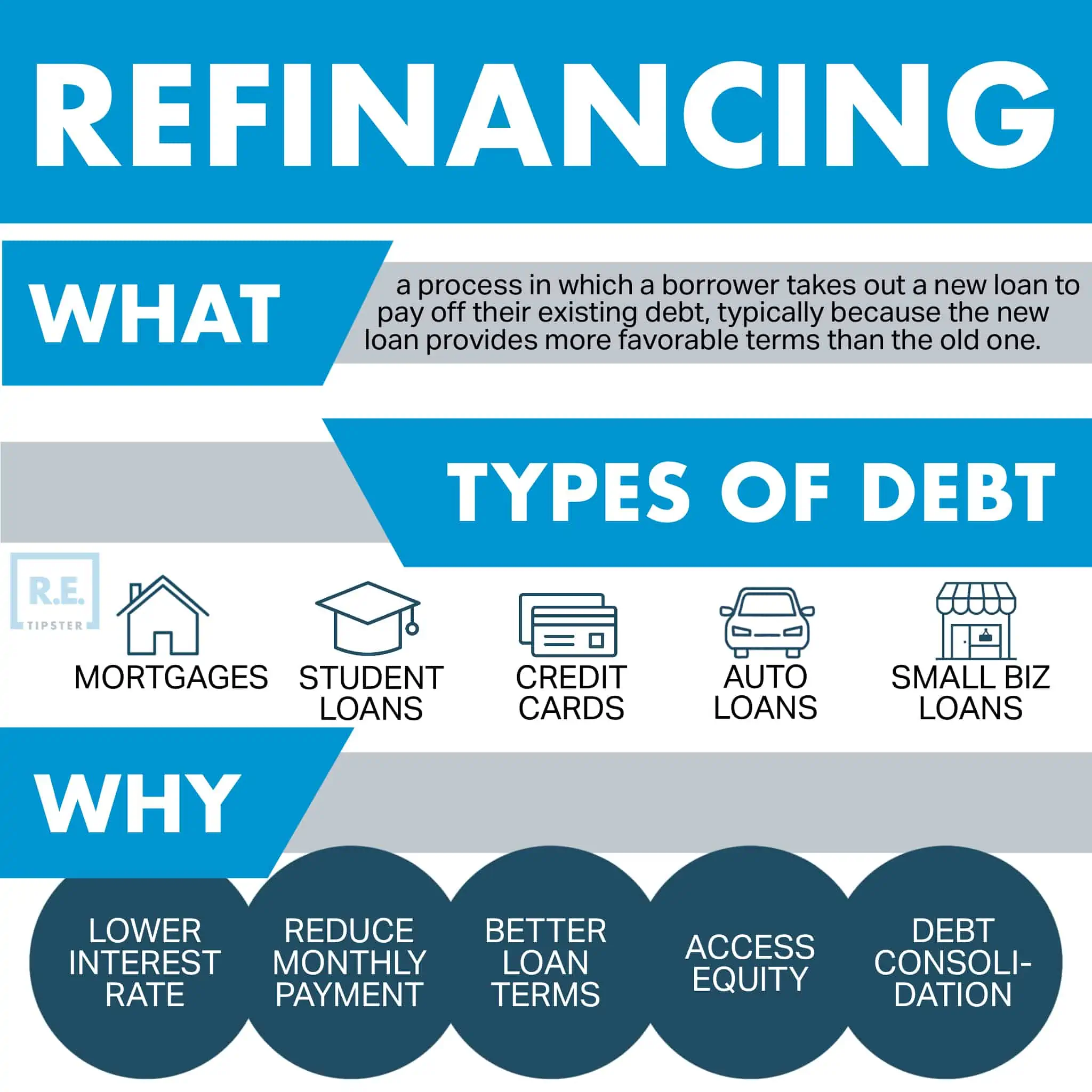

A refinance loan is a financial transaction where a borrower replaces an existing loan with a new one, typically from the same or a different lender. This new loan pays off the original debt, and the borrower then makes payments on the new terms. While the concept applies to various types of debt—from personal loans and student loans to auto loans—it is most commonly associated with mortgages due to the significant financial implications and the large sums involved. Understanding what a refinance entails is crucial for anyone looking to optimize their financial situation, reduce their debt burden, or unlock their existing assets.

Understanding the Core Concept of Refinancing

At its heart, refinancing is a strategic financial move designed to improve a borrower’s existing loan terms. It’s not about taking on new debt in addition to what you already owe; rather, it’s about replacing an old debt with a more favorable new one.

The Basic Definition

Simply put, refinancing involves securing a new loan to pay off an existing one. The new loan comes with its own set of terms, including a new interest rate, a new repayment schedule, and potentially new fees. Once the new loan is approved and disbursed, the funds are used to clear the outstanding balance of the original loan. From that point forward, all repayments are directed towards the new loan. This process can be compared to exchanging an old contract for a new one, hoping the new terms are more beneficial.

Common Types of Loans Refinanced

While the principles of refinancing are universal, the application varies depending on the type of loan:

- Mortgages: This is by far the most common type of refinancing. Homeowners often refinance their mortgages to secure lower interest rates, change their loan term, or convert home equity into cash.

- Auto Loans: Car owners might refinance their auto loans to reduce monthly payments, lower interest rates, or change the loan term, especially if their credit score has improved since the original purchase.

- Student Loans: Both federal and private student loans can be refinanced. This is often done to consolidate multiple loans into a single payment, achieve a lower interest rate, or alter the repayment schedule.

- Personal Loans: Individuals with existing personal loans might refinance them to get a better interest rate, especially if their financial standing has improved, or to extend the repayment period to reduce monthly costs.

Key Players in a Refinance Transaction

A typical refinance transaction involves several parties:

- The Borrower: This is the individual or entity seeking to replace their existing loan. Their financial health, creditworthiness, and goals drive the entire process.

- The New Lender: This is the financial institution (bank, credit union, online lender) providing the new loan. They assess the borrower’s eligibility and offer new terms.

- The Original Lender (sometimes): While the original lender is paid off, in some cases, a borrower might refinance with their current lender. However, it’s common to shop around for the best terms from various institutions.

- Third-Party Services (especially for mortgages): These can include appraisers, title companies, escrow agents, and attorneys who facilitate various aspects of the transaction, ensuring legal compliance and property valuation.

Why People Refinance: Primary Motivations

The decision to refinance is usually driven by a specific financial goal. Understanding these motivations can help borrowers determine if refinancing aligns with their objectives.

Lowering Your Interest Rate

One of the most compelling reasons to refinance is to secure a lower interest rate. This can happen due to:

- Market Changes: Interest rates fluctuate, and a borrower might be able to lock in a significantly lower rate than when they originally took out their loan.

- Improved Credit Score: If a borrower’s credit score has improved substantially since the original loan, they may now qualify for more favorable terms and a lower rate, signaling reduced risk to lenders. A lower interest rate translates directly to reduced costs over the life of the loan and lower monthly payments.

Reducing Monthly Payments

By extending the loan term or securing a lower interest rate, refinancing can significantly reduce the borrower’s monthly financial obligation. While extending the term might mean paying more interest over the loan’s lifetime, it can provide crucial breathing room in a tight monthly budget. This is a common strategy for those looking to improve their cash flow.

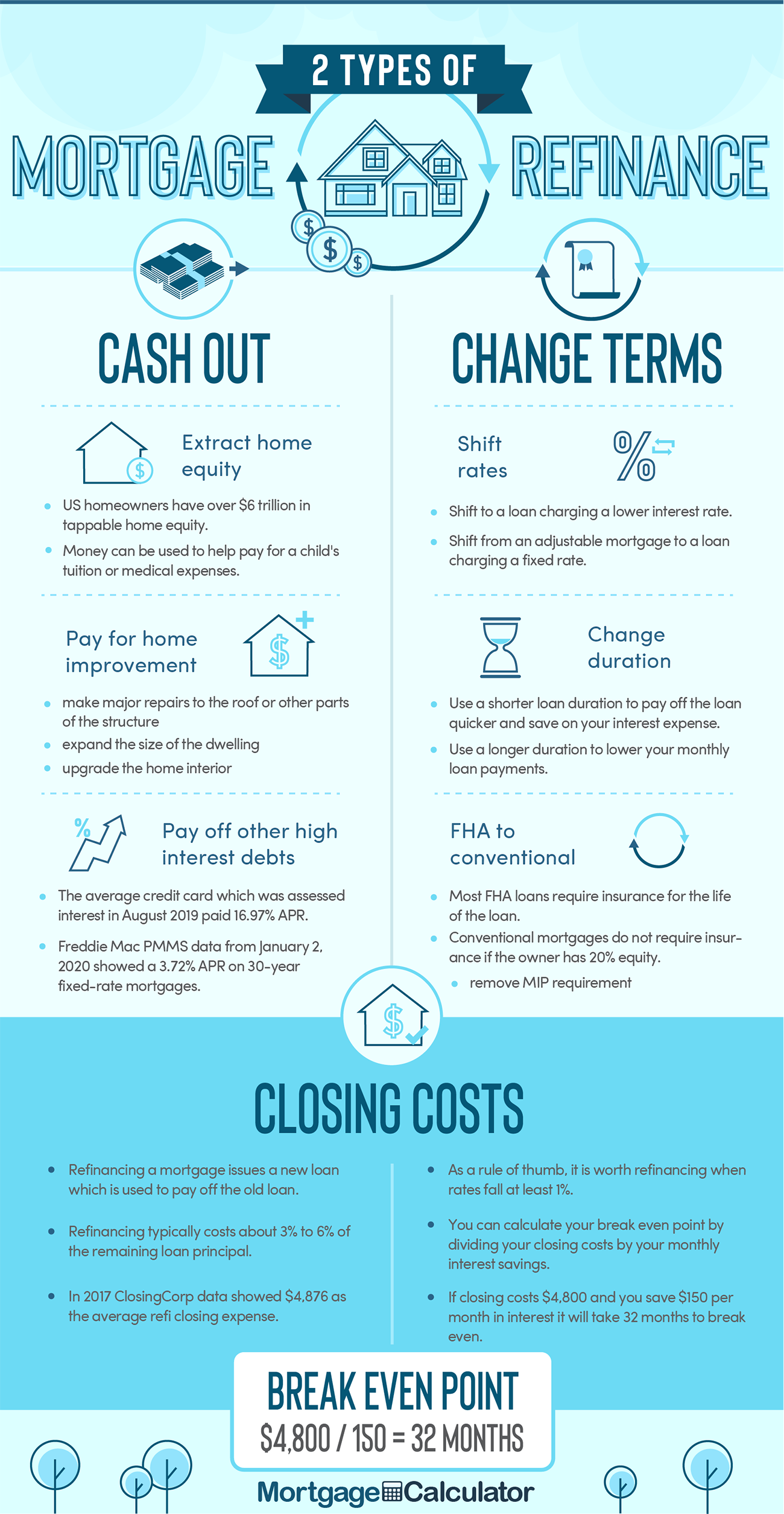

Accessing Home Equity (Cash-Out Refinance)

For homeowners, a cash-out refinance allows them to tap into their home’s equity. With this type of refinance, the new loan is for a higher amount than the outstanding balance of the original mortgage. The difference is given to the homeowner in cash, which can then be used for various purposes such as home improvements, consolidating high-interest debt, funding education, or making other investments. This strategy can be more advantageous than a personal loan or credit card for large expenses, as mortgage rates are typically lower.

Changing Loan Terms

Borrowers might refinance to alter the structure of their loan:

- Fixed-Rate to Adjustable-Rate (or vice versa): Someone with a fixed-rate mortgage might switch to an adjustable-rate mortgage (ARM) if they anticipate selling their home before the ARM adjusts, potentially enjoying a lower initial rate. Conversely, someone with an ARM might switch to a fixed-rate to gain predictability and stability in their monthly payments.

- Shorter or Longer Amortization: A borrower might refinance from a 30-year mortgage to a 15-year mortgage to pay off their home faster and save on total interest, provided they can afford the higher monthly payments. Or, they might extend a 15-year loan to a 30-year one to reduce monthly payments.

Consolidating Debt

A refinance loan, especially a cash-out mortgage refinance, can be a powerful tool for debt consolidation. By using the cash-out portion to pay off high-interest debts like credit card balances or personal loans, borrowers can consolidate multiple payments into a single, often lower-interest, monthly mortgage payment. This simplifies financial management and can lead to significant savings on interest over time.

Removing or Adding a Borrower

Life changes, such as divorce, marriage, or the need to release a co-signer, can necessitate a refinance. This allows for the removal of one party from the loan obligation or the addition of a new co-borrower, updating the legal and financial responsibility for the debt.

The Refinance Process: A Step-by-Step Guide

While specific steps can vary by loan type and lender, the general refinance process follows a predictable path.

Assess Your Financial Situation and Goals

Before embarking on a refinance, borrowers should thoroughly evaluate their current financial standing, including credit score, debt-to-income ratio, and available equity (for mortgages). Critically, define your primary goal: Is it to lower your rate, reduce payments, get cash out, or consolidate debt? Having a clear objective will guide your choices.

Research and Compare Lenders

Do not settle for the first offer. Shop around and compare interest rates, fees, closing costs, and terms from multiple lenders (banks, credit unions, online lenders, mortgage brokers). A seemingly small difference in interest rate can translate to thousands of dollars in savings over the life of a loan. Look for transparency in fees and positive customer service reviews.

Gather Necessary Documentation

Lenders will require extensive documentation to verify your income, assets, and existing debts. This typically includes recent pay stubs, W-2 forms, tax returns, bank statements, investment account statements, existing loan statements, and possibly property deeds and insurance policies (for mortgages). Having these documents organized and readily available can expedite the application process.

Apply for the Loan

Once you’ve selected a preferred lender, you’ll complete a formal loan application. This involves providing personal and financial information, consenting to a credit check, and specifying the type of refinance you’re seeking. Be prepared for a “hard inquiry” on your credit report, which will temporarily lower your score.

Underwriting and Appraisal

Following the application, the lender’s underwriting department will review all submitted documents to assess your creditworthiness and ability to repay the new loan. For mortgage refinances, an appraisal of the property will be ordered to determine its current market value, ensuring there is sufficient collateral for the loan. The underwriting process can take several weeks as the lender verifies all information.

Loan Approval and Closing

If your application passes underwriting, you will receive a loan approval with a commitment letter outlining the final terms. During the closing phase, you will review and sign numerous legal documents. For mortgages, this includes the new promissory note and deed of trust. Once all documents are signed and closing costs are paid, the new loan funds are disbursed to pay off your old loan, and the refinance is complete.

Potential Costs and Considerations of Refinancing

While the benefits can be substantial, refinancing is not without costs and important considerations.

Closing Costs

Refinancing, particularly a mortgage refinance, incurs closing costs, which are fees paid to the lender and third parties for processing the new loan. These can include:

- Application Fees: For processing your loan application.

- Appraisal Fees: For valuing the property.

- Title Insurance and Search: To ensure clear title to the property.

- Origination Fees (Points): Fees paid to the lender for originating the loan, often expressed as a percentage of the loan amount.

- Recording Fees: To legally record the new mortgage.

- Escrow Fees: For managing the closing process.

These costs typically range from 2% to 5% of the loan amount and can often be rolled into the new loan balance, though this means paying interest on them.

Break-Even Point Analysis

It’s crucial to calculate the “break-even point” when refinancing. This is the amount of time it will take for your savings from the lower interest rate or reduced payments to offset the costs of refinancing. If you plan to sell your home or pay off the loan before reaching the break-even point, the refinance might not be financially advantageous.

Impact on Credit Score

Applying for a refinance involves a hard inquiry on your credit report, which can temporarily ding your score. Additionally, closing your old loan and opening a new one can affect your credit history and overall credit mix. While these impacts are usually minor and temporary for responsible borrowers, it’s something to be aware of.

Prepayment Penalties

Some existing loans, particularly older or certain types of personal loans, may carry prepayment penalties. These are fees charged by the original lender if you pay off your loan earlier than scheduled. Always check your current loan agreement for any such clauses before refinancing, as these penalties can erode your savings.

The Dangers of “Rate Chasing”

Constantly refinancing every time interest rates drop slightly can lead to accumulated closing costs that outweigh any potential savings. Each refinance incurs fees, so it’s essential to ensure the benefits truly justify the expenses and effort involved. Refinancing should be a strategic move, not a frequent reaction to minor market shifts.

Is Refinancing Right For You? Making an Informed Decision

Deciding whether to refinance requires careful consideration of your personal financial situation, market conditions, and long-term goals.

When Refinancing Makes Sense

- Significant Interest Rate Drop: If current rates are substantially lower than your existing loan’s rate, the long-term savings can be considerable, justifying the closing costs.

- Improved Credit Score: If your credit profile has strengthened significantly, you’re likely to qualify for better terms than you initially received.

- Need for Cash: A cash-out refinance can be an excellent way to fund major expenses or consolidate high-interest debt, provided you use the funds wisely and can manage the new mortgage payments.

- Desire for Different Loan Terms: Whether you want to pay off your loan faster with a shorter term or reduce monthly payments with a longer term, refinancing can provide the flexibility to align with your financial strategy.

- Debt Consolidation: If you have multiple high-interest debts, consolidating them into a lower-interest refinance loan can simplify payments and save money.

When to Reconsider Refinancing

- High Closing Costs Relative to Savings: If the fees associated with refinancing are high and your potential savings are minimal, it might not be worth the effort.

- Short Time Horizon: If you plan to move, sell the asset, or pay off the loan in the near future, you might not reach the break-even point to recoup your closing costs.

- Worsening Financial Situation: If your credit score has declined, or your income or job stability is uncertain, refinancing might not be possible, or you might not qualify for better terms.

- Prepayment Penalties: If your current loan has a hefty prepayment penalty, the cost of breaking the old loan might outweigh the benefits of the new one.

Seeking Professional Financial Advice

For complex situations or if you are unsure whether refinancing aligns with your broader financial plan, consulting with a qualified financial advisor is highly recommended. They can help you analyze your specific circumstances, weigh the pros and cons, and determine the optimal strategy for your financial health. A refinance loan can be a powerful financial tool, but like any financial decision, it requires thorough research and a clear understanding of its implications.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.