In the vast and dynamic landscape of the global economy, the term “small business” is frequently used, yet its precise definition and profound significance are often underappreciated. Far from being a monolithic entity, a small business represents a diverse array of ventures that form the bedrock of local economies, drive innovation, and serve as crucial engines of job creation. To truly grasp what constitutes a small business is to delve beyond simplistic notions of size and revenue, exploring the intricate financial, operational, and strategic nuances that define these enterprises and underscore their vital role in prosperity.

This article will meticulously unpack the concept of a small business, examining the quantitative and qualitative factors that distinguish it, highlighting its immense financial and economic contributions, and exploring the unique financial realities and management challenges inherent to its operation. By the end, readers will possess a comprehensive understanding of what truly defines a small business in the modern financial world.

Defining Small Business: More Than Just Size

While the label “small” immediately suggests a limited scale, the official and practical definitions of a small business are far more sophisticated, often varying by industry, government body, and economic context. It’s a definition that blends objective metrics with subjective characteristics to paint a complete picture.

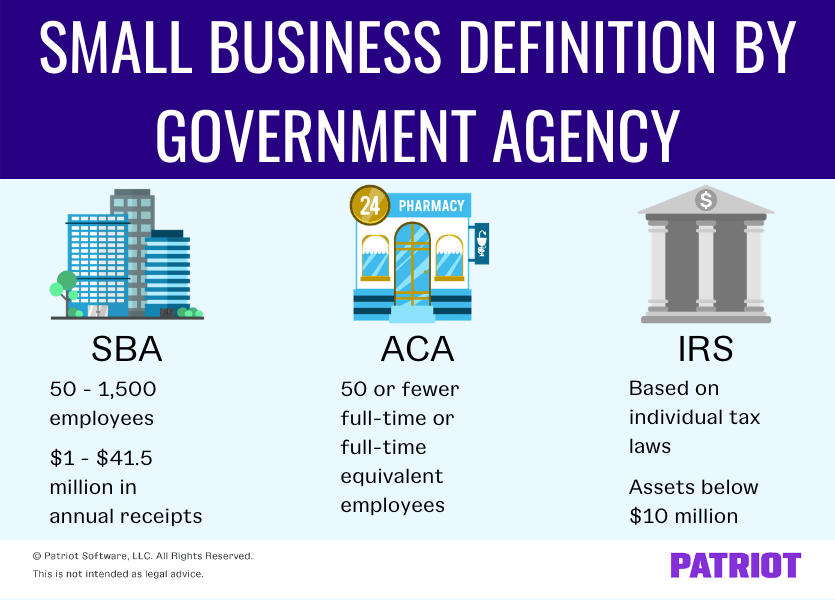

Quantitative Metrics: The SBA’s Benchmark

In the United States, the most authoritative definition often comes from the Small Business Administration (SBA). The SBA establishes size standards that are crucial for determining eligibility for federal contracts, loans, and other support programs. These standards are not universal but are instead tailored to specific industries.

Typically, the SBA uses two primary quantitative metrics:

- Employee Count: For many industries, a business is considered small if it has fewer than a certain number of employees. This threshold can range dramatically, from 100 employees for some manufacturing sectors to 1,500 employees for certain electric utility companies. Professional services, for instance, might cap at 500 employees.

- Annual Revenue: For other industries, particularly in retail trade, services, or finance, the determining factor is average annual receipts (revenue). These thresholds also vary widely, from around $1 million for certain agricultural services to over $40 million for some wholesale trade sectors.

These varying thresholds underscore a critical point: “small” is relative. A small manufacturing firm is likely much larger in terms of employees and assets than a small consulting firm, yet both are vital components of their respective economic ecosystems and qualify for similar support mechanisms due to their “small” classification within their industry.

Qualitative Characteristics: Beyond the Numbers

Beyond these hard numbers, several qualitative characteristics often distinguish small businesses, impacting their financial structure and operational strategy:

- Independent Ownership and Operation: Small businesses are typically owned and operated by individuals or a small group, with control generally residing with the founders or a limited number of investors. This contrasts with large corporations, which often have dispersed ownership among shareholders.

- Localized Operations: While not always true in the digital age, many small businesses serve a local or regional market, fostering direct relationships with their customer base and contributing directly to the local economy.

- Limited Market Share: By definition, a small business does not dominate its industry or market sector. It operates within a competitive landscape alongside other small and large players.

- Agility and Adaptability: Often, small businesses are more nimble and able to pivot quickly in response to market changes or customer feedback, a significant financial advantage when facing rapidly evolving consumer demands.

- Personalized Service: The financial model of many small businesses relies heavily on building strong customer relationships, offering personalized service that larger, more impersonal corporations may struggle to provide.

Differentiating from Micro-Businesses and Startups

It’s also important to distinguish small businesses from related terms. A micro-business is typically a subset of a small business, characterized by very few employees (often fewer than 10) and minimal capital, such as a sole proprietorship or a very small family-run operation. A startup, while often small in its initial phase, is primarily defined by its intention for rapid growth and scalability, often driven by innovative technology or business models with the aim of eventually becoming a large enterprise or being acquired. Not all small businesses are startups, and not all startups remain small businesses; many are content to serve a niche and grow organically within their existing scale.

The Economic Engine: Why Small Businesses Matter Financially

The collective financial contribution of small businesses to national and global economies is nothing short of immense. They are not merely passive participants but active drivers of economic vitality, resilience, and progress.

Job Creation and Local Economies

One of the most profound financial impacts of small businesses is their role in job creation. In the U.S., small businesses are responsible for creating nearly two-thirds of net new jobs annually. These jobs provide income for millions of households, stimulating consumer spending and tax revenues. By hiring locally, small businesses recirculate money within their communities, bolstering local economies. Every wage paid, every supply purchased from another local vendor, and every profit reinvested contributes directly to the financial health of neighborhoods, towns, and cities. This local economic multiplier effect is a cornerstone of regional prosperity.

Innovation and Competition

Small businesses are often hotbeds of innovation, bringing new products, services, and business models to market. Without the rigid structures of large corporations, they can experiment more freely, taking calculated financial risks that can lead to breakthroughs. This spirit of innovation fuels competition, which is financially beneficial for consumers, driving down prices, increasing quality, and expanding choice. A market dominated solely by large corporations risks stagnation and higher prices; small businesses provide the dynamism needed to keep economies vibrant and competitive.

Economic Resilience and Diversification

In times of economic uncertainty, a diverse array of small businesses can provide a crucial buffer. An economy heavily reliant on a few large industries is vulnerable to sector-specific downturns. Small businesses, spread across various sectors—from retail and services to manufacturing and tech—diversify the economic base, making it more resilient to shocks. They also offer diverse income streams for individuals, fostering entrepreneurship and providing alternatives to traditional employment, which is a powerful tool for financial stability at both individual and societal levels.

Financial Realities and Management for Small Businesses

Operating a small business involves a distinct set of financial realities and management challenges. Success hinges on a robust understanding and adept handling of these monetary aspects.

Funding and Capital Access

One of the primary financial hurdles for many small businesses is securing adequate funding. Unlike large corporations with established credit lines and access to public markets, small businesses often rely on a variety of sources:

- Bootstrapping: Using personal savings and initial revenue to fund operations, minimizing debt and external equity dilution.

- Bank Loans: Traditional financing, often requiring collateral and a solid business plan.

- Government-Backed Loans: Programs like those offered by the SBA (e.g., 7(a) loans) reduce risk for lenders, making capital more accessible to small businesses.

- Venture Capital and Angel Investors: For high-growth potential businesses, these equity investors provide significant capital in exchange for ownership stakes.

- Crowdfunding: Raising small amounts of capital from a large number of individuals, often through online platforms.

- Grants: Specific funds provided by governments or foundations, usually for businesses meeting certain criteria (e.g., innovation, social impact).

Managing the debt-to-equity ratio, understanding interest rates, and forecasting repayment capabilities are critical financial management skills for small business owners.

Cash Flow Management: The Lifeblood of Small Business

Perhaps no financial concept is more critical to a small business than cash flow. Profitability is essential, but a profitable business can still fail if it runs out of cash. Small businesses often face unpredictable revenue streams and delays in payment from customers, while expenses like rent, payroll, and inventory are constant.

Effective cash flow management involves:

- Monitoring Inflows and Outflows: Tracking every dollar entering and leaving the business.

- Cash Flow Forecasting: Predicting future cash positions to identify potential shortfalls or surpluses.

- Managing Accounts Receivable: Prompt invoicing and diligent follow-up on overdue payments.

- Managing Accounts Payable: Strategically timing payments to suppliers without damaging relationships.

- Establishing a Cash Reserve: Maintaining an emergency fund to cover unexpected expenses or lean periods.

Poor cash flow management is a leading cause of small business failure, making it a central pillar of financial strategy.

Financial Planning and Budgeting

Strategic financial planning is paramount for small businesses to achieve their goals. This involves:

- Setting Financial Goals: Defining clear, measurable objectives for revenue, profit margins, and growth.

- Budgeting: Creating detailed plans for allocating financial resources over a specific period, controlling expenses, and ensuring funds are available for critical operations and investments.

- Forecasting: Predicting future financial performance based on historical data and market trends, allowing for proactive adjustments.

- Understanding Key Financial Statements: Regularly reviewing income statements, balance sheets, and cash flow statements to assess financial health and make informed decisions.

A well-crafted budget acts as a financial roadmap, guiding decisions on everything from hiring to inventory purchases to marketing expenditures.

Profitability and Sustainable Growth

While revenue is important, ultimate financial success for a small business lies in profitability—the ability to generate more income than expenses—and achieving sustainable growth. This requires:

- Understanding Margins: Calculating gross profit margin (revenue minus cost of goods sold) and net profit margin (the percentage of revenue left after all expenses).

- Pricing Strategy: Setting prices that cover costs, provide a reasonable profit, and remain competitive.

- Cost Control: Continuously seeking ways to reduce operating expenses without compromising quality or service.

- Strategic Reinvestment: Deciding how much profit to retain in the business for growth initiatives (e.g., new equipment, expansion, marketing) versus distributing to owners.

Sustainable growth means expanding the business at a pace that its financial resources and operational capacity can support, avoiding overextension that can lead to cash flow crises or debt spirals.

Navigating the Small Business Landscape: Challenges and Opportunities

The small business journey is fraught with challenges but also rich with opportunities, many of which have significant financial implications.

Regulatory Compliance and Taxation

Small businesses face a complex web of regulations and tax obligations, which can be a significant financial burden. Understanding and complying with federal, state, and local laws related to payroll taxes, sales tax, income tax, licenses, permits, and labor laws requires time, resources, and often professional financial advice. Non-compliance can lead to hefty fines, legal troubles, and severe financial setbacks. Proactive engagement with tax professionals and careful record-keeping are essential.

Competition and Market Positioning

Competing with larger, more established companies that benefit from economies of scale, extensive marketing budgets, and greater financial leverage is a constant challenge. Small businesses must strategically position themselves by:

- Niche Specialization: Focusing on specific markets or customer segments where they can excel.

- Value Proposition: Offering unique products, superior service, or a distinct customer experience that justifies their pricing.

- Building Brand Loyalty: Cultivating strong relationships that transcend price competition.

- Leveraging Local Advantages: Emphasizing their community roots and local appeal.

Financially, this means investing in customer retention, targeted marketing, and quality assurance to maintain competitive edge.

Leveraging Financial Tools and Resources

Fortunately, the modern financial landscape offers numerous tools and resources to help small businesses thrive:

- Accounting Software: Solutions like QuickBooks, Xero, or FreshBooks automate bookkeeping, invoicing, expense tracking, and financial reporting, providing real-time insights into financial health.

- Payment Processors: Platforms such as Square, Stripe, or PayPal simplify transaction processing, often offering integrated financial management features.

- Financial Advisors and Consultants: Professional guidance on budgeting, tax planning, investment strategies, and securing funding.

- Government Programs and Business Development Centers: Offering advice, training, and financial assistance specifically tailored for small businesses.

Embracing these tools can significantly streamline financial operations, improve decision-making, and free up valuable time for owners to focus on growth.

Conclusion

What is a small business? It is a dynamic, multifaceted entity that transcends simple definitions of size. It is a vital economic engine, a wellspring of innovation, and a cornerstone of community prosperity. Defined by a blend of quantitative metrics and qualitative characteristics, small businesses require astute financial management, from securing capital and managing cash flow to strategic planning and navigating regulatory complexities.

Despite the inherent challenges, the opportunities for growth, impact, and personal fulfillment are immense. By understanding the unique financial realities and leveraging available resources, small business owners can not only survive but thrive, continuing to contribute meaningfully to the economic fabric of societies worldwide. Their success is not just their own; it is a shared success that underpins the health and dynamism of the broader economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.