A profit sharing 401(k) plan is a powerful retirement savings vehicle that combines the popular tax-advantaged savings of a traditional 401(k) with a unique employer contribution component: profit sharing. This means employers can share a portion of their company’s profits directly with their employees in the form of retirement savings, offering a compelling incentive for both parties. For employees, it represents an additional, often unexpected, boost to their retirement nest egg, potentially accelerating their savings journey. For employers, it serves as a valuable tool for employee retention, recruitment, and as a way to reward hard work and company success. Understanding the intricacies of this plan is crucial for anyone looking to optimize their retirement strategy or for businesses seeking to enhance their employee benefits package.

Understanding the Core Components: 401(k) and Profit Sharing

At its heart, a profit sharing 401(k) plan is a hybrid. It builds upon the foundational principles of a traditional 401(k) while integrating the employer’s discretionary profit-sharing contributions. This symbiotic relationship creates a robust retirement savings solution.

The Traditional 401(k) Foundation

The 401(k) plan, named after the section of the Internal Revenue Code that governs it, has become a cornerstone of retirement planning in the United States. Its primary appeal lies in its tax advantages. Employees can contribute a portion of their pre-tax income directly from their paycheck, which reduces their current taxable income. This means they pay taxes on that money later, typically in retirement when their tax bracket may be lower.

Employee Contributions: Building Your Own Nest Egg

Employees have the power to decide how much they want to contribute to their 401(k), up to annual limits set by the IRS. These contributions are often made through payroll deductions, making saving automatic and consistent. The money invested within the 401(k) grows tax-deferred, meaning any earnings, interest, or dividends are not taxed until withdrawal in retirement. This compounding effect, over decades, can significantly enhance the total retirement savings. Many plans also offer a Roth 401(k) option, where contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free.

Investment Options: Tailoring Your Retirement Portfolio

Within a 401(k) plan, employees typically have a menu of investment options to choose from. These can range from conservative options like money market funds and stable value funds to more aggressive choices like stock mutual funds and bond funds. Some plans also offer target-date funds, which automatically adjust their asset allocation to become more conservative as the participant approaches their target retirement date. The employee is responsible for selecting investments that align with their risk tolerance and financial goals.

Vesting Schedules: Earning Ownership of Employer Contributions

While employee contributions are always 100% vested (meaning they are immediately owned by the employee), employer contributions, including profit sharing, are often subject to a vesting schedule. A vesting schedule dictates the timeline over which an employee earns full ownership of the employer’s contributions. Common schedules include cliff vesting, where employees become fully vested after a certain period of service (e.g., three years), or graded vesting, where a percentage of the employer contribution vests each year over a longer period. Understanding your vesting schedule is crucial, as leaving the company before becoming fully vested means forfeiting some or all of the employer’s contributions.

The Profit Sharing Element: An Employer’s Generous Gift

Profit sharing is a discretionary contribution that an employer makes to employee retirement accounts based on the company’s profitability. Unlike matching contributions, which are tied to employee contributions, profit sharing is purely a function of the employer’s financial performance and their willingness to share that success.

Discretionary Contributions: Flexibility for Employers

The “discretionary” nature of profit sharing is a key characteristic. Employers are not obligated to make a profit sharing contribution in any given year. The decision to contribute, and the amount of the contribution, is typically determined by the company’s board of directors or management, often based on predefined formulas or simply as a reward for a strong financial quarter or year. This flexibility allows businesses to manage their cash flow effectively while still offering a valuable benefit.

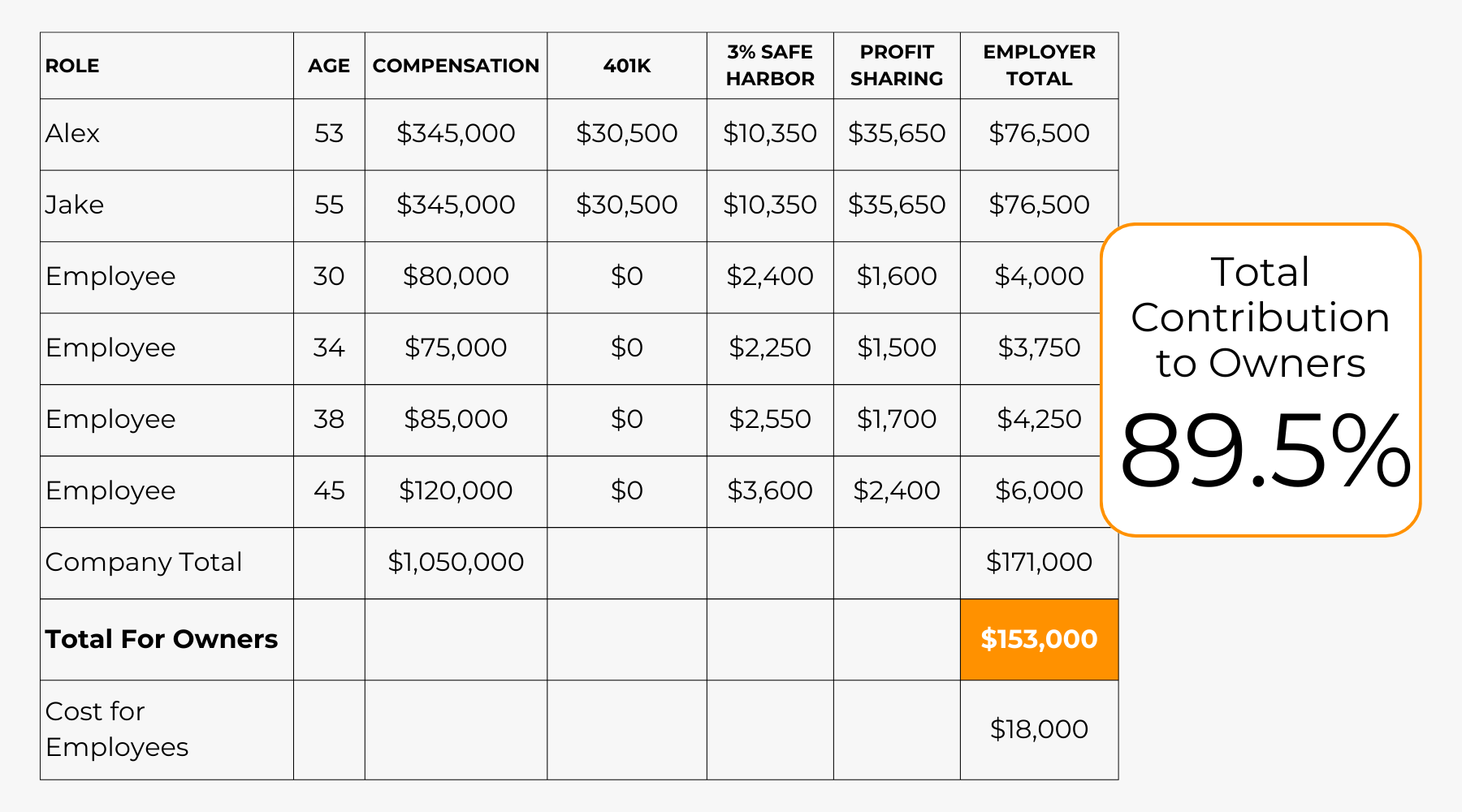

Allocation Methods: How Profits Are Shared

There are several common methods for allocating profit sharing contributions among eligible employees. The most prevalent include:

- Pro-rata Allocation: This method allocates profit sharing contributions in proportion to each employee’s compensation. Employees who earn more receive a larger share of the profit sharing contribution.

- Integrated Allocation: This method considers both compensation and Social Security contributions. It allows for a more significant allocation to lower-paid employees compared to a pure pro-rata method, as it “integrates” the employer contribution with what would have been covered by Social Security taxes.

- New Comparability Allocation: This is a more complex method that allows employers to allocate contributions based on specific employee demographics or groups, often to favor highly compensated employees within legal limits, or to provide more generous contributions to specific groups. However, these plans are subject to stringent non-discrimination testing to ensure they do not unfairly benefit highly compensated employees over non-highly compensated employees.

The chosen allocation method is a critical design feature of the plan and can significantly impact how much each employee receives.

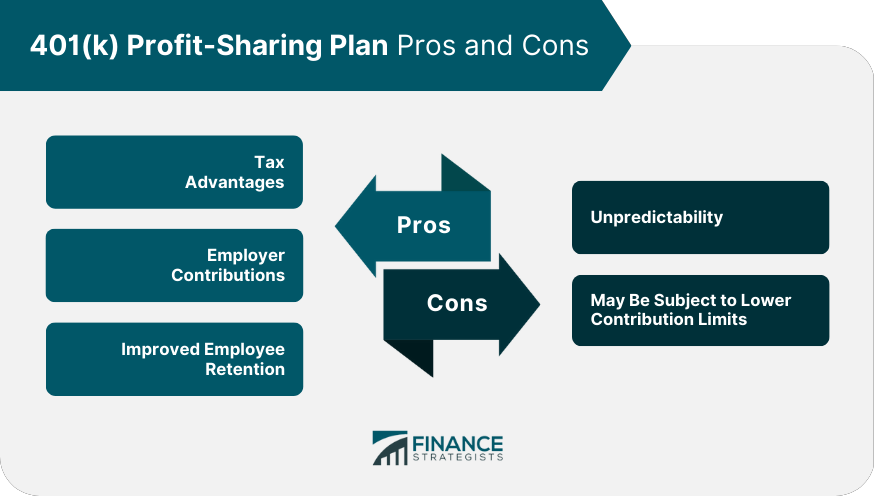

Benefits of a Profit Sharing 401(k) Plan

The dual nature of the profit sharing 401(k) plan offers a multitude of advantages for both employees and employers, fostering a mutually beneficial relationship.

Advantages for Employees: Accelerating Retirement Savings

For employees, the profit sharing 401(k) is a powerful tool for wealth accumulation. It goes beyond what they can save from their own paycheck.

Increased Savings Potential

The most obvious benefit is the potential for significantly higher retirement savings. An employer’s profit sharing contribution is essentially “free money” that boosts the employee’s retirement account balance, often without any direct effort on their part beyond meeting basic eligibility requirements. This can be particularly impactful for those who may struggle to save enough on their own or who are later in their careers and need to catch up on their retirement savings.

Enhanced Financial Security and Motivation

Knowing that their employer is invested in their future financial well-being can foster a greater sense of loyalty and motivation among employees. The prospect of receiving a profit sharing contribution can be a strong incentive to perform well and contribute to the company’s success. It creates a tangible link between individual and company performance, reinforcing the idea that everyone benefits when the company thrives. This can lead to increased job satisfaction and a stronger commitment to the organization.

Tax Advantages on Employer Contributions

Similar to employee contributions, employer profit sharing contributions are also tax-advantaged. They are tax-deductible for the employer and are not considered taxable income for the employee until withdrawal in retirement. This means the entire profit sharing contribution grows tax-deferred, further maximizing its long-term impact on retirement savings.

Advantages for Employers: Attracting and Retaining Talent

Businesses that offer profit sharing 401(k) plans gain a competitive edge in the labor market and cultivate a more engaged workforce.

Competitive Recruitment Tool

In today’s competitive job market, attractive employee benefits are no longer a luxury but a necessity. A profit sharing 401(k) plan can be a significant differentiator, making a company more appealing to top talent. It signals that the employer values its employees and is willing to share the company’s success, which can attract candidates who are looking for more than just a salary.

Improved Employee Retention and Loyalty

Employees who feel valued and are rewarded for their contributions are more likely to stay with a company. Profit sharing directly links employee efforts to financial rewards, fostering a sense of shared purpose and increasing loyalty. This can significantly reduce employee turnover, which is costly for businesses in terms of recruitment, training, and lost productivity.

Performance-Based Incentive and Morale Booster

Profit sharing acts as a powerful performance-based incentive. When employees see that their hard work contributes to the company’s profits and, in turn, to their own retirement savings, it can drive higher levels of productivity and engagement. It creates a positive feedback loop where success is celebrated and shared, boosting overall morale and fostering a culture of collaboration and achievement.

Tax Benefits for the Company

Employer contributions to profit sharing 401(k) plans are tax-deductible business expenses. This reduces the company’s taxable income, providing a direct financial benefit. This makes it a cost-effective way for businesses to reward employees and invest in their retirement security.

Key Considerations and Plan Administration

While the benefits are substantial, implementing and managing a profit sharing 401(k) plan requires careful consideration and ongoing administration.

Eligibility Requirements and Contribution Limits

To participate in a profit sharing 401(k) plan, employees typically need to meet certain eligibility criteria. These can include age requirements (e.g., age 21) and minimum service periods (e.g., employed for 12 months and worked at least 1,000 hours). These requirements are designed to ensure that contributions are made to employees who have a demonstrated commitment to the company.

IRS Contribution Limits

Both employee and employer contributions are subject to annual limits set by the IRS. These limits are designed to ensure that retirement plans serve their intended purpose of providing retirement security and are not used primarily for tax avoidance. The total amount that can be contributed to an individual’s 401(k) plan (from both employee and employer, including profit sharing and any employer match) is capped annually. It’s crucial for plan administrators and participants to stay informed about these limits.

Non-Discrimination Testing

A critical aspect of administering any 401(k) plan, especially those with profit sharing, is non-discrimination testing. The IRS mandates these tests to ensure that retirement plans do not unfairly benefit highly compensated employees (HCEs) over non-highly compensated employees (NHCEs).

Average Deferral Percentage (ADP) and Average Contributions Percentage (ACP) Tests

These tests compare the average contribution rates of HCEs to those of NHCEs. If the plan fails these tests, employers may need to take corrective actions, such as refunding excess contributions to HCEs or making additional contributions to NHCEs. Profit sharing formulas, especially integrated or new comparability designs, can make these tests more complex.

Top-Heavy Testing

If more than 60% of the plan’s assets are held by key employees (which typically include officers and those owning more than 5% of the company), the plan is considered “top-heavy.” In such cases, the employer is required to make a minimum contribution to non-key employees to satisfy the top-heavy requirements.

Choosing a Plan Administrator and Investment Fiduciaries

Selecting the right plan administrator is paramount to the success of a profit sharing 401(k) plan. The administrator is responsible for record-keeping, compliance, and often provides participant education.

Roles and Responsibilities

Plan administrators handle the day-to-day operations, including processing contributions, managing distributions, and ensuring compliance with regulatory requirements. Employers also have a fiduciary responsibility to act in the best interest of plan participants, which includes selecting a qualified administrator, offering appropriate investment options, and ensuring fees are reasonable.

Investment Selection and Monitoring

The selection of investment options within the plan is another critical responsibility. Plan sponsors must offer a diverse range of investment choices that are suitable for retirement savers. They are also responsible for periodically reviewing and monitoring these investments to ensure they remain appropriate and that fees are competitive. This involves due diligence and a commitment to acting in the best interests of the plan participants.

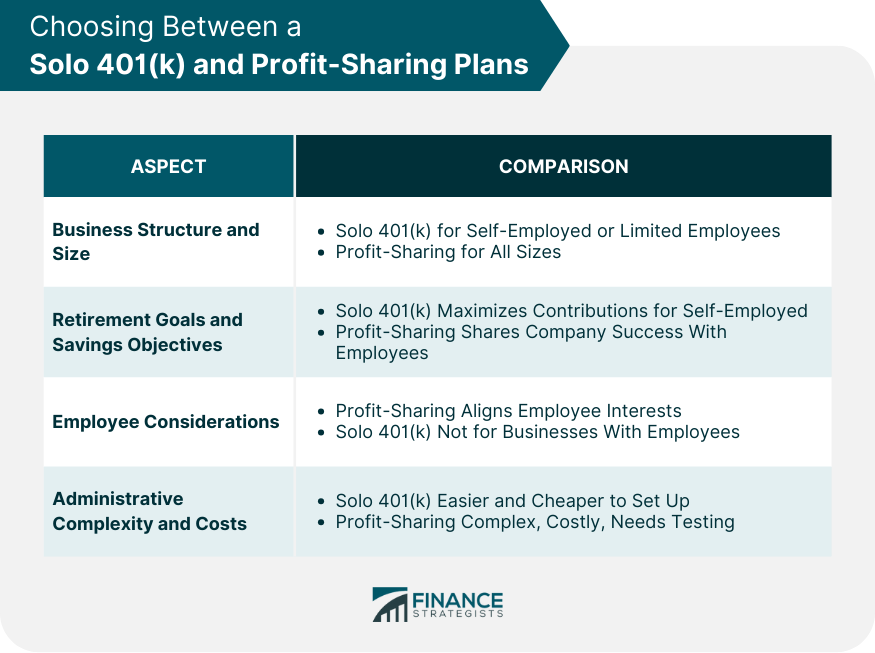

Is a Profit Sharing 401(k) Plan Right for You?

Deciding whether to participate in a profit sharing 401(k) plan or to implement one as an employer depends on individual circumstances and business objectives.

For Employees: Maximizing Your Retirement Potential

As an employee, if your employer offers a profit sharing 401(k), it’s an opportunity you should seriously consider.

Assess Your Current Savings and Future Needs

Evaluate your current retirement savings and project your future needs. A profit sharing contribution can significantly accelerate your journey towards financial independence in retirement. Even if you already have a robust savings plan, the additional contributions can provide valuable diversification and growth potential.

Understand Your Plan’s Specifics

Take the time to understand the details of your plan. Know your eligibility requirements, vesting schedule, the profit sharing allocation method, and the investment options available. This knowledge will empower you to make informed decisions and maximize the benefits of the plan.

For Employers: Enhancing Your Benefits Strategy

For business owners and HR professionals, a profit sharing 401(k) can be a strategic addition to their benefits package.

Evaluate Your Company’s Financial Health and Goals

Consider your company’s financial stability and long-term goals. Profit sharing is tied to profitability, so ensure your business can comfortably sustain these contributions. It’s an excellent way to reward success and motivate your team, but it must be financially viable.

Weigh the Costs and Benefits of Implementation

While there are administrative costs and the direct expense of contributions, the benefits in terms of employee attraction, retention, and morale can far outweigh these costs. Conduct a thorough cost-benefit analysis to determine if a profit sharing 401(k) aligns with your overall business strategy and HR objectives. Seeking advice from a qualified financial advisor or benefits consultant can be invaluable in this decision-making process.

In conclusion, a profit sharing 401(k) plan offers a compelling synergy of individual savings power and employer generosity, creating a potent engine for retirement wealth accumulation. For employees, it’s a chance to significantly boost their nest egg and feel more invested in their company’s success. For employers, it’s a strategic tool to attract, retain, and motivate a high-performing workforce, all while enjoying valuable tax benefits. Understanding its components, advantages, and administrative considerations is key to harnessing its full potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.