The term “plan sponsor” is fundamental to understanding a vast array of financial arrangements, particularly those that facilitate wealth accumulation and security for individuals. While the concept might initially sound niche, it underpins critical aspects of both personal and business finance, impacting retirement savings, employee benefits, and investment strategies. Essentially, a plan sponsor is the entity that establishes and oversees a financial plan or program. This encompasses a wide spectrum, from large corporations offering retirement benefits to individuals setting up investment accounts for themselves or others.

Understanding the role and responsibilities of a plan sponsor is crucial for anyone involved in managing or participating in such programs. Whether you’re an employer considering offering employee benefits, an investor seeking to establish a structured savings vehicle, or an individual beneficiary of a sponsored plan, grasping the intricacies of plan sponsorship can lead to better financial outcomes and informed decision-making. This article will delve into the multifaceted nature of plan sponsors, exploring their various forms, their core duties, and the profound implications of their role in the realm of finance.

The Diverse Landscape of Plan Sponsors

Plan sponsors are not a monolithic entity; their nature and scope vary significantly depending on the context. The most common associations are with retirement plans, but the principle extends to other financial programs. Identifying the different types of plan sponsors is the first step to appreciating their impact.

Corporate Retirement Plan Sponsors

This is perhaps the most widely recognized category. Corporations, non-profit organizations, and government entities act as plan sponsors when they establish and manage retirement plans for their employees. The most prevalent of these are:

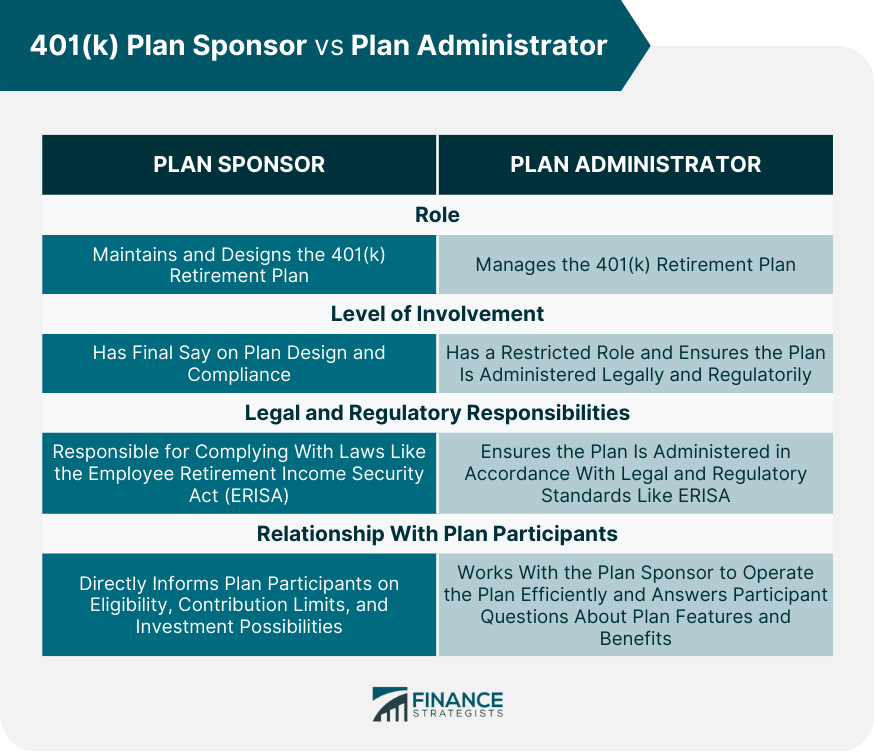

- 401(k) Plans: In the United States, these employer-sponsored defined contribution plans allow employees to save for retirement on a tax-deferred basis. The company, as the plan sponsor, selects the investment options, handles administrative duties (often through a third-party administrator), and is responsible for ensuring compliance with regulations like the Employee Retirement Income Security Act (ERISA).

- 403(b) Plans: Similar to 401(k)s, these are retirement savings plans for employees of public schools, colleges, universities, hospitals, and certain religious organizations. The sponsoring organization manages the plan, choosing eligible investment providers and ensuring adherence to legal requirements.

- Pension Plans (Defined Benefit Plans): While less common than in the past, some employers still offer defined benefit plans, where the sponsor guarantees a specific retirement benefit amount to employees, often based on salary and years of service. The sponsor bears the investment risk and is responsible for funding the promised benefits.

- Small Business Retirement Plans (e.g., SIMPLE IRA, SEP IRA): For smaller businesses, plans like the Savings Incentive Match Plan for Employees (SIMPLE) IRA and the Simplified Employee Pension (SEP) IRA serve as accessible retirement savings vehicles. The business owner or entity acts as the plan sponsor, making contributions and managing the plan’s administration.

In these corporate settings, the plan sponsor’s primary motivation is often to attract and retain talent, provide a valuable employee benefit, and foster a culture of financial well-being among their workforce. The financial implications for the sponsoring organization can include tax deductions for contributions and the potential for increased employee loyalty and productivity.

Individual Plan Sponsors

Beyond the corporate realm, individuals can also act as plan sponsors, particularly when establishing financial plans for themselves or others, often with a long-term savings or investment objective.

- Self-Directed Retirement Accounts: An individual can act as their own plan sponsor for individual retirement accounts (IRAs) like Traditional IRAs and Roth IRAs. While these are not employer-sponsored, the individual is responsible for making contributions, selecting investments, and adhering to IRS rules. The government, through its tax legislation, essentially “sponsors” the concept of these accounts by providing tax advantages.

- Trusts and Estates: Individuals can establish trusts for the benefit of beneficiaries, appointing a trustee to manage assets according to the trust document. In this scenario, the grantor of the trust, who sets up the terms, can be considered an initial plan sponsor, with the trustee taking on ongoing administrative responsibilities. These trusts can hold various assets, including investments intended for long-term growth.

- Custodial Accounts for Minors (e.g., UGMA/UTMA): Parents or guardians can open custodial accounts for minors under the Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA). The adult donor acts as the plan sponsor, depositing assets into the account, which the minor will control upon reaching the age of majority. The sponsor’s goal is to provide a financial head start or fund future needs like education.

The motivations for individual plan sponsorship are typically personal: saving for retirement, providing for family, or accumulating wealth for specific future goals. The emphasis here is on personal financial planning and the proactive management of one’s own financial future.

Other Forms of Sponsorship

The concept of a plan sponsor can also extend to less conventional but equally important financial arrangements:

- Non-Profit Organizations and Foundations: These entities may sponsor programs aimed at financial education, grants, or scholarship funds. While not always direct investment plans, they “sponsor” financial initiatives designed to benefit specific groups or causes.

- Government Programs: While not a “sponsor” in the corporate sense, government initiatives like Social Security or Medicare can be viewed as large-scale, government-sponsored financial programs designed for broad public benefit.

The Responsibilities and Duties of a Plan Sponsor

The role of a plan sponsor is far from passive. It involves a significant set of responsibilities, legal obligations, and fiduciary duties, particularly when dealing with retirement plans for employees. These duties are designed to protect the interests of the plan participants.

Fiduciary Responsibilities

For employers sponsoring retirement plans, the most critical aspect of their role is acting as a fiduciary. This means they must act in the best interests of the plan participants and beneficiaries, exercising prudence and loyalty. Key fiduciary duties include:

- Prudent Management: Plan sponsors must act with the care, skill, and diligence that a prudent person familiar with such matters would use in conducting a similar enterprise. This applies to investment decisions, plan administration, and vendor selection.

- Loyalty: The sponsor’s primary allegiance must be to the plan participants, not to their own interests or the interests of the company, except where those align with the participants’ best interests.

- Diversification: Plan sponsors have a duty to ensure that plan assets are diversified to minimize the risk of large losses, unless it is prudent not to do so.

- Acting Solely in the Interest of Participants: All actions taken by the plan sponsor must be for the exclusive benefit of the plan participants and beneficiaries. This includes ensuring that plan expenses are reasonable.

- Avoiding Conflicts of Interest: Sponsors must avoid situations where their personal interests conflict with their fiduciary duties to the plan.

Administrative and Operational Duties

Beyond fiduciary obligations, plan sponsors are responsible for the day-to-day operations and administration of the plan. This often involves:

- Selecting and Monitoring Service Providers: Sponsors must carefully select and continuously monitor third-party administrators, recordkeepers, investment managers, and other service providers to ensure they are performing their duties effectively and at a reasonable cost.

- Establishing and Maintaining Plan Documents: This includes creating a comprehensive plan document that outlines the rules and procedures of the plan, as well as summary plan descriptions (SPDs) that clearly communicate the plan’s benefits and features to participants.

- Ensuring Compliance with Regulations: Plan sponsors must stay abreast of and comply with all applicable federal and state laws and regulations, such as ERISA, the Internal Revenue Code, and Department of Labor guidelines. This includes filing required reports with government agencies.

- Processing Contributions and Distributions: For retirement plans, this involves ensuring that employee and employer contributions are made accurately and on time, and that participant distribution requests are handled promptly and correctly.

- Recordkeeping: Maintaining accurate and up-to-date records of all plan transactions, participant accounts, and relevant documentation is crucial.

Communication and Education

An often-underestimated but vital duty of a plan sponsor is effective communication with plan participants. This involves:

- Providing Clear and Timely Information: Participants need to understand their benefits, investment options, fees, and how to access their funds. This includes providing regular statements and making plan documents accessible.

- Offering Educational Resources: Many sponsors go beyond basic communication to offer financial literacy and retirement planning education. This can empower participants to make informed investment decisions and plan effectively for their future.

- Responding to Inquiries: Plan sponsors must have a system in place to answer participant questions and address concerns in a timely and helpful manner.

The complexity of these responsibilities highlights why many organizations outsource some of these functions to specialized financial service providers. However, the ultimate responsibility and liability for the plan typically remain with the plan sponsor.

The Significance of Plan Sponsorship in Financial Planning

The role of a plan sponsor is intrinsically linked to the success of financial planning for individuals and the financial health of organizations. Their decisions and actions have far-reaching consequences.

Impact on Employee Benefits and Retirement Security

For businesses, being a plan sponsor is a strategic decision that directly impacts their ability to attract and retain top talent. Offering competitive retirement benefits can be a significant differentiator in the job market. From the employee’s perspective, a well-managed and generously sponsored plan is a cornerstone of their retirement security. The quality of investment options, the level of employer contributions, and the overall administration of the plan can dramatically influence how prepared an individual is for life after work. A responsible plan sponsor fosters an environment where employees can confidently build their retirement nest egg.

Influence on Investment Performance and Cost

The plan sponsor’s choice of investment options and service providers directly affects the performance of the plan’s assets and the fees participants pay. A vigilant sponsor will regularly review investment performance, benchmark fees against industry standards, and select providers that offer a good balance of performance, services, and cost. Poor investment selection or excessive fees can significantly erode returns over time, diminishing the value of the plan for participants. Conversely, a sponsor committed to transparency and fiduciary duty can help optimize investment outcomes and minimize costs.

Contribution to Financial Literacy and Well-being

Beyond the direct financial aspects, plan sponsors play a crucial role in promoting financial literacy. By providing educational resources and encouraging informed decision-making, they empower individuals to take greater control of their financial futures. This can extend beyond retirement planning to encompass broader financial wellness, which can positively impact employee morale, productivity, and overall quality of life. A sponsor that invests in its employees’ financial education is investing in their long-term success and the stability of the organization.

Risk Management and Compliance

For the sponsoring entity, acting as a plan sponsor involves inherent risks, particularly regarding compliance with complex regulations. Failure to meet fiduciary duties or adhere to legal requirements can result in significant financial penalties, litigation, and reputational damage. Therefore, a robust risk management framework is essential. This includes understanding the legal landscape, implementing strong internal controls, and seeking expert advice when necessary. A diligent plan sponsor proactively mitigates these risks, ensuring the integrity and sustainability of the financial programs they oversee.

Navigating the Role of a Plan Sponsor

For entities considering becoming a plan sponsor, or those currently in this role, understanding the landscape and proactively managing responsibilities is paramount. The decision to sponsor a financial plan, especially for employees, is a significant commitment that requires careful consideration and ongoing diligence.

Due Diligence Before Sponsorship

Before establishing a plan, potential sponsors must conduct thorough due diligence. This involves:

- Assessing Needs: Clearly defining the objectives of the plan. Is it primarily for employee retention, tax benefits, or to foster a specific financial behavior?

- Understanding Legal and Regulatory Requirements: Familiarizing oneself with all applicable laws and regulations, such as ERISA, and understanding the fiduciary responsibilities that will be assumed.

- Evaluating Costs and Resources: Determining the financial investment required for contributions, administration, and potential service provider fees. Assessing the internal resources available for plan management.

- Researching Service Providers: Investigating potential third-party administrators, recordkeepers, and investment managers, considering their experience, reputation, fee structures, and services offered.

Ongoing Management and Oversight

Once a plan is established, continuous oversight is critical. This includes:

- Regular Performance Reviews: Periodically reviewing the performance of investments and service providers against established benchmarks.

- Fee Analysis: Continuously evaluating the reasonableness of plan fees and seeking cost efficiencies where possible without compromising quality.

- Compliance Monitoring: Staying updated on regulatory changes and ensuring the plan remains in compliance with all legal requirements.

- Participant Engagement: Actively engaging with participants to ensure they understand the plan and have access to the resources they need. This may involve soliciting feedback and making adjustments as necessary.

Seeking Expert Advice

Given the complexity of financial regulations and investment management, plan sponsors should not hesitate to seek expert advice. This can include:

- Legal Counsel: To ensure compliance with all relevant laws and to navigate any legal complexities.

- Financial Advisors and Consultants: To assist with investment selection, fiduciary guidance, and plan design.

- Third-Party Administrators (TPAs): To handle the day-to-day administrative tasks of the plan.

By approaching plan sponsorship with a strategic mindset, a commitment to fiduciary duty, and a proactive approach to management, entities can effectively fulfill their roles, benefiting both themselves and the participants of the financial plans they oversee. The designation of “plan sponsor” carries weight, signifying a commitment to financial well-being and responsible stewardship of assets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.