A put spread is a sophisticated options trading strategy that involves simultaneously buying and selling put options on the same underlying asset, with the same expiration date, but at different strike prices. This strategy is typically employed by traders who have a moderately bearish outlook on the underlying asset, meaning they expect its price to decline, but they also wish to limit their potential losses and cap their potential gains. Understanding put spreads is crucial for investors seeking to navigate the complexities of options trading with a defined risk and reward profile.

The fundamental concept behind a put spread is to create a directional bet on a price movement while simultaneously controlling the cost and the potential downside. Unlike simply buying a put option, which offers unlimited profit potential as the underlying price falls but also carries the risk of losing the entire premium paid, a put spread involves a more hedged approach. This hedging is achieved by selling another put option at a lower strike price.

Types of Put Spreads and Their Mechanics

There are two primary types of put spreads: the bear put spread and the out-of-the-money (OTM) put spread. While both involve buying and selling put options, their construction and the market outlook they represent differ.

Bear Put Spread: A Moderately Bearish Strategy

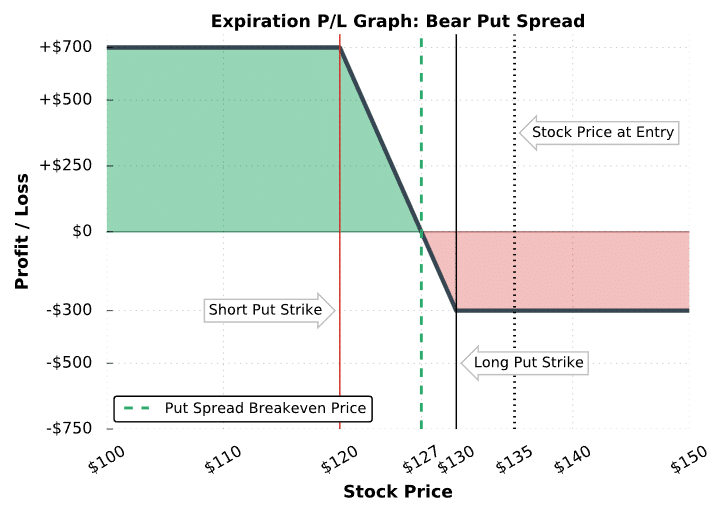

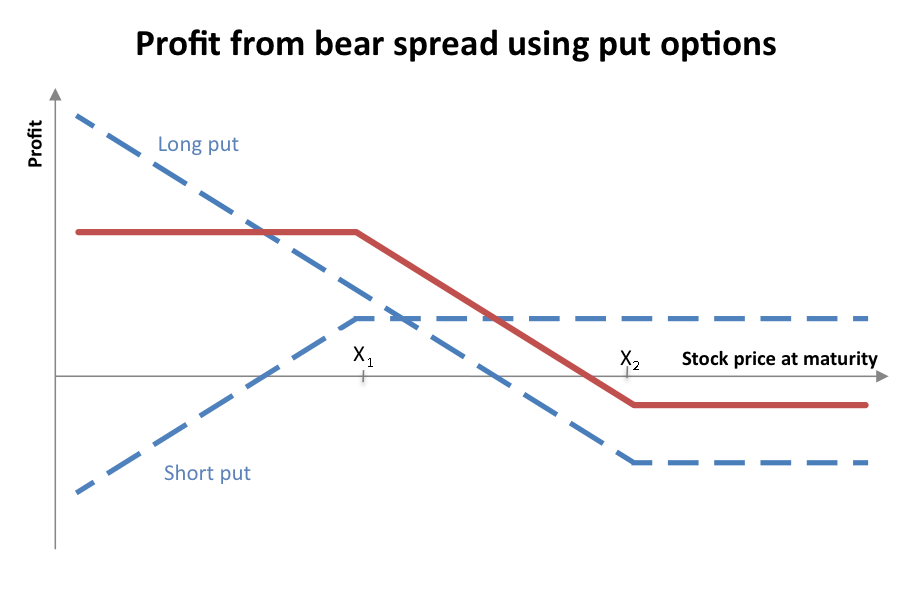

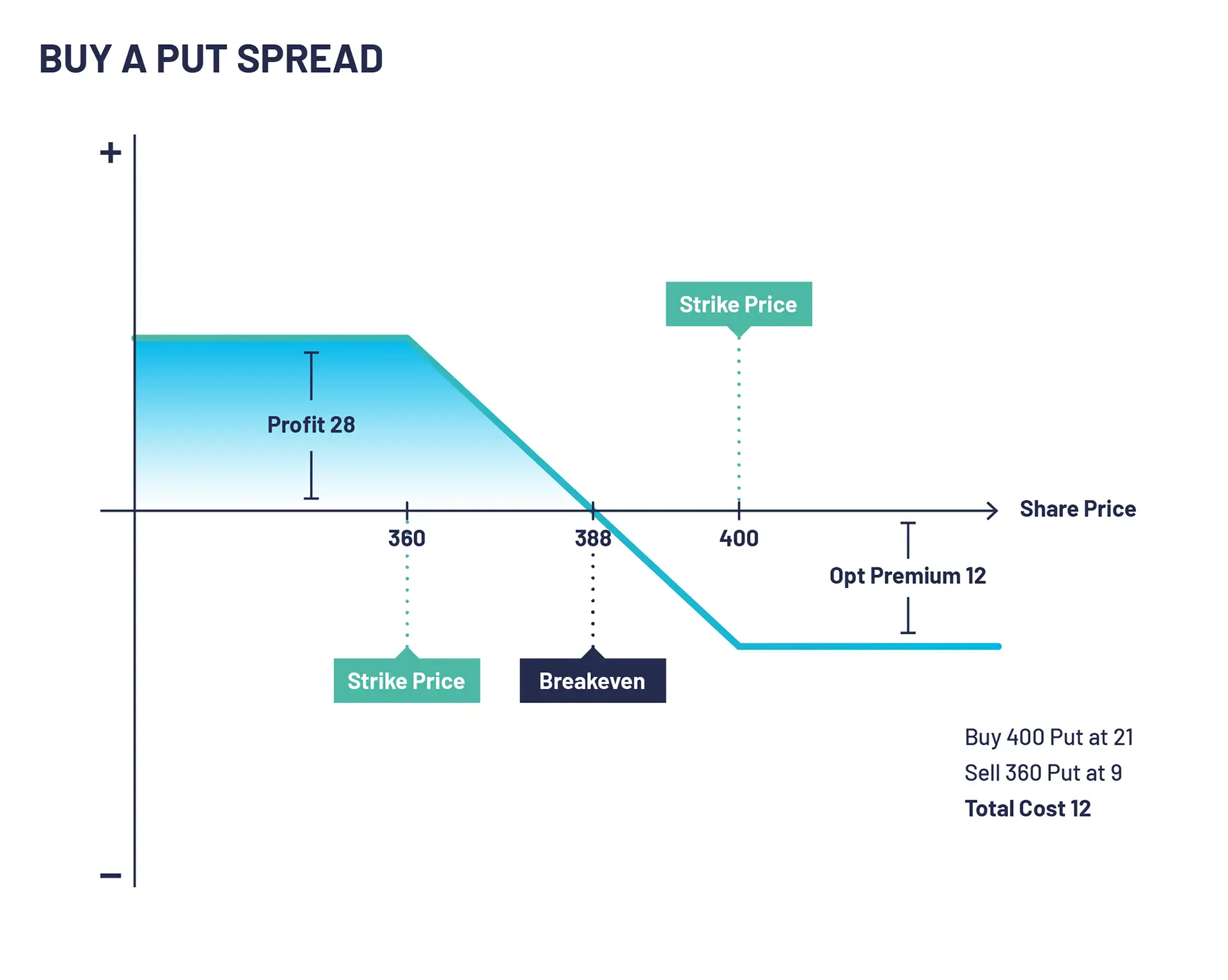

The bear put spread, also known as a debit put spread, is the most common type of put spread. It is established when a trader expects a moderate decline in the price of an underlying asset. To construct a bear put spread, a trader simultaneously buys a put option with a higher strike price and sells a put option with a lower strike price. Both options must have the same underlying asset and the same expiration date.

The goal of a bear put spread is to profit from a downward price movement, but with limited risk and limited profit potential. The premium paid for the higher strike put option is greater than the premium received for the lower strike put option, resulting in a net debit (cost) to establish the position. This net debit represents the maximum potential loss.

Key Components of a Bear Put Spread:

- Long Put (Higher Strike): This option gives the trader the right, but not the obligation, to sell the underlying asset at the higher strike price. This is the primary driver of profit if the underlying price falls.

- Short Put (Lower Strike): This option obligates the trader to buy the underlying asset at the lower strike price if the buyer of this option chooses to exercise it. This sale helps to offset the cost of the long put and defines the maximum profit.

Profit and Loss Scenarios for a Bear Put Spread:

-

Maximum Profit: The maximum profit is achieved when the price of the underlying asset at expiration is at or below the lower strike price. In this scenario, both put options are in the money. The profit is calculated as the difference between the strike prices minus the net debit paid to establish the spread.

- Formula: (Higher Strike Price – Lower Strike Price) – Net Debit Paid

-

Maximum Loss: The maximum loss is limited to the net debit paid to establish the spread. This occurs when the price of the underlying asset at expiration is at or above the higher strike price. In this situation, both put options expire worthless, and the trader loses the initial investment.

- Formula: Net Debit Paid

-

Breakeven Point: The breakeven point is the price at which the trader neither makes nor loses money. It is calculated by subtracting the net debit paid from the higher strike price.

- Formula: Higher Strike Price – Net Debit Paid

The bear put spread is favored by traders who believe the underlying asset will decline but are concerned about the risk of unlimited losses associated with a naked short put or the full premium cost of a single long put. It allows for a controlled bet on downside volatility.

Out-of-the-Money (OTM) Put Spread: A Cheaper, Lower Probability Strategy

An out-of-the-money (OTM) put spread is a variation of the bear put spread where both the long and short put options have strike prices below the current market price of the underlying asset. This means that at the time of establishment, neither option is in the money.

This strategy is generally cheaper to implement than a standard bear put spread because OTM options have lower premiums. However, it also has a lower probability of being profitable and offers a smaller potential profit. The OTM put spread is suitable for traders who anticipate a significant downward move in the underlying asset but are willing to accept a lower chance of success for a potentially higher return relative to the initial cost.

Construction of an OTM Put Spread:

- Long Put (Higher Strike, OTM): The trader buys a put option with a strike price below the current market price.

- Short Put (Lower Strike, OTM): The trader sells a put option with an even lower strike price, also below the current market price.

Profit and Loss Scenarios for an OTM Put Spread:

-

Maximum Profit: The maximum profit is achieved when the price of the underlying asset at expiration is at or below the lower strike price. Similar to the bear put spread, the profit is the difference between the strike prices minus the net debit.

- Formula: (Higher Strike Price – Lower Strike Price) – Net Debit Paid

-

Maximum Loss: The maximum loss is limited to the net debit paid. This occurs if the price of the underlying asset at expiration is at or above the higher strike price.

- Formula: Net Debit Paid

-

Breakeven Point: The breakeven point is calculated by subtracting the net debit paid from the higher strike price.

- Formula: Higher Strike Price – Net Debit Paid

The primary advantage of an OTM put spread is its lower initial cost, making it more accessible to traders with smaller capital. However, the significantly lower probability of the underlying asset moving enough to make both options profitable must be carefully considered.

The Strategic Advantages and Disadvantages of Put Spreads

Put spreads offer a nuanced approach to options trading, providing specific advantages but also inherent limitations. Understanding these trade-offs is crucial for traders deciding whether this strategy aligns with their objectives.

Strategic Advantages:

- Limited Risk: The most significant advantage of a put spread is its defined maximum loss. By selling a put option, the trader effectively caps their downside risk to the net premium paid. This is a stark contrast to simply buying a put option, where the entire premium can be lost if the underlying price moves against the trader’s expectation.

- Reduced Cost: Compared to buying a single, at-the-money (ATM) or in-the-money (ITM) put option, a bear put spread often has a lower initial cost. The premium received from selling the lower strike put helps to offset the cost of buying the higher strike put. This makes it a more capital-efficient way to express a bearish view.

- Defined Profit Potential: While profits are capped, they are also predictable. Knowing the maximum profit potential allows traders to set realistic expectations and manage their positions accordingly.

- Leveraged Downside Exposure: Put spreads allow traders to participate in the potential downward movement of an asset with a smaller capital outlay than shorting the underlying stock directly. This provides leveraged exposure to bearish price action.

- Flexibility in Outlook: Put spreads can be tailored to different degrees of bearishness. A bear put spread with strike prices closer to the current market price will be more sensitive to price movements and offer a higher potential profit (relative to cost) for a given decline, but with higher initial cost. Conversely, an OTM put spread is cheaper but requires a larger price drop for profitability.

Strategic Disadvantages:

- Limited Profit Potential: The flip side of limited risk is limited reward. The maximum profit is capped at the difference between the strike prices minus the net debit. This means that even if the underlying asset plummets far below the lower strike price, the profit will not exceed this predetermined amount.

- Lower Probability of Profit: Compared to simply buying a put option, a put spread generally has a lower probability of achieving its maximum profit. For the spread to be profitable, the underlying asset’s price must fall below the breakeven point. If it only falls to the breakeven point or stays above it, the trade results in a loss.

- Commissions and Fees: Like all options strategies, put spreads involve commissions for both legs of the trade (buying and selling). These costs can eat into profits, especially for smaller spreads or for traders who execute many trades.

- Assignment Risk (for the short put): The trader who sells the lower strike put option faces the risk of being assigned if the option is in-the-money at expiration. This means they would be obligated to buy the underlying asset at the strike price, even if the market price is significantly lower. While this is part of the strategy’s design, it’s a factor to be managed, especially if the trader doesn’t want to own the underlying asset.

- Time Decay (Theta): As expiration approaches, the value of options erodes due to time decay (theta). In a put spread, the short put option, being closer to the money or in-the-money, typically decays faster than the long put option (especially if it’s further OTM). This can be a disadvantage if the underlying asset doesn’t move quickly enough to offset the negative impact of theta.

When to Use a Put Spread

The decision to employ a put spread strategy hinges on a trader’s specific market outlook, risk tolerance, and capital availability. It is not a strategy for every market condition or every trader.

Expressing a Moderately Bearish View

The primary scenario for using a put spread is when a trader anticipates a decline in the price of an underlying asset but does not expect a catastrophic collapse. They believe the price will fall, but within a defined range. A bear put spread is particularly suitable for this outlook, offering a cost-effective way to profit from this moderate bearishness while providing protection against larger-than-expected price drops. For example, if a company releases earnings that are slightly disappointing, leading to an expectation of a modest price decline, a bear put spread could be considered.

Hedging a Portfolio

Traders who hold long positions in stocks or other assets may use put spreads as a hedging tool. If they are concerned about a potential short-term downturn in the market or a specific sector, they can implement put spreads on those holdings. This strategy can act as a form of insurance, limiting potential losses on their existing portfolio while allowing them to retain ownership of the underlying assets. The cost of the put spread is offset by the potential downside protection it provides.

Capitalizing on Volatility with Limited Risk

While often associated with bearish views, put spreads can also be used to express a view on volatility. If a trader expects implied volatility to increase, leading to higher put option premiums, but still wants to profit from a downward price move, a put spread can be implemented. The strategy can be attractive when the trader believes that current implied volatility is too low for the potential downside risk.

When NOT to Use a Put Spread

Conversely, there are situations where a put spread is not the optimal choice.

- Strongly Bullish Outlook: Naturally, a put spread is entirely unsuitable for traders with a bullish or neutral outlook on the underlying asset.

- Expectation of a Major Collapse: If a trader anticipates a severe and rapid decline in an asset’s price, the capped profit potential of a put spread might be too restrictive. In such extreme bearish scenarios, simply buying a put option might offer unlimited profit potential, albeit with a higher upfront cost and risk of losing the entire premium.

- Very Small Price Movements Expected: For very minor price fluctuations or sideways movement, the breakeven point of a put spread might be too difficult to achieve. The cost of establishing the spread, including commissions, could outweigh any potential small gains. In such cases, strategies like selling out-of-the-money put options might be more appropriate if a neutral to slightly bullish view is held.

- Limited Trading Capital: While put spreads can be cheaper than single puts, the transaction costs for both legs of the trade can add up. For traders with very limited capital, the commissions might make the strategy uneconomical.

In conclusion, a put spread is a versatile yet specific options strategy. It offers a controlled method for traders to express a moderately bearish view, hedge existing positions, or capitalize on expected price movements with defined risk and reward. Its effectiveness lies in its ability to balance the desire for profit from a declining market with the prudence of limiting potential losses, making it a valuable tool in the options trader’s arsenal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.