Money market accounts (MMAs) often emerge in conversations about personal finance and investing, positioned as a secure and accessible place to park your savings. But what exactly is a money market account, and how does it fit into a broader financial strategy? Far from being a complex investment vehicle, an MMA is fundamentally a type of savings account offered by banks and credit unions that typically offers a higher interest rate than a traditional savings account, with the added benefit of limited check-writing privileges and debit card access. This makes them a popular choice for individuals looking for a safe haven for their liquid assets, bridging the gap between a standard savings account and more volatile investment options.

Understanding the nuances of MMAs is crucial for making informed decisions about where to allocate your funds. While they offer attractive features, it’s important to recognize their limitations and compare them against other financial products. This article will delve into the core characteristics of money market accounts, explore their advantages and disadvantages, differentiate them from similar financial instruments, and provide guidance on how to best utilize them within a personal financial plan.

The Core Characteristics of a Money Market Account

At its heart, a money market account is a deposit account that blends features of both savings and checking accounts, with a distinct focus on providing a modest return on your funds. Unlike traditional savings accounts that primarily earn interest, MMAs are designed to offer a more competitive Annual Percentage Yield (APY) while still maintaining a high degree of liquidity and safety. This distinction is vital for anyone looking to earn more on their cash without taking on significant risk.

Interest Rates and APY

The primary allure of a money market account is its interest rate. MMAs generally offer higher interest rates than standard savings accounts. This is because the funds deposited into MMAs are often pooled by the financial institution and invested in short-term, low-risk, highly liquid debt instruments, such as Treasury bills, certificates of deposit (CDs), and commercial paper. These investments are considered very safe and provide a steady stream of income, which the bank can then pass on to account holders in the form of higher interest.

The Annual Percentage Yield (APY) is the key metric to watch. APY takes into account the effect of compounding interest, providing a more accurate picture of the actual return on your investment over a year. When comparing MMAs from different institutions, always look at the advertised APY. It’s also important to note that MMA interest rates are variable, meaning they can fluctuate based on prevailing market interest rates. During periods of rising interest rates, your MMA APY can increase, while during periods of falling rates, it may decrease.

Liquidity and Access to Funds

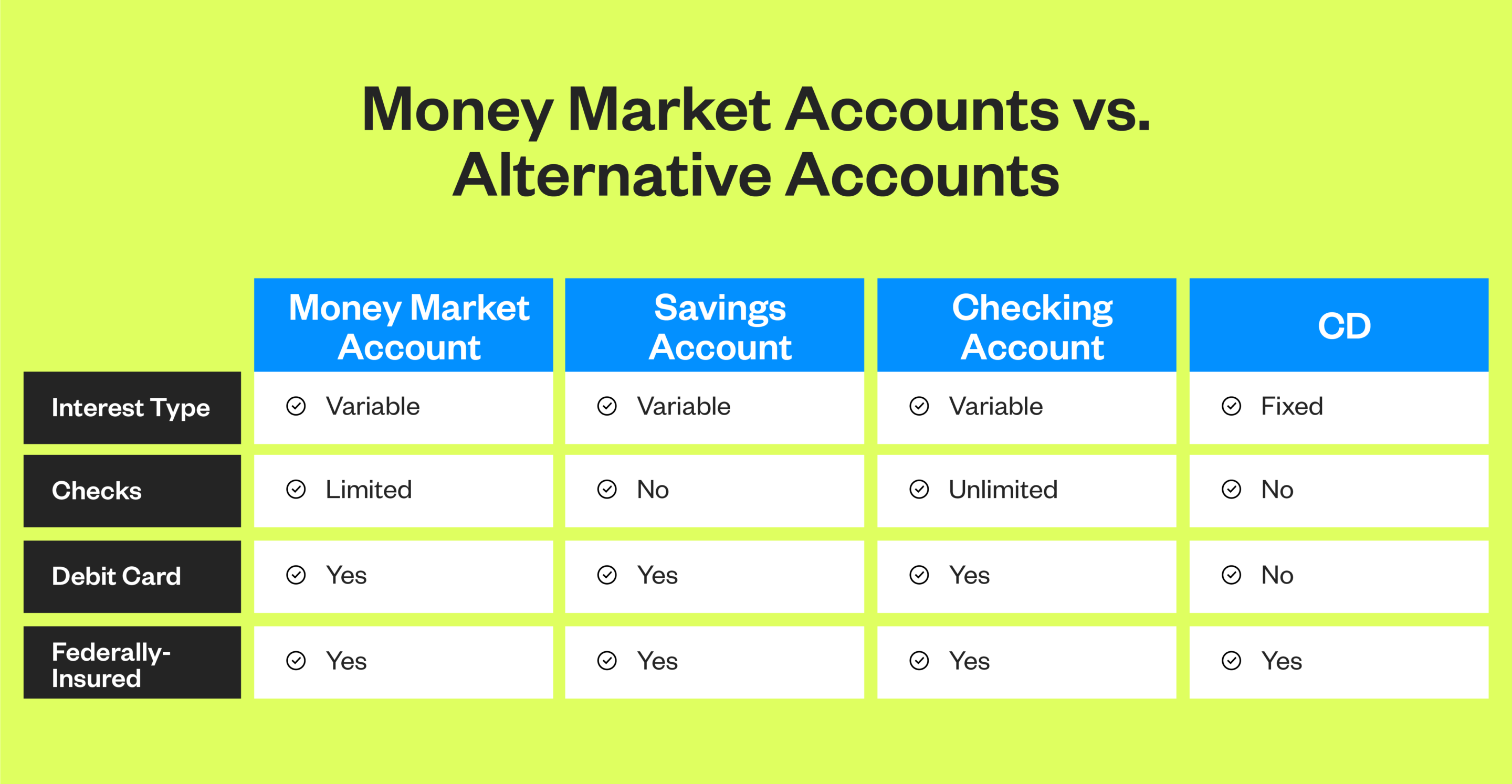

Liquidity refers to how easily you can access your money. Money market accounts are designed for liquidity, meaning you can withdraw funds relatively quickly and easily. This is a significant advantage over investments like CDs, which typically penalize you for early withdrawal. MMAs usually come with check-writing privileges, allowing you to write a limited number of checks directly from your account. Many also offer a debit card for ATM withdrawals and point-of-sale purchases.

However, it’s crucial to be aware of the regulatory limitations on access. Under federal regulations (specifically, Regulation D, though some aspects have been relaxed), MMAs are typically limited to six “convenient withdrawals and transfers” per month to another account, or by check, debit card, or electronic payment. Exceeding this limit can result in fees or even the conversion of your MMA to a standard checking account. This “six-transaction rule” is a key differentiator from traditional checking accounts and is intended to maintain the MMA’s status as a savings vehicle rather than a transactional account.

Safety and Deposit Insurance

One of the most compelling reasons to choose a money market account is its safety. Like traditional savings and checking accounts, MMAs offered by banks are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor, per insured bank, for each account ownership category. Similarly, MMAs offered by credit unions are insured by the National Credit Union Administration (NCUA) for the same amount. This federal insurance provides a strong guarantee that your principal is protected, even if the financial institution fails.

This inherent safety distinguishes MMAs from other investment vehicles like mutual funds or stocks, which carry market risk and are not federally insured. The underlying investments of a money market fund (a different product, discussed later) are subject to market fluctuations, but the deposits in a money market account are direct obligations of the bank and are protected by FDIC or NCUA insurance.

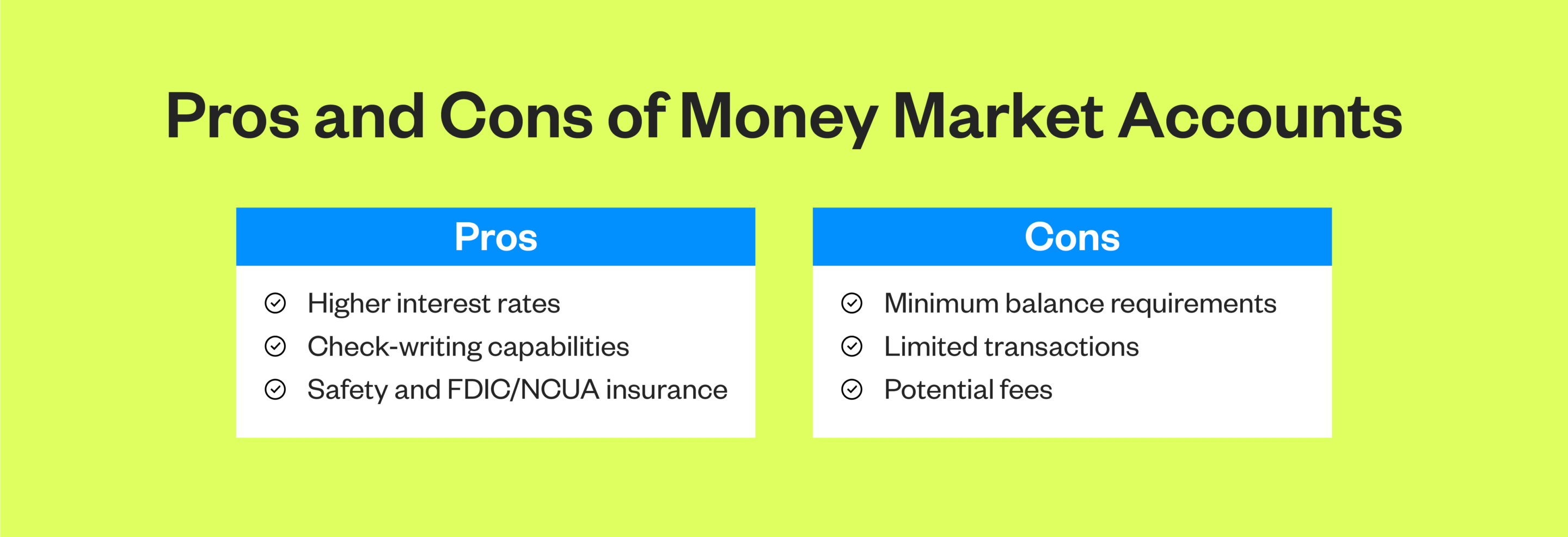

Advantages of Money Market Accounts

Money market accounts offer a compelling blend of accessibility, safety, and a competitive return, making them a valuable tool for various financial goals. Their structure provides a practical solution for individuals looking to grow their savings without venturing into riskier investments.

Earning a Higher Yield Than Traditional Savings

The most immediate advantage is the potential for a higher APY compared to standard savings accounts. While the difference may seem small on a few hundred dollars, it can translate into significant earnings over time, especially on larger balances. This is particularly attractive in an environment where inflation might be eroding the purchasing power of your cash. By choosing an MMA, you’re giving your money a better chance to keep pace with or even outpace inflation, thereby preserving and growing your wealth. This higher yield is a direct benefit of the financial institution’s ability to invest pooled funds in slightly more lucrative, yet still low-risk, instruments.

Preservation of Principal

For many individuals, the primary goal for holding money in an account is to keep it safe. Money market accounts excel in this regard. As mentioned, they are federally insured, meaning your initial deposit is protected up to the insurance limits. This security provides peace of mind, especially for funds that are earmarked for short-term goals like a down payment on a house, an emergency fund, or upcoming expenses. The focus of the underlying investments in low-risk debt instruments further reinforces the stability of your principal. You are not exposed to the volatility of the stock market, ensuring that your balance won’t significantly decrease due to market downturns.

Convenient Access to Funds

While offering a better yield than traditional savings, MMAs don’t significantly compromise on accessibility. The ability to write checks or use a debit card provides a level of convenience that is usually associated with checking accounts. This makes them ideal for managing a portion of your funds that you might need access to on relatively short notice, without the hassle of transferring money from a less accessible account. For instance, you might use an MMA to hold funds for a vacation you plan to take in a few months, knowing you can easily access the money if needed, while still earning a better interest rate than a regular savings account.

Flexibility for Short-to-Medium Term Goals

The combination of a decent return and good liquidity makes MMAs well-suited for a variety of short-to-medium term financial goals. This could include building an emergency fund, saving for a down payment on a car or home, accumulating funds for a large purchase, or even holding money before investing it in longer-term assets. By keeping these funds in an MMA, they are working for you by earning interest, rather than sitting idle in a low-yield account, while remaining readily available when you need them.

Disadvantages of Money Market Accounts

Despite their numerous benefits, money market accounts are not without their drawbacks. Understanding these limitations is crucial for determining if an MMA is the right fit for your financial situation and for managing your expectations.

Limited Transaction Capabilities

As previously noted, federal regulations (though currently relaxed in practice by many institutions) historically placed limits on the number of certain transactions allowed from a money market account per month. While many banks have temporarily removed these limits, it’s wise to be aware of the potential for their reintroduction. Even with current flexibility, these accounts are not designed for high-frequency transactions. If you need an account for daily spending and frequent bill payments, a traditional checking account will be more suitable. Exceeding transaction limits can lead to fees or account reclassification, negating the benefits of the MMA.

Variable Interest Rates Can Fluctuate

While the ability to earn a higher interest rate is an advantage, the fact that these rates are variable can also be a disadvantage. If market interest rates fall, the APY on your money market account will likely decrease. This means the earnings on your savings could diminish, potentially making it less attractive compared to other options. This unpredictability can be a concern for those who prefer a guaranteed return over a specific period. Unlike a Certificate of Deposit (CD), where the interest rate is fixed for the term of the CD, an MMA’s rate is subject to market forces.

Typically Lower Returns Than Long-Term Investments

Money market accounts are designed for safety and liquidity, not for aggressive growth. Consequently, the returns they offer are generally lower than those typically generated by long-term investments such as stocks, bonds, or diversified mutual funds. If your financial goals are long-term, such as retirement savings, relying solely on an MMA will likely result in significantly slower wealth accumulation. These accounts are best suited for short-to-medium term savings where capital preservation is a priority.

Minimum Balance Requirements and Fees

Many money market accounts come with minimum balance requirements to earn the stated APY or to avoid monthly maintenance fees. If your balance drops below this threshold, you may earn a significantly lower interest rate or incur fees that eat into your earnings. These fees can negate the advantage of a higher APY, especially for smaller balances. It is essential to carefully review the terms and conditions of any MMA you consider to understand these requirements and potential fees.

Money Market Accounts vs. Other Financial Products

Understanding how money market accounts differ from similar financial products is key to making the most appropriate choice for your savings and investment strategy. While they share some characteristics, their core purposes and risk profiles vary significantly.

Money Market Account vs. Money Market Fund

This is a common point of confusion. A money market account (MMA) is a type of deposit account offered by banks and credit unions. It is insured by the FDIC or NCUA, providing principal protection. The funds deposited are liabilities of the bank.

A money market fund (MMF), on the other hand, is a type of mutual fund. It invests in short-term, low-risk debt instruments like Treasury bills, commercial paper, and certificates of deposit. While MMFs aim to maintain a stable Net Asset Value (NAV) of $1.00 per share, they are not FDIC or NCUA insured and are subject to market risk. Although designed to be very safe, there have been instances where MMFs have “broken the buck” (their NAV fell below $1.00), especially during severe financial crises. MMFs are typically purchased through brokerage accounts.

Money Market Account vs. Traditional Savings Account

The primary difference lies in the interest rate. Money market accounts generally offer a higher APY than traditional savings accounts. Both are federally insured, but MMAs often provide limited check-writing or debit card access, making them more liquid than standard savings accounts, which usually require transfers to a linked checking account for access. Savings accounts typically have no transaction limits and are purely for accumulating funds.

Money Market Account vs. Certificate of Deposit (CD)

Certificates of Deposit (CDs) are also deposit accounts, offering fixed interest rates for a specified term. The key distinction is liquidity. CDs typically impose significant penalties for early withdrawal, making your funds inaccessible without losing earned interest. MMAs offer much greater liquidity, allowing you to access your money with fewer restrictions, albeit usually with a limit on certain types of transactions. In exchange for this liquidity, MMAs typically offer lower interest rates than longer-term CDs.

Money Market Account vs. Checking Account

Checking accounts are designed for daily transactions, offering unlimited check-writing, debit card access, and usually no interest earnings. Money market accounts offer a hybrid approach: some transactional capabilities (limited checks/debit card) but primarily function as a place to save and earn interest. They are not intended for frequent spending. While MMAs offer better returns, checking accounts offer superior transactional flexibility.

How to Maximize Your Money Market Account

To truly benefit from a money market account, it’s essential to approach its use strategically. This involves understanding its role within your broader financial picture and actively managing your account to take advantage of its strengths.

Determine Your Goals and Time Horizon

Before opening an MMA, clearly define what you intend to use it for. Is it for your emergency fund? Saving for a down payment in the next 6-12 months? Holding cash before making a larger investment? The suitability of an MMA depends heavily on your time horizon and your primary objective. For short-term goals (under a year) where preserving capital is paramount, an MMA is an excellent choice. For longer-term goals, you would likely want to explore investments that offer the potential for higher growth, even with increased risk.

Compare APYs and Fees Across Institutions

Don’t settle for the first MMA you find. Interest rates can vary significantly between banks and credit unions, and even online banks often offer more competitive rates than traditional brick-and-mortar institutions. Pay close attention to the APY, but also look for any monthly maintenance fees, minimum balance requirements to avoid fees, and transaction fees. Sometimes, a slightly lower APY with no fees or lower minimum balance requirements might be more beneficial depending on your balance. Online tools and financial comparison websites can be invaluable resources for this research.

Understand and Adhere to Transaction Limits

Even if your current financial institution has temporarily waived transaction limits, be mindful of the underlying principle. MMAs are designed as savings vehicles, not transactional accounts. Regularly exceeding transaction limits can lead to fees or even conversion to a different account type, diminishing the benefits. If you anticipate needing frequent access to funds for spending, ensure you have a separate, suitable checking account.

Consider the Role of Your Emergency Fund

A money market account is an ideal place to house your emergency fund. It provides the necessary safety and accessibility for unexpected expenses, while also earning a better return than a typical savings account. Having three to six months’ worth of living expenses readily available in an insured, interest-bearing account offers significant financial security and peace of mind.

Integrate with Your Broader Financial Plan

A money market account should not operate in isolation. It’s one component of a well-rounded financial strategy. Understand how it fits with your checking accounts, retirement accounts (like 401(k)s or IRAs), investment portfolios, and any short-term savings goals. For example, once your emergency fund is adequately stocked in an MMA, consider channeling additional savings into investment vehicles that offer higher growth potential for long-term objectives. Regular review of your financial accounts and goals will help you ensure your money is working as hard as possible for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.