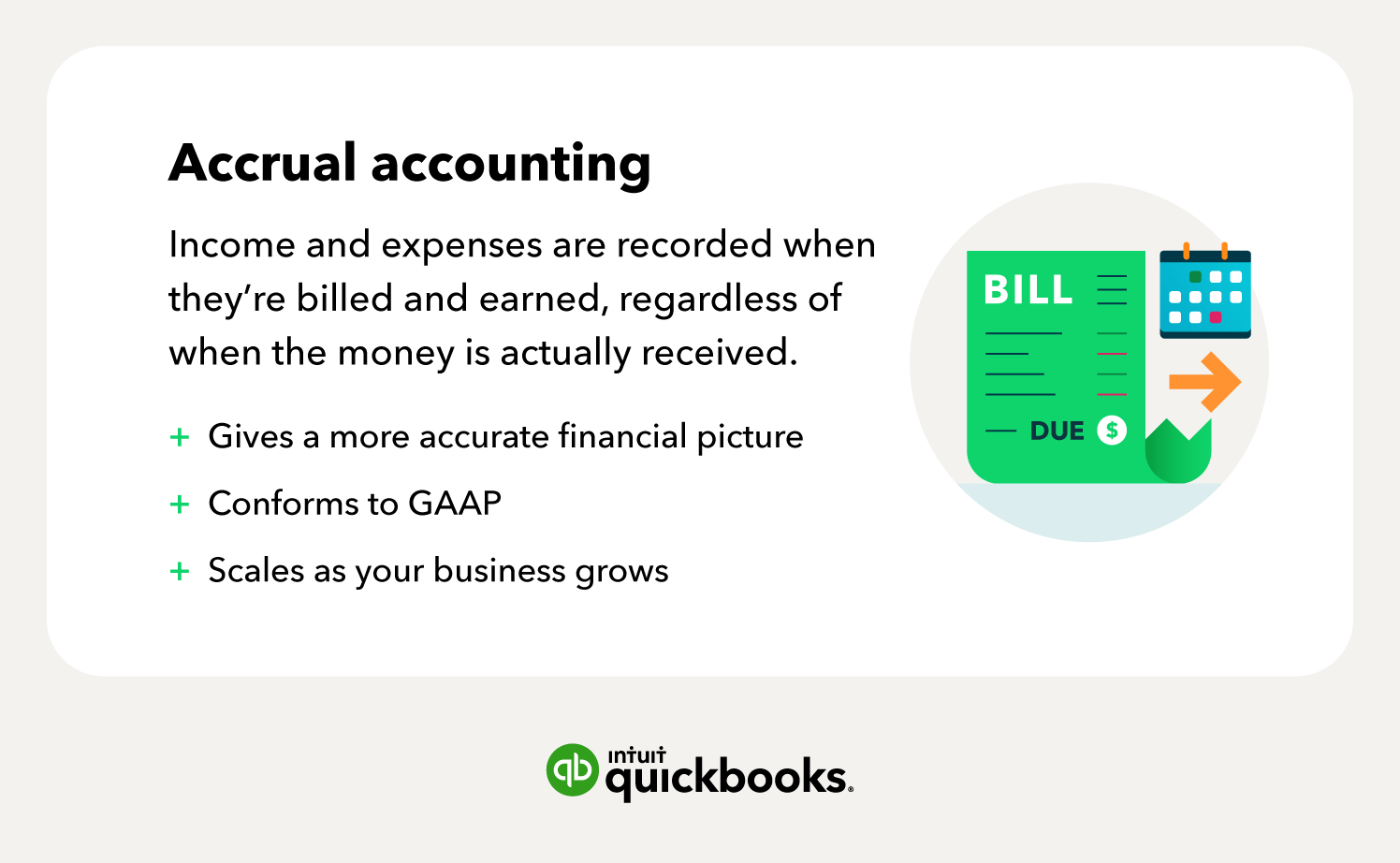

Accrual is an accounting method that records revenues and expenses when they are earned or incurred, regardless of when the actual cash changes hands. While simple cash-based accounting works for a personal checkbook or a child’s lemonade stand, the complexities of modern business demand a more sophisticated approach. Accrual accounting bridges the gap between a transaction and its ultimate settlement, ensuring that a company’s financial statements reflect its true performance over a specific period.

The Core Concept: Accrual vs. Cash Accounting

To master the concept of accrual, one must first understand its counterpart: cash basis accounting. These two methods represent the two primary ways organizations track their financial health, but they offer vastly different perspectives on the same events.

How Accrual Accounting Works

Accrual accounting is built on the premise of economic events rather than physical cash movement. If you provide a service to a client in December but don’t receive the payment until January, accrual accounting requires you to record that revenue in December. Why? Because that is when the work was performed and the “economic value” was created. Similarly, if you receive a utility bill for electricity used in August but pay it in September, the expense belongs in August’s records. This method ensures that the financial statements for a specific month or year tell the full story of what happened during that time.

The Matching Principle: Why Timing Matters

The cornerstone of accrual accounting is the “Matching Principle.” This principle dictates that expenses should be matched with the revenues they helped generate. Imagine a manufacturer that spends $10,000 on raw materials in March to create products that are sold in April for $20,000. Under cash accounting, March would look like a massive loss, and April would look like a massive gain. Under accrual accounting, the $10,000 cost is “matched” against the $20,000 revenue in April. This provides a clear view of the profit margin and prevents the “lumpy” financial reporting that makes long-term planning difficult.

Key Differences: A Comparative Look

The primary difference lies in timing. Cash accounting is immediate and simple; it tracks the bank account. Accrual accounting is comprehensive and forward-looking; it tracks obligations. While cash accounting is easier for tax purposes for very small businesses, accrual accounting is required for any business that carries inventory or exceeds certain revenue thresholds set by regulatory bodies. It allows for a more “smoothed” view of operations, removing the noise of delayed payments and early deposits.

Accrual in Action: Revenue and Expenses

To see how accrual functions in a professional setting, we must look at the two sides of the ledger: what the business is owed and what the business owes. These are categorized as accrued revenue and accrued expenses.

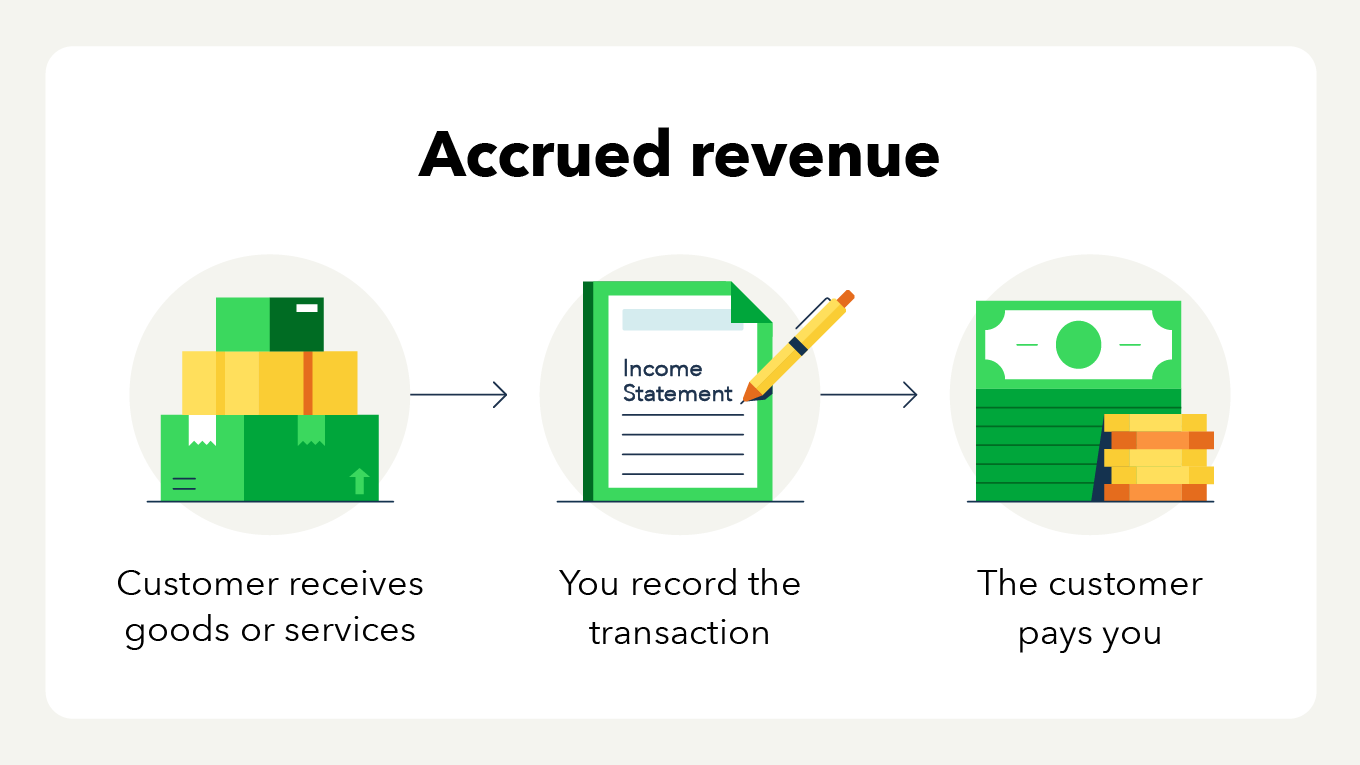

Accrued Revenue: Earning Without the Cash

Accrued revenue occurs when a company has fulfilled its performance obligations but has not yet billed the customer or received payment. This is common in service-based industries. For example, a consulting firm might work on a three-month project. At the end of month one, they have earned one-third of the fee, even if the contract states they won’t invoice until the project is complete. In an accrual system, that one-third is recorded as “Accrued Revenue” (an asset on the balance sheet) and “Service Revenue” (on the income statement). This prevents the firm’s books from looking empty during the months of active labor.

Accrued Expenses: Obligations Before Payment

On the flip side, accrued expenses are costs that a business has incurred but not yet paid. A classic example is employee wages. If the work week ends on Friday, June 30th, but the employees aren’t paid until Friday, July 7th, the company still owes for those last few days of June. To accurately reflect the expenses of June, the accountant will record an “Accrued Expense” entry. Other common examples include interest on loans that builds up over time and taxes that are calculated throughout the year but paid quarterly or annually.

Real-World Business Examples

Consider a subscription-based software company (SaaS). When a customer pays $1,200 for an annual subscription in January, the company cannot claim all $1,200 as revenue immediately. Instead, they record $100 each month as they provide the service. The remaining balance is held as “deferred revenue.” Conversely, if a construction company uses heavy machinery in October but receives the repair bill in November, they must “accrue” that repair cost in October to ensure the monthly profit report is accurate. These adjustments ensure that stakeholders see the actual operational costs of doing business.

Why Accrual Matters for Business Growth and Strategy

For investors and business leaders, accrual accounting is not just a technical requirement; it is a strategic tool. It provides the “big picture” that cash accounting obscures, allowing for more precise forecasting and risk management.

Providing a True Picture of Financial Health

If a company only used cash accounting, it could look incredibly successful simply by delaying the payment of its bills. Conversely, a highly profitable company might look like it’s failing if it just made a massive investment in inventory that hasn’t sold yet. Accrual accounting strips away these timing distortions. It reveals the underlying profitability of a business’s core activities. When a CEO looks at an accrual-based income statement, they see the efficiency of their operations, not just the current state of the company’s checking account.

Navigating Complex Financial Cycles

Many businesses operate on seasonal cycles. A retailer may spend millions on inventory in the summer to prepare for the holiday season. If they relied on cash accounting, their summer months would show devastating losses, and their winter months would show unrealistic profits. Accrual accounting allows management to see the “cost of goods sold” (COGS) precisely when the sales happen. This enables better inventory management, more accurate pricing strategies, and more effective resource allocation throughout the year.

Investor and Creditor Requirements

If you ever intend to seek venture capital, take out a significant business loan, or take a company public, accrual accounting is non-negotiable. Investors want to see the “run rate” of a business. They want to know the revenue growth trends and the “burn rate” of expenses. Because accrual accounting follows standardized rules, it allows investors to compare Company A with Company B on an apples-to-apples basis. Creditors, meanwhile, use accrual-based balance sheets to determine a company’s “liquidity” and “solvency”—essentially, whether the company has the assets (like accounts receivable) to cover its long-term liabilities.

Managing Accruals: Tools, Best Practices, and Compliance

Implementing an accrual system requires more diligence than a cash system. It necessitates a structured approach to record-keeping and a reliance on modern financial technology.

Leveraging Financial Software for Accuracy

Manually tracking accruals is a recipe for error. Modern financial tools and ERP (Enterprise Resource Planning) systems automate much of this process. Software like QuickBooks, Xero, or NetSuite can automatically generate recurring accrual entries and track “Accounts Receivable” (AR) and “Accounts Payable” (AP). These tools provide real-time dashboards that show “Earned Revenue” versus “Cash on Hand,” giving managers a dual-lens view of their financial position at any given moment.

Adjusting Entries and the Closing Process

The “Closing of the Books” is a monthly or annual ritual in accrual accounting. During this period, accountants make “adjusting entries.” These entries account for things like depreciation (spreading the cost of a large purchase over its useful life) and bad debt expense (accounting for the reality that some customers may never pay their bills). This rigorous process ensures that by the time a financial report is issued, every penny of revenue and expense has been assigned to its proper timeframe.

Regulatory Standards (GAAP and IFRS)

In the United States, the Generally Accepted Accounting Principles (GAAP) set the standard for accrual accounting. Internationally, the International Financial Reporting Standards (IFRS) serve a similar purpose. Following these standards is vital for legal compliance and financial integrity. These frameworks provide specific rules on “Revenue Recognition”—exactly when a company is allowed to say they’ve “earned” money. For instance, recent updates to GAAP (specifically ASC 606) have changed how companies across all industries must account for contracts with customers, emphasizing the importance of staying current with accrual regulations.

Conclusion: Mastering Accrual for Long-Term Financial Success

Accrual accounting is the language of professional finance. While it requires more effort to maintain than a simple cash-in, cash-out system, the insights it provides are indispensable. By decoupling the timing of cash from the timing of economic value, accrual accounting allows for a sophisticated understanding of profit, loss, and long-term sustainability.

For the modern business leader or investor, understanding “what is accrual” is the first step toward financial literacy. It moves the focus away from the volatility of the bank balance and toward the stability of earned value. Whether you are managing a growing startup or analyzing a portfolio of stocks, viewing the world through the lens of accrual ensures that you are making decisions based on the most accurate, transparent, and comprehensive financial data available. In the end, mastering accruals is about more than just keeping books; it is about mastering the reality of your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.