In the complex landscape of business finance and commercial lending, the term “security agreement” serves as a cornerstone for risk management and capital distribution. For entrepreneurs, small business owners, and corporate finance officers, understanding this document is not merely a legal necessity—it is a strategic imperative. At its core, a security agreement is a contractual arrangement that provides a lender with a “security interest” in a specific asset or property pledged as collateral. This ensures that if a borrower defaults on their financial obligations, the lender has a legal pathway to recover the value of the loan.

In this comprehensive guide, we will delve into the mechanics of security agreements, their essential components, and how they function within the broader financial ecosystem to facilitate the flow of credit.

1. Understanding the Core Mechanics of a Security Agreement

To grasp the importance of a security agreement, one must first understand the fundamental tension in finance: the balance between risk and reward. Lenders want to provide capital to earn interest, but they must mitigate the risk that the borrower will fail to repay. The security agreement is the primary tool used to bridge this gap.

The Legal Definition and Purpose

A security agreement is a document that provides a lender a security interest in a specified asset or property that is pledged as collateral. According to the Uniform Commercial Code (UCC) in the United States, which governs most commercial transactions, a security interest is an interest in personal property or fixtures which secures payment or performance of an obligation.

The primary purpose is to transform an “unsecured” loan into a “secured” loan. In an unsecured loan (like a standard credit card), the lender has no specific claim to any of the borrower’s assets if they stop paying. In a secured loan, the security agreement grants the lender a priority claim, allowing them to seize and sell the collateral to recoup their losses.

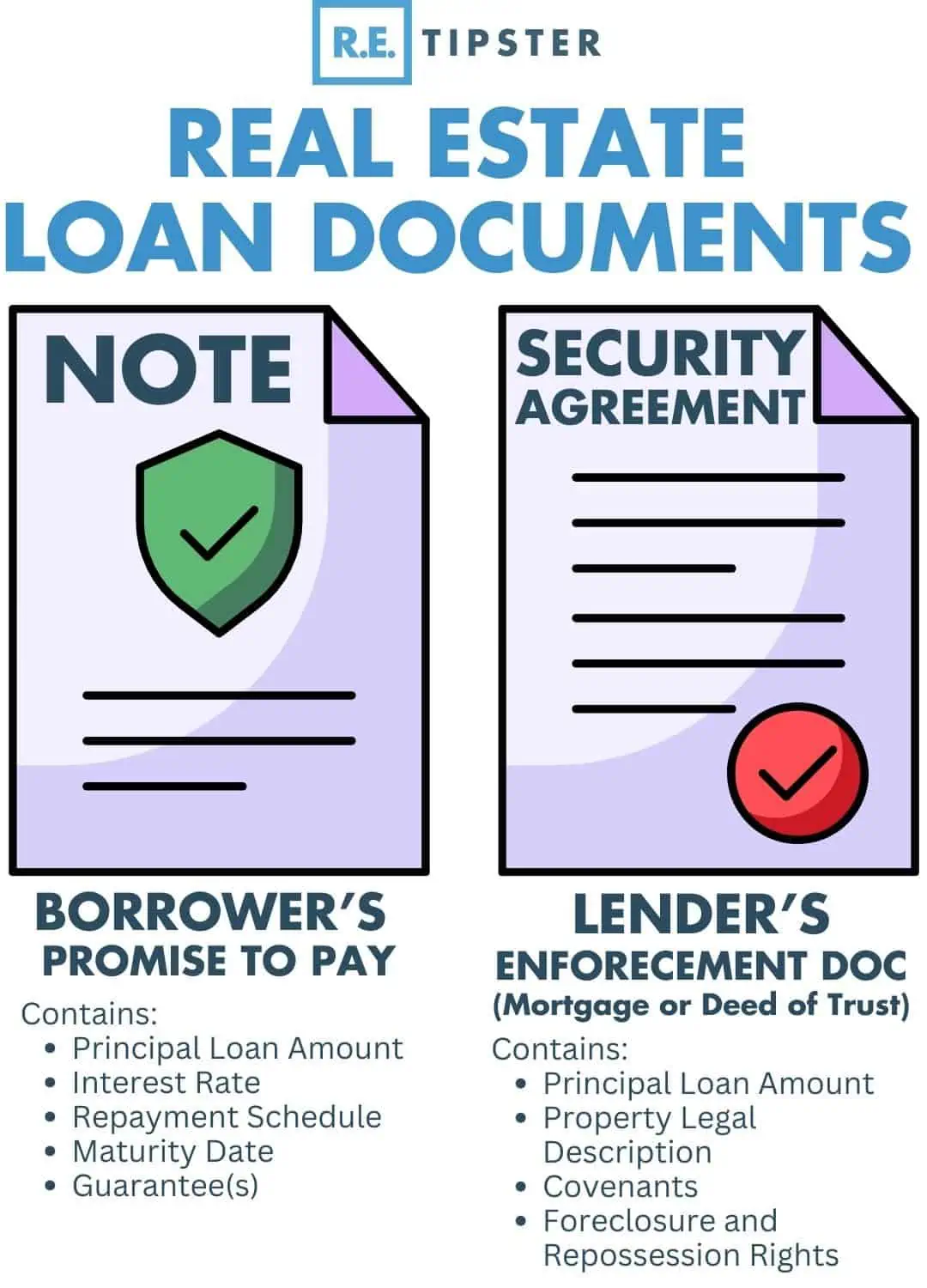

How It Differs from a Financing Statement (UCC-1)

A common point of confusion in business finance is the difference between a security agreement and a UCC-1 financing statement. While they are related, they serve distinct roles:

- The Security Agreement: This is the private contract between the lender and the borrower. It creates the security interest and outlines the terms, rights, and responsibilities of both parties.

- The UCC-1 Financing Statement: This is a public notice filed with a state’s Secretary of State or a similar regulatory body. Its purpose is to “perfect” the security interest—essentially telling the rest of the world that the lender has a legal claim to the borrower’s assets.

The Role of Collateral in Business Finance

Collateral is the “skin in the game.” By pledging assets—whether they be physical machinery, intellectual property, or future revenue—the borrower provides the lender with a safety net. This reduction in risk often leads to more favorable loan terms for the borrower, such as lower interest rates, higher borrowing limits, and longer repayment periods. Without the legal framework of a security agreement, many businesses would find it impossible to secure the financing necessary for expansion or operational stability.

2. Key Components of an Effective Security Agreement

A well-drafted security agreement must be precise. Ambiguity in these documents can lead to prolonged legal battles and financial loss. Most professional agreements contain several critical sections that define the boundaries of the lender-borrower relationship.

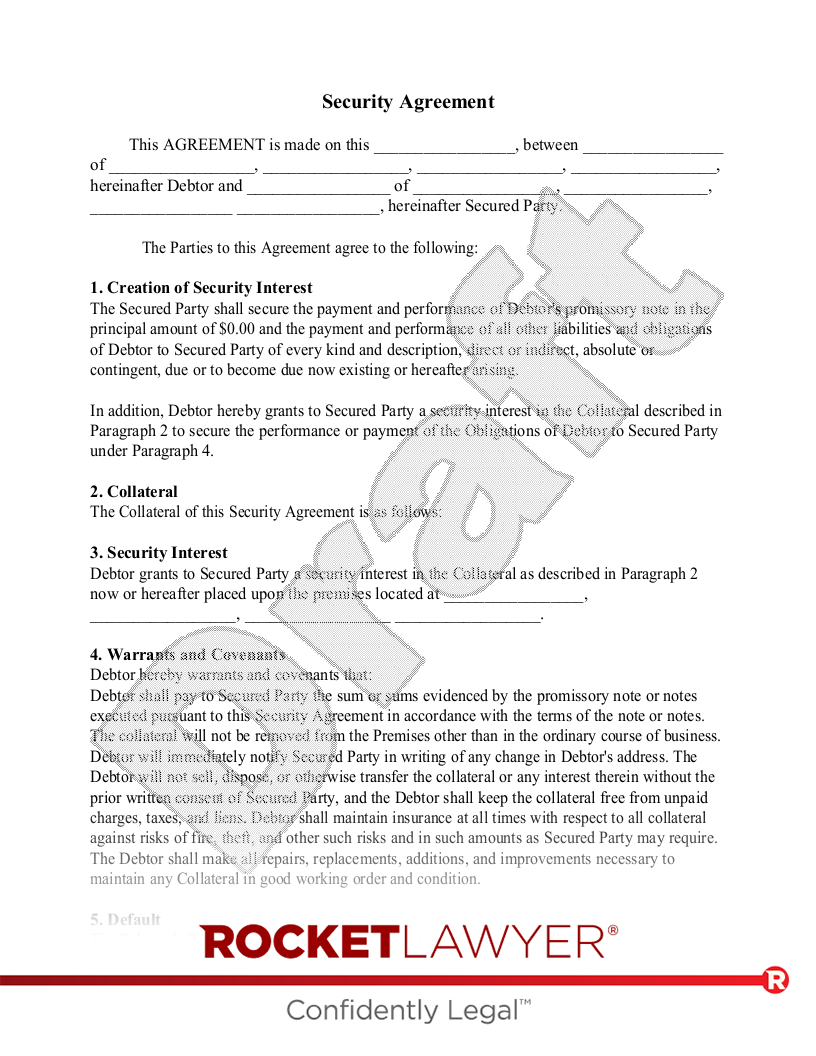

Parties Involved and the Granting Clause

The agreement must clearly identify the “Debtor” (the borrower) and the “Secured Party” (the lender). Following this identification is the “Granting Clause,” which is perhaps the most vital sentence in the document. It typically reads: “The Debtor hereby grants to the Secured Party a security interest in the following property…” Without this explicit language, a security interest may not legally attach to the assets, rendering the lender’s claim toothless.

Description of Collateral

Specificity is paramount when describing the collateral. In some cases, a lender may take a “blanket lien,” which covers all of the debtor’s assets, both current and future-acquired. In other cases, the agreement might specify particular items, such as a CNC machine identified by its serial number or a specific fleet of delivery vehicles. If the description is too vague, the lender risks losing their priority status during bankruptcy or liquidation proceedings.

Obligations and Covenants

The security agreement isn’t just about what happens during a default; it also outlines how the borrower must manage the collateral while the loan is active. These “covenants” often include:

- Maintenance: The borrower must keep the collateral in good working order.

- Insurance: The borrower must maintain insurance on the collateral, naming the lender as the loss payee.

- Taxes: The borrower must pay all taxes related to the collateral to prevent government liens from taking priority.

- Inspection Rights: The lender usually retains the right to inspect the collateral at reasonable times.

Default and Remedies

This section defines what constitutes a “breach” of the agreement. While the most common default is a failure to make timely payments, other triggers might include the borrower filing for bankruptcy, the collateral being seized by another creditor, or the borrower providing false information on their financial statements. The “Remedies” portion outlines what the lender can do once a default occurs, such as accelerating the debt (making the full balance due immediately) or repossessing the collateral.

3. Types of Collateral Covered in Business Finance

In the “Money” niche, collateral is categorized based on its liquidity and nature. The type of collateral involved often dictates the complexity of the security agreement.

Tangible Assets: Equipment and Inventory

For manufacturing or retail businesses, tangible assets are the most common forms of collateral.

- Equipment: Includes machinery, computers, and vehicles. These are generally easier to value but may depreciate over time.

- Inventory: This includes raw materials and finished goods intended for sale. Security agreements involving inventory often include “after-acquired property” clauses, ensuring that as inventory is sold and replaced, the lender’s interest automatically attaches to the new stock.

Intangible Assets: Accounts Receivable and Intellectual Property

Modern business finance increasingly relies on intangible assets.

- Accounts Receivable: Also known as “factoring” or “receivables financing,” a business can pledge the money owed to it by customers. This provides immediate cash flow based on future expected income.

- Intellectual Property (IP): Patents, trademarks, and copyrights can be incredibly valuable. However, perfecting a security interest in IP often requires filings with the U.S. Patent and Trademark Office (USPTO) in addition to standard UCC filings.

Floating Liens vs. Fixed Liens

A Fixed Lien attaches to a specific, identifiable asset that doesn’t change, like a piece of real estate or a specific tractor. A Floating Lien, however, is more dynamic. It “floats” over a category of assets that change daily, such as inventory or accounts receivable. The floating lien becomes “fixed” only when a default occurs, allowing the lender to claim whatever assets are in that category at that specific moment.

4. The Importance of Attachment and Perfection

For a lender to truly be protected, two legal milestones must be met: attachment and perfection. These concepts are fundamental to understanding how security agreements function in a competitive financial environment where multiple creditors might be vying for the same assets.

What is “Attachment”?

Attachment is the process by which a security interest becomes enforceable against the debtor. For attachment to occur, three conditions must generally be met:

- The lender must give value (usually by providing the loan).

- The debtor must have rights in the collateral (they must own it or have the right to pledge it).

- The debtor must sign a security agreement that provides a description of the collateral.

Once these three pillars are in place, the security interest has “attached,” and the lender has a legal claim against the borrower.

Perfection: Protecting the Lender’s Priority

While attachment makes the agreement valid between the lender and the borrower, Perfection makes the agreement valid against third parties. If a business takes out two loans from two different banks using the same equipment as collateral, the bank that “perfected” its interest first usually has the first right to the asset. Perfection is typically achieved by filing a UCC-1 financing statement, though for certain assets like cash or stocks, it can be achieved through “control” or “possession.”

The Impact on Small Business Loans

For small business owners, the perfection of a security agreement is what shows up on a credit report or a public records search. Investors and other lenders will look for these filings to determine how much of the company’s assets are already “spoken for.” High levels of encumbered assets can make it more difficult to secure additional rounds of funding, making it vital for business owners to manage their security agreements strategically.

5. Best Practices for Navigating Security Agreements

Navigating the world of secured debt requires a proactive approach. Whether you are a lender looking to protect your capital or a borrower looking to fuel growth, following best practices can prevent future financial distress.

Due Diligence for Borrowers

Before signing a security agreement, borrowers must conduct thorough due diligence. This includes verifying that they have the clear title to the assets they are pledging and ensuring that the valuation of those assets is accurate. Borrowers should also be wary of “cross-collateralization” clauses, which allow a lender to use collateral from one loan to secure another, potentially putting more assets at risk than initially intended.

Negotiating Terms and Conditions

Everything in a security agreement is negotiable. Borrowers should strive to limit the scope of the collateral to only what is necessary to secure the loan. For example, instead of a blanket lien on all assets, a borrower might negotiate to pledge only specific pieces of equipment. Additionally, negotiating the “cure period”—the amount of time a borrower has to fix a default before the lender repossesses the collateral—can provide a crucial lifeline during a temporary cash flow crunch.

Managing the Lifecycle of the Agreement

A security agreement is not a “set it and forget it” document. As a business grows, its asset base changes. It is essential to periodically review existing agreements. If a loan is paid off, the borrower must ensure that the lender files a UCC-3 Termination Statement to “release” the lien. Failure to do this can leave a “cloud” on the business’s title, making it difficult to sell the company or secure new financing in the future.

Conclusion

The security agreement is the unsung hero of the financial world, providing the legal structure that allows businesses to leverage their assets for growth. By clearly defining what happens in the event of a default, these agreements reduce uncertainty, lower the cost of borrowing, and provide lenders with the confidence to inject capital into the economy.

For anyone involved in the movement of money—from the institutional investor to the local shop owner—mastering the nuances of the security agreement is essential. It is more than just a contract; it is a vital financial tool that, when used correctly, facilitates the sustainable expansion of commerce and the efficient management of financial risk.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.