The market risk premium (MRP) is a fundamental concept in finance, representing the excess return an investor expects to receive for taking on the risk of investing in the stock market as a whole, compared to a risk-free investment. It’s not a static number, but rather a dynamic estimate that fluctuates with market conditions, economic outlook, and investor sentiment. Understanding the MRP is crucial for anyone involved in investing, whether an individual looking to grow their personal wealth or a financial professional managing institutional portfolios. It forms the bedrock of many valuation models and investment decisions, providing a quantitative measure of the compensation investors demand for bearing systemic risk.

The Core Concept: Risk and Return Trade-off

At its heart, the market risk premium is a manifestation of the fundamental principle of finance: the risk-return trade-off. Investors are inherently risk-averse. This means they generally prefer investments with lower risk and lower expected returns over investments with higher risk and higher expected returns, all else being equal. However, to entice investors to venture into riskier assets like equities, which are inherently more volatile than, say, government bonds, these assets must offer the prospect of a higher return. The MRP quantifies this “extra” return.

Defining the Components: Expected Market Return and Risk-Free Rate

To grasp the MRP, we must first understand its two constituent parts: the expected market return and the risk-free rate.

Expected Market Return: The Horizon of Equity Performance

The expected market return is the anticipated average return of the overall stock market over a specific period. This is not a guaranteed outcome but a forward-looking estimate. It’s typically based on historical performance of broad market indices, such as the S&P 500 in the United States or the FTSE 100 in the United Kingdom, combined with economic forecasts and projections about future corporate earnings growth. Analysts and economists use various sophisticated models to arrive at these estimates, considering factors like inflation, interest rate trajectories, and global economic growth. The longer the investment horizon, the more the expected market return tends to converge with historical averages, as short-term volatility tends to smooth out over time.

The Risk-Free Rate: The Baseline of Safety

The risk-free rate represents the theoretical return an investment can yield with zero risk. In practice, this is approximated by the yield on government securities of highly creditworthy nations, such as U.S. Treasury bonds. Because governments are considered the least likely entities to default on their debt obligations, their bonds are seen as the safest investment available. The maturity of the government security used to proxy the risk-free rate is important; typically, longer-term government bonds (e.g., 10-year or 30-year Treasuries) are used, as they better reflect long-term investment horizons. This rate is heavily influenced by central bank monetary policy, inflation expectations, and overall economic stability.

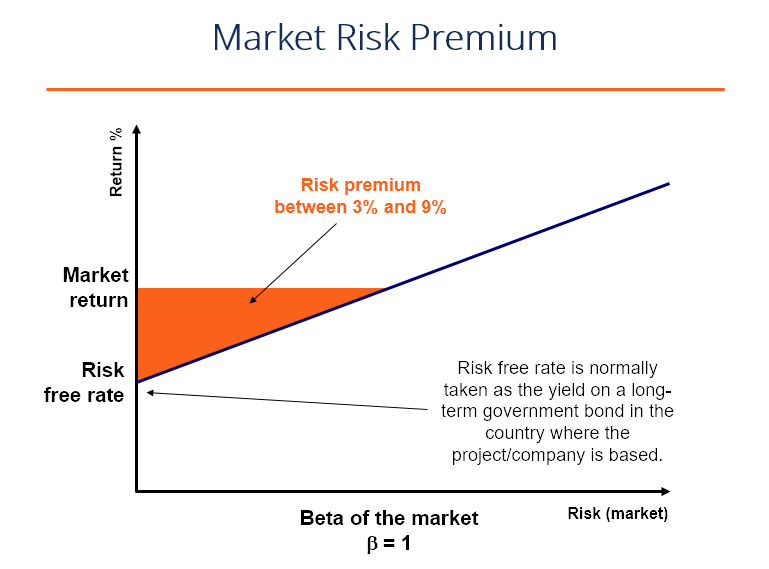

The Calculation: Subtracting Safety from Ambition

The market risk premium is calculated by simply subtracting the risk-free rate from the expected market return.

Market Risk Premium = Expected Market Return – Risk-Free Rate

For example, if the expected return of the stock market is 12% and the current yield on a 10-year U.S. Treasury bond (our risk-free rate proxy) is 4%, then the market risk premium would be 8% (12% – 4% = 8%). This 8% represents the additional return investors anticipate receiving for investing in the stock market instead of the risk-free Treasury bonds.

Factors Influencing the Market Risk Premium

The MRP is not a constant; it’s a fluid figure that responds to a multitude of economic, financial, and psychological factors. Understanding these drivers is key to appreciating its volatility and its implications for investment strategy.

Economic Conditions and Outlook

The overall health and direction of the economy play a paramount role in shaping the MRP.

Inflation and Interest Rates

Periods of high inflation typically lead to rising interest rates, as central banks attempt to curb price increases. Higher interest rates increase the attractiveness of fixed-income investments (like bonds), making them a more competitive alternative to equities. This can put downward pressure on stock valuations and, consequently, on the MRP. Conversely, low inflation and stable or declining interest rates tend to make equities more attractive, potentially boosting the MRP.

Economic Growth and Corporate Earnings

Strong economic growth is generally associated with higher corporate earnings, which fuels investor optimism and demand for stocks. This can lead to a higher expected market return, thus expanding the MRP. Conversely, during economic downturns or periods of uncertainty, investors become more risk-averse, anticipating lower earnings and potential stock price declines. This can reduce the expected market return and, consequently, compress the MRP.

Investor Sentiment and Risk Aversion

Beyond purely economic indicators, the psychological state of investors significantly impacts the MRP.

Market Volatility

Periods of high market volatility, characterized by large and frequent price swings, tend to increase perceived risk. When investors are more fearful, they demand a higher premium for taking on that risk. This means that even if the underlying economic fundamentals remain stable, increased uncertainty and fear can lead to a higher MRP. Conversely, in calm and stable markets, investor confidence rises, and the required risk premium tends to diminish.

Geopolitical Events and Uncertainty

Unforeseen events such as wars, political instability, or pandemics can inject significant uncertainty into the global economic landscape. These events often lead to a flight to safety, where investors sell off riskier assets like stocks and move into perceived safe havens. This increased risk aversion drives up the MRP, as investors demand more compensation for holding equities in such uncertain times.

Changes in Market Structure and Regulation

Evolution within financial markets themselves can also subtly influence the MRP.

Liquidity and Market Efficiency

The ease with which investors can buy and sell securities (liquidity) and the speed at which prices reflect all available information (efficiency) can impact perceived risk. Markets that are more liquid and efficient generally present less idiosyncratic risk to investors, potentially leading to a lower MRP. Conversely, illiquid or less efficient markets may command a higher premium.

Regulatory Changes

New regulations or changes to existing ones can alter the risk-return profile of investments. For instance, regulations that increase the compliance burden or operational risk for companies might lead investors to demand a higher MRP to compensate for these added complexities.

The Significance of the Market Risk Premium in Investing

The market risk premium is not just an academic curiosity; it has profound practical implications for investors and financial professionals alike. It serves as a vital input in a variety of financial analyses and decision-making processes.

Valuation of Assets: The Cornerstone of Discounted Cash Flow

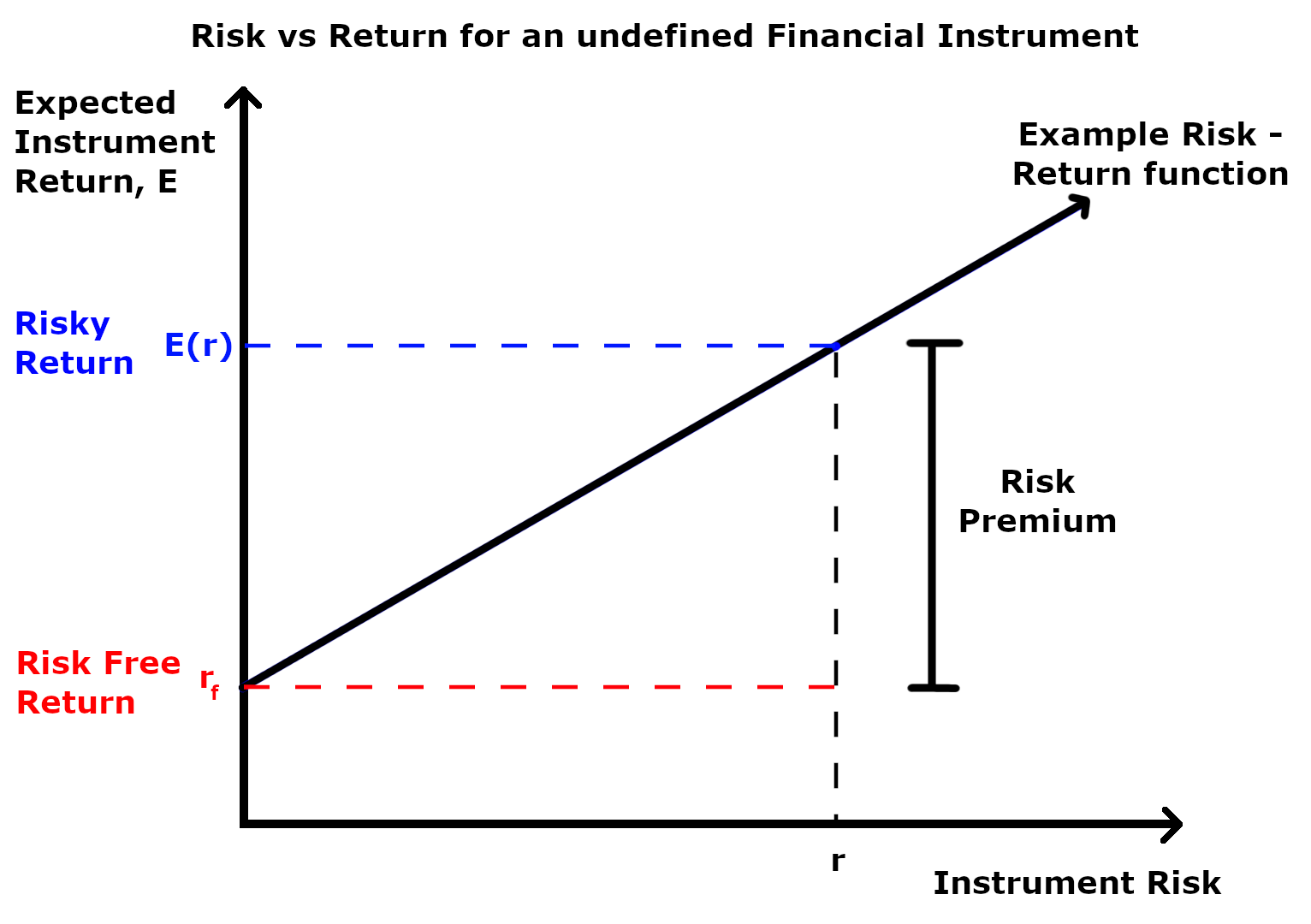

One of the most critical applications of the MRP is in the valuation of individual stocks and entire companies. The Capital Asset Pricing Model (CAPM) is a widely used model that estimates the expected return of an asset based on its systematic risk (beta), the risk-free rate, and the market risk premium.

Expected Return = Risk-Free Rate + Beta * (Market Risk Premium)

The MRP is a key component in calculating the discount rate used in discounted cash flow (DCF) analyses. When a company’s future cash flows are projected, they are discounted back to their present value using a discount rate that reflects the riskiness of those cash flows. A higher MRP leads to a higher discount rate, which in turn results in a lower present value for future cash flows, thus lowering the estimated intrinsic value of the company. Conversely, a lower MRP will increase the discount rate and the estimated value.

Portfolio Construction and Asset Allocation

The MRP is fundamental to strategic asset allocation decisions. Investors use their expectations of the MRP to determine the optimal mix of assets in their portfolios. For instance, if the MRP is perceived to be high, an investor might allocate a larger portion of their portfolio to equities to capture those potentially higher returns. Conversely, if the MRP is low, or if an investor’s risk tolerance is low, they might favor less risky assets like bonds.

Performance Benchmarking and Manager Evaluation

The MRP also plays a role in evaluating the performance of investment managers. When assessing whether a fund manager has outperformed the market, it’s important to consider the level of risk taken. A manager who achieves a return slightly above the market might be considered underperforming if they took on significantly more risk than the market average. The MRP helps frame this risk-adjusted performance analysis.

Setting Investment Goals and Expectations

For individual investors, understanding the MRP helps set realistic return expectations. It provides a baseline understanding of the compensation investors can expect for bearing equity risk over the long term. This can prevent disappointment from unrealistic return targets and guide individuals towards investment strategies that align with their risk tolerance and financial objectives.

Estimating the Market Risk Premium: Challenges and Approaches

Accurately estimating the market risk premium is a challenging endeavor, as it involves forecasting future returns and assessing current risk perceptions. There are several common methods employed, each with its strengths and weaknesses.

Historical Approach: Looking Back to Predict Forward

The most straightforward method involves examining historical data. This approach calculates the average difference between the actual returns of a broad market index (like the S&P 500) and the risk-free rate (like U.S. Treasury yields) over a significant historical period.

Pros:

- Objective: Based on actual, observable data.

- Simple: Easy to calculate and understand.

Cons:

- Assumes the Past Repeats: Historical performance is not necessarily indicative of future results. Market conditions and investor behavior evolve.

- Data Sensitivity: The estimated MRP can vary significantly depending on the historical period chosen. A period of unusually high or low returns can skew the results.

- Limited Forward-Looking Power: Doesn’t directly account for current economic conditions or future expectations.

Forward-Looking (Implied) Approach: Gauging Current Sentiment

This approach attempts to extract the MRP directly from current market prices and expected future earnings or cash flows. Models such as the Dividend Discount Model (DDM) or cash flow-based valuation models can be used to imply the MRP. By observing current stock prices and making assumptions about future dividends or earnings growth, one can back-calculate the discount rate that equates these future expectations with the current price. Subtracting the current risk-free rate from this implied discount rate yields an implied MRP.

Pros:

- Forward-Looking: Directly incorporates current market conditions and investor expectations.

- Reflects Current Sentiment: Captures the market’s current assessment of risk and return.

Cons:

- Relies on Assumptions: Highly sensitive to the assumptions made about future growth rates, dividends, and other variables.

- Model Dependent: Different valuation models will produce different implied MRPs.

- Complex: Requires more sophisticated modeling techniques.

Survey-Based Approach: Asking the Experts

Another method involves surveying financial professionals, economists, and institutional investors about their expectations for future market returns and their perception of risk.

Pros:

- Direct Input: Captures the opinions and expectations of those actively involved in the markets.

- Can Reflect Nuances: May capture qualitative factors not easily quantifiable in quantitative models.

Cons:

- Subjective: Based on opinions, which can be biased or inconsistent.

- Potential for Herd Mentality: Survey respondents may be influenced by the prevailing market sentiment.

- Limited Reach: May not capture the views of all market participants.

In practice, many financial analysts and institutions use a combination of these approaches, comparing the results from different methodologies to arrive at a more robust estimate of the market risk premium. The lack of a single, universally agreed-upon method underscores the inherent difficulty and subjective nature of forecasting future market behavior.

In conclusion, the market risk premium is a vital, albeit complex, metric in the world of finance. It represents the compensation investors demand for bearing the inherent risks of investing in the stock market over and above what they could earn from a risk-free asset. Its estimation is a continuous challenge, influenced by a dynamic interplay of economic conditions, investor psychology, and market structures. A thorough understanding of the MRP empowers investors to make more informed decisions, set realistic expectations, and navigate the often-turbulent waters of the financial markets with greater clarity and confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.