In an increasingly digital financial landscape, understanding the fundamental mechanics of how money moves is paramount. While many aspects of our daily finances, from swiping a debit card to making an online purchase, seem effortless, a complex network of identifiers and systems works behind the scenes to ensure transactions are accurate and secure. Among these crucial identifiers is the routing number. Often discussed in the context of bank accounts and checks, its relationship with a debit card can sometimes be a source of confusion.

A routing number is a cornerstone of the U.S. financial system, acting as a unique nine-digit code that identifies your financial institution, much like a postal code identifies a specific geographic location. While your debit card is your primary tool for accessing funds directly from your bank account for purchases and ATM withdrawals, the routing number itself isn’t typically printed on the card. Instead, it’s intrinsically linked to the underlying bank account that your debit card draws from. Grasping this distinction and understanding where to find and how to use your routing number is not just good practice, but a vital component of managing your personal finances effectively, enabling everything from direct deposits to automated bill payments. This article will demystify the routing number, clarify its connection to your debit card and bank account, and underscore its indispensable role in the modern financial ecosystem.

Unpacking the Essentials: What Exactly is a Routing Number?

At its core, a routing number is more than just a sequence of digits; it’s a critical navigational tool within the vast and intricate U.S. banking system. Understanding its precise definition and purpose is the first step towards demystifying its function in your financial life.

The Core Definition: A Unique Bank Identifier

A routing number, officially known as an ABA (American Bankers Association) routing transit number, is a nine-digit code used to identify a specific financial institution in the United States. Established in 1910, its primary purpose was to facilitate the sorting and routing of paper checks, ensuring they reached the correct bank for payment. While its origins lie in a more analog era, its utility has profoundly evolved, becoming central to the digital transfer of funds. Each of the nine digits carries specific information, allowing the Automated Clearing House (ACH) network and wire transfer systems to accurately direct funds to the intended bank. This unique identifier ensures that when you send or receive money electronically, the transaction goes to the right financial institution, even among the thousands operating nationwide.

Why Banks Need It: The Backbone of Electronic Transactions

The necessity of routing numbers stems from the fundamental requirement to accurately identify the origin and destination of financial transactions. Without a standardized system, electronic transfers would be prone to errors, delays, and security vulnerabilities. Banks rely on routing numbers for several key functions:

- Facilitating ACH Transfers: This includes direct deposits (like paychecks, tax refunds, or government benefits), automatic bill payments, and person-to-person (P2P) payments that link directly to bank accounts. The routing number ensures that the funds are debited from or credited to the correct bank.

- Processing Wire Transfers: For larger, often time-sensitive transfers between financial institutions, both domestic and international, the routing number (along with SWIFT/BIC codes for international transfers) is indispensable for swift and secure delivery.

- Clearing Checks: Despite the rise of digital payments, checks are still used. When a check is deposited, the routing number directs it to the correct issuing bank for verification and fund transfer.

In essence, the routing number acts as a crucial address for your bank, enabling seamless and secure financial operations across the entire network.

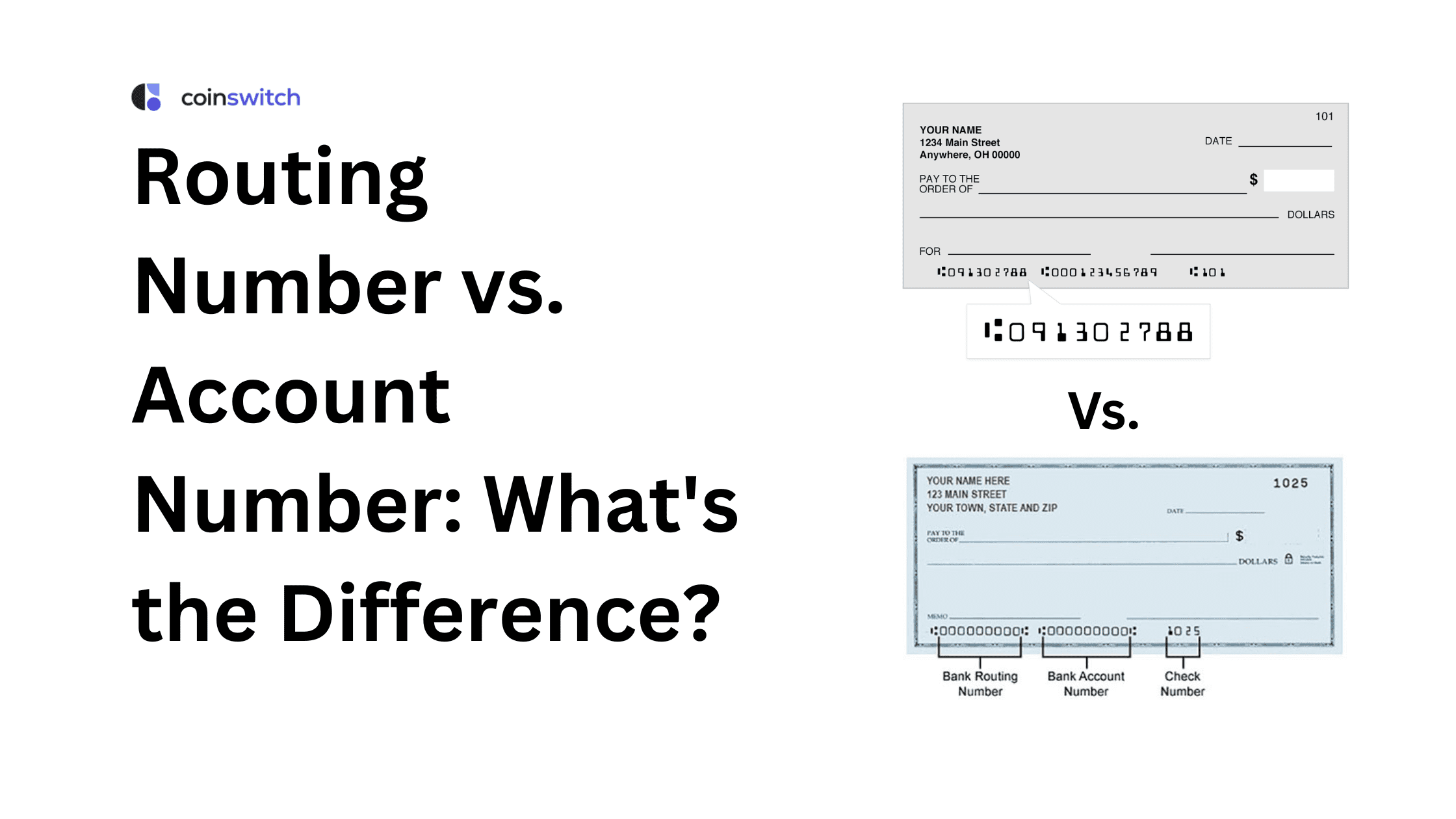

Distinction from Account Number: Two Sides of the Same Coin

It’s common for individuals to confuse a routing number with an account number, but they serve distinct and equally important roles. While both are necessary for many financial transactions, they identify different components:

- Routing Number (Bank Identifier): This nine-digit code identifies the specific financial institution (bank, credit union) where the account is held. Think of it as the bank’s unique “street address.” A single bank might have multiple routing numbers, especially if it operates in different regions or for different types of transactions (e.g., one for ACH, another for wire transfers, though often they are the same).

- Account Number (Specific Account Identifier): This is a unique sequence of digits (typically 10-12 digits, but varying by bank) that identifies your specific checking or savings account within that financial institution. This is your personal “house number” at that bank’s address.

To complete most electronic transactions, both the routing number (to find the bank) and the account number (to find your specific account within that bank) are required. Understanding this distinction is vital for accurately providing your banking details and avoiding potential financial missteps.

Your Debit Card and the Routing Number: A Closer Look

The debit card is arguably one of the most frequently used financial tools in modern life. It grants immediate access to funds in your checking account for purchases, online transactions, and ATM withdrawals. Given its direct link to your bank account, it’s natural to wonder if the routing number resides directly on the card itself.

Is the Routing Number Directly On Your Debit Card?

This is a common point of confusion, and the straightforward answer is: No, the routing number is typically not printed directly on your physical debit card. While your debit card is undeniably connected to a bank account that has a routing number, the card itself serves a different primary function.

Debit cards are designed for point-of-sale (POS) transactions, ATM withdrawals, and online purchases where you generally provide the card number, expiration date, and CVV (Card Verification Value). These details are sufficient for transactions that involve debiting your specific account through the card networks (Visa, Mastercard, etc.). The routing number, on the other hand, is primarily used for direct bank-to-bank transfers, which do not typically involve swiping or inserting a debit card. Printing it on the card would also present a security risk, as it’s a piece of information that, combined with an account number, could be used for unauthorized access to your funds.

Where to Find Your Routing Number (If Not on the Card)

Since your debit card won’t display it, knowing where to locate your routing number is essential for various financial activities. Here are the most reliable sources:

- Bank Checks: For checking accounts, the routing number is prominently displayed at the bottom of a physical check, typically the first set of nine digits on the left.

- Online Banking Portal/Mobile App: This is often the quickest and most convenient method. After logging into your bank’s online platform or mobile app, navigate to your account details. The routing number for your specific account is usually listed alongside your account number.

- Bank Statements: Your monthly bank statements, whether paper or electronic, will almost always include your routing number, usually near your account number or at the top of the statement.

- Bank’s Official Website: Many banks provide a dedicated section on their website (often in the FAQ or “Contact Us” sections) where you can look up routing numbers by state or account type.

- Contact Customer Service: If you can’t find it through any of the above methods, a quick call to your bank’s customer service department will provide you with the correct routing number after verifying your identity.

It’s important to note that some banks may have different routing numbers for different purposes (e.g., one for ACH transfers, another for wire transfers). Always double-check that you are using the correct routing number for the specific type of transaction you are performing.

Why the Debit Card Itself Doesn’t Display It: Security and Functionality

The decision not to print routing numbers on debit cards is rooted in both security protocols and the distinct functionality of the card itself.

From a security perspective, the debit card is already susceptible to theft or compromise. If a routing number were also printed on it, alongside the card number and your name (which often helps deduce your account number), it would simplify the process for fraudsters to initiate unauthorized ACH transfers or other bank-to-bank transactions. By keeping the routing number separate, banks add another layer of protection. If your card is lost or stolen, criminals can use it for card-based transactions, but they generally cannot initiate direct bank transfers without additional information.

From a functionality standpoint, the debit card is designed for instantaneous point-of-sale transactions and ATM access, which operate on specific card networks (Visa, Mastercard, etc.). These networks use unique card numbers and associated security features to process payments. Routing numbers, conversely, are integral to the ACH network and wire transfer systems, which are distinct from card processing networks. The information needed for a card transaction is different from the information needed for a bank-to-bank transfer, making it unnecessary and potentially confusing to include routing numbers on cards.

The Critical Role of Routing Numbers in Modern Finance

While your debit card offers immediate access to your funds, it’s the routing number that truly underpins the broader infrastructure enabling the seamless movement of money within the financial system. Its significance extends far beyond simply identifying your bank.

Facilitating Electronic Transfers: The Engine of Digital Payments

The routing number is the engine that drives virtually all major forms of electronic money transfers in the U.S. Without it, the convenience and speed we’ve come to expect from digital banking would be impossible.

- Direct Deposits: Whether it’s your monthly paycheck, a government benefit like Social Security, or a tax refund, direct deposits rely entirely on routing numbers. Your employer or the issuing agency uses your bank’s routing number and your account number to ensure your funds land directly into your designated account without the need for paper checks.

- Automatic Bill Payments: Many consumers set up recurring bill payments for utilities, loans, or subscriptions directly from their bank accounts. These automated clearing house (ACH) debits use your routing and account numbers to pull funds from your bank at scheduled intervals, offering convenience and reducing the risk of missed payments.

- Domestic Wire Transfers: For transferring large sums of money quickly and securely between banks within the United States, a routing number is essential. Wire transfers are often irreversible and are used for critical transactions like closing on a house or making a significant investment.

- Person-to-Person (P2P) Payments: While many P2P apps like Venmo or Zelle operate with phone numbers or email addresses, they ultimately link back to a bank account. For initial setup or for larger transfers, your routing and account numbers may be required to connect your bank account to these services, enabling the underlying ACH transfers.

In essence, any transaction that involves moving money directly between bank accounts, rather than through a card network, is facilitated by the routing number.

Preventing Errors and Ensuring Security: A Layer of Accuracy

Beyond mere facilitation, routing numbers play a critical role in maintaining the accuracy and security of the financial system. Each routing number is rigorously assigned and verified by the American Bankers Association, ensuring its uniqueness and validity.

- Accuracy in Routing: Imagine trying to mail a letter without a zip code; it might eventually get there, but with significant delays and potential misdirection. The routing number acts as this essential “zip code” for financial transactions, guiding funds precisely to the correct financial institution. This dramatically reduces the potential for funds being sent to the wrong bank, which could lead to significant financial headaches and recovery efforts.

- Fraud Prevention: While a routing number alone isn’t enough to compromise an account, its structured use helps prevent certain types of fraud. By requiring both a valid routing number and a valid account number, the system adds a layer of verification. Banks also monitor unusual activity associated with routing numbers, flagging potential fraudulent attempts to open accounts or initiate transfers from unknown or suspicious sources. The regulated nature of routing number assignment also means that only legitimate financial institutions possess these identifiers.

What Happens if You Use the Wrong Routing Number?

Mistakes happen, but using an incorrect routing number can have notable consequences:

- Rejected Transactions: Most commonly, if the routing number doesn’t match a valid bank or doesn’t correspond to the provided account number, the transaction will simply be rejected. This is the best-case scenario, as your money isn’t lost, but the payment or deposit will be delayed. You’ll then need to correct the information and re-initiate the transfer.

- Delayed Payments: Even if the routing number is valid but incorrect for your specific account, the transaction might be delayed as the banks try to reconcile the discrepancy. This can lead to late fees if it’s a bill payment, or delays in receiving crucial funds.

- Funds Sent to the Wrong Account (Rare but Serious): In rare instances, if the incorrect routing number happens to correspond to a real bank and the account number also happens to match a real account at that bank (even if it’s not yours), your funds could be mistakenly deposited into someone else’s account. Recouping these funds can be a complex and lengthy process, often requiring the cooperation of the recipient and the involved banks, and there’s no guarantee of full recovery, especially if the funds are quickly withdrawn.

Therefore, always double-checking your routing number before initiating any critical transaction is a small but crucial step in safeguarding your financial well-being.

Safeguarding Your Financial Information

Understanding what a routing number is and where to find it is only half the battle. Equally important is knowing when and how to share this sensitive information and recognizing potential red flags to protect yourself from financial fraud.

When and How to Share Your Routing Number

Because a routing number, especially when combined with your account number, provides direct access to your bank account for electronic transfers, it’s information that should be treated with care.

When to Share:

- Employer for Direct Deposit: This is one of the most common and legitimate reasons to share your routing and account numbers. It ensures your paycheck is deposited directly into your bank account.

- Legitimate Billers for Automatic Payments: When setting up recurring payments for utilities, rent, mortgage, or loans directly from your bank account, you’ll need to provide these details. Always ensure the biller is reputable and that you are on their official website or using their verified payment portal.

- Government Agencies: For tax refunds, social security benefits, or other government disbursements, you’ll need to provide your routing and account numbers to receive funds electronically.

- Setting up Investment Accounts or Other Financial Services: When linking your bank account to a brokerage, retirement, or other financial services account for transfers, you will be asked for these details.

- Friends/Family for Bank-to-Bank Transfers: If someone needs to transfer money directly into your account, you’ll need to provide them with your routing and account numbers. Be sure you trust the individual.

How to Share:

- Secure Platforms: Whenever possible, use secure, encrypted online portals provided by your bank, employer, or biller. Avoid sending this information via unencrypted email or text messages.

- In Person with Trusted Entities: If you’re providing a voided check or written details, ensure you are doing so with a legitimate representative of a trusted organization.

- Verify Recipient: Always verify the identity of the person or organization requesting your banking details. Call them back on a known, official number if you’re unsure.

Red Flags and Security Best Practices

Vigilance is your best defense against financial fraud. Be aware of these warning signs and adopt sound security habits:

- Unsolicited Requests: Be extremely wary of anyone who unexpectedly asks for your routing and account numbers, especially via email, text, or phone calls claiming to be from your bank or a government agency. Legitimate institutions rarely ask for this sensitive information unsolicited.

- Threats or Urgency: Scammers often try to create a sense of urgency or fear (“Your account will be closed if you don’t provide this immediately!”). This is a classic tactic to pressure you into revealing information without thinking.

- Phishing Attempts: Look out for suspicious emails or links that mimic your bank’s website but have slight variations in the URL. Always manually type your bank’s website address or use their official mobile app.

- Public Wi-Fi: Avoid accessing your online banking or entering sensitive information when connected to unsecured public Wi-Fi networks, as they can be vulnerable to eavesdropping.

- Monitor Bank Statements: Regularly review your bank statements and transaction history for any unauthorized activity. The sooner you detect an issue, the faster your bank can help resolve it.

- Strong Passwords and Multi-Factor Authentication (MFA): Use strong, unique passwords for your online banking accounts and enable MFA whenever available. This adds a crucial layer of security, requiring a second verification step (like a code sent to your phone) to log in.

The Interplay with Other Financial Identifiers

While routing numbers are specific to the U.S. domestic banking system, it’s worth briefly noting their relationship with international equivalents. For international wire transfers, you’ll typically need a SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or BIC code (Bank Identifier Code) in addition to the recipient’s bank account number. SWIFT codes serve a similar purpose to routing numbers but on a global scale, identifying specific banks for cross-border transactions. Understanding this distinction is key if you ever need to send or receive money internationally, as a U.S. routing number alone won’t suffice.

Conclusion: Empowering Your Financial Journey

The journey through the intricacies of the routing number reveals its unassuming yet profoundly powerful role in modern personal finance. While your debit card acts as your direct portal to your funds, it is the routing number that serves as the crucial navigator, directing the flow of money through the vast banking network with precision and security. It’s the silent workhorse behind the convenience of direct deposits, automatic bill payments, and countless other electronic transfers that define our financial interactions today.

We’ve established that while your debit card is your most frequent tool for daily spending, the routing number itself does not reside on the card. Instead, it’s an identifier for the bank account your card draws from, accessible through checks, online banking portals, and bank statements. This deliberate separation is a key aspect of financial security, ensuring that different pieces of information are needed for different types of transactions.

Understanding the routing number is more than just knowing a nine-digit code; it’s about grasping a fundamental element of financial literacy. It empowers you to confidently manage your money, set up essential financial services, and most importantly, protect your assets by knowing when and how to share this vital information securely. In an era where digital transactions are the norm, this knowledge equips you to navigate your financial landscape with greater insight, control, and peace of mind. By paying attention to these details, you not only safeguard your own finances but also contribute to the integrity of the broader financial system.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.