A judicial foreclosure is a legal process initiated by a lender to reclaim a property when a homeowner defaults on their mortgage payments. Unlike some other foreclosure methods, this process always involves the court system, requiring a judge’s order for the property to be sold. It is a time-consuming and often emotionally taxing experience for all parties involved, typically reserved for states where mortgage agreements do not include a “power of sale” clause, or when specific state laws mandate a judicial review. Understanding the intricacies of judicial foreclosure is crucial for homeowners, lenders, and potential buyers navigating the real estate market.

Understanding the Foreclosure Process

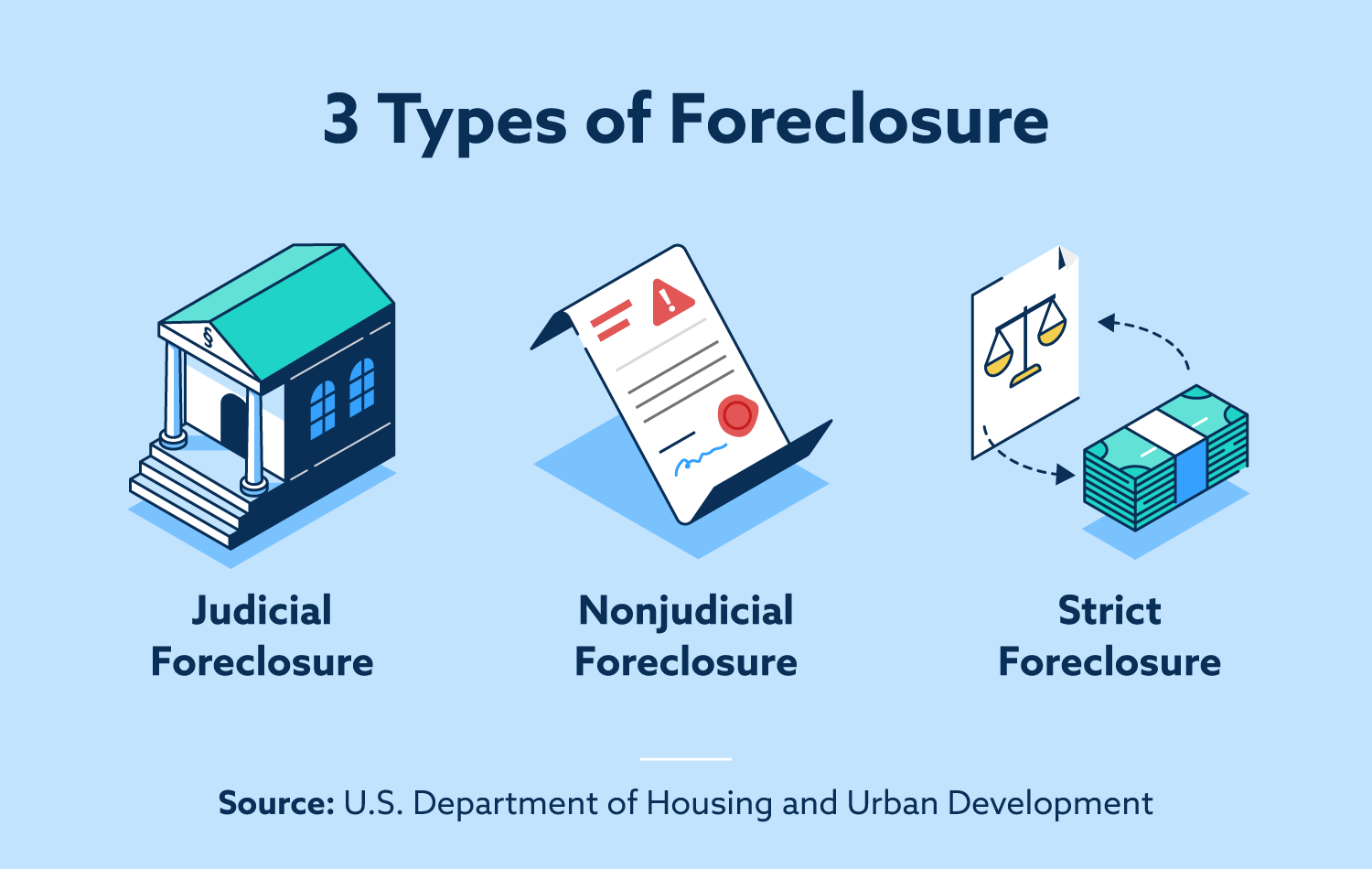

Foreclosure, in its essence, is the legal procedure by which a lender attempts to recover the balance of a loan from a borrower who has defaulted, forcing the sale of the asset used as collateral – typically a home. The type of foreclosure pursued largely depends on the state in which the property is located and the specific terms outlined in the mortgage or deed of trust.

Distinguishing Judicial from Non-Judicial Foreclosure

The primary differentiator between judicial and non-judicial foreclosure lies in the involvement of the court system.

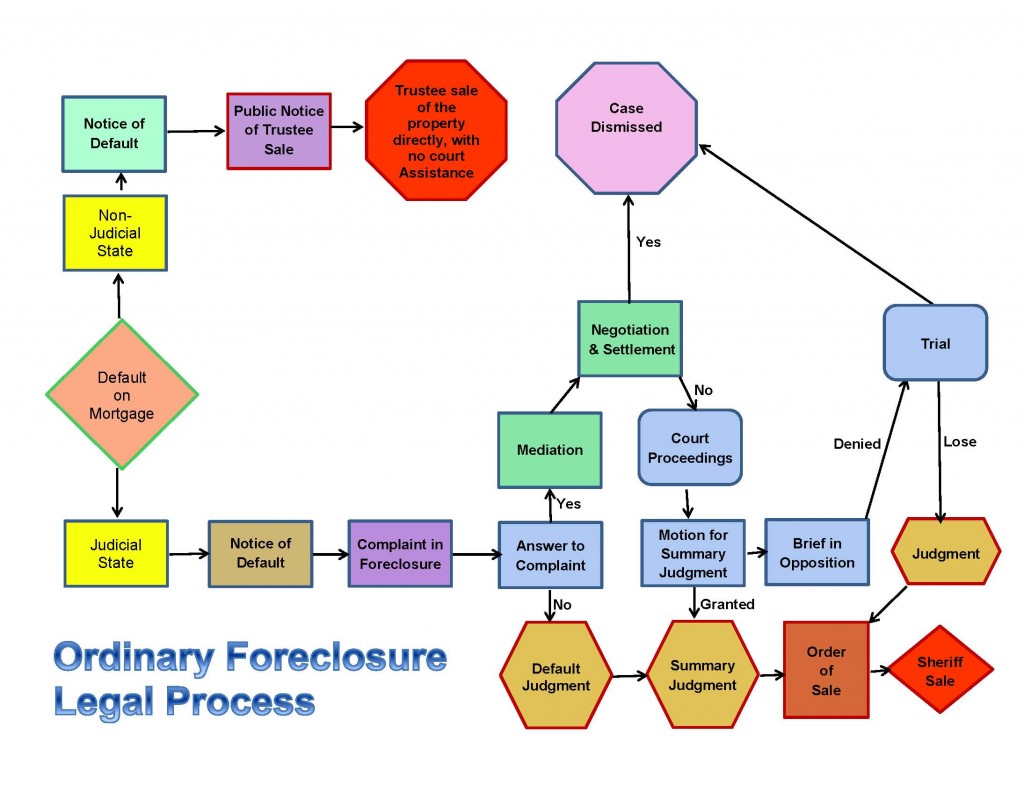

Judicial Foreclosure: This method requires the lender to file a lawsuit in court to obtain a judgment of foreclosure. The process begins with the lender filing a complaint and serving it to the homeowner. The homeowner has an opportunity to respond and present a defense. If the court finds in favor of the lender, it will issue a judgment allowing the property to be sold, typically through a public auction. This court oversight provides a formal legal review of the lender’s right to foreclose, often leading to a longer, more costly process compared to its non-judicial counterpart.

Non-Judicial Foreclosure: In contrast, non-judicial foreclosure occurs without court intervention. This streamlined process is permitted in states where the mortgage document (or deed of trust) includes a “power of sale” clause. This clause grants the lender the authority to sell the property directly upon default, following specific notice requirements dictated by state law. While faster and generally less expensive for the lender, non-judicial foreclosures offer fewer legal protections and opportunities for homeowners to dispute the action in court before the sale.

The choice between these methods profoundly impacts the timeline, costs, and legal avenues available to both lenders and homeowners.

States Where Judicial Foreclosure is Prevalent

The prevalence of judicial foreclosure varies significantly across the United States. Generally, states are classified as either “judicial” or “non-judicial” states, though many have hybrid systems where both methods are possible depending on the mortgage instrument and circumstances.

States commonly identified as “judicial foreclosure states” include Florida, Illinois, New Jersey, New York, Pennsylvania, and Connecticut, among others. In these states, even if a mortgage contains a power of sale clause, state law often mandates that foreclosures proceed through the courts. This legislative preference is typically rooted in a desire to provide greater consumer protection and ensure due process for homeowners facing the loss of their primary residence. Conversely, states like California, Texas, Arizona, and Georgia are predominantly non-judicial, where the power of sale clause is more readily exercised outside the court system. Homeowners in judicial foreclosure states generally have more time to explore alternatives or prepare their legal defense, given the extended timelines inherent in court proceedings.

The Stages of a Judicial Foreclosure

Navigating a judicial foreclosure involves a series of distinct legal and financial steps, each with specific requirements and implications.

Default and Notice

The foreclosure process officially begins when a homeowner defaults on their mortgage, typically by missing several consecutive payments. Most mortgage agreements define default after 90 to 120 days of non-payment. Before initiating a lawsuit, federal regulations generally require the lender to wait at least 120 days from the date of delinquency before filing for foreclosure. During this period, the lender is usually required to send a “breach letter” or “notice of default,” informing the homeowner of their delinquency, the amount owed, and the deadline to cure the default (reinstate the loan) to avoid further action. This initial phase is a critical window for homeowners to engage with their lender to explore alternatives to foreclosure.

Filing the Lawsuit

If the homeowner fails to cure the default, the lender will formally initiate the judicial foreclosure process by filing a lawsuit in the appropriate state court. This lawsuit, often called a “complaint for foreclosure” or “petition for foreclosure,” names the homeowner (and any other parties with an interest in the property, such as junior lienholders) as defendants. The complaint outlines the details of the mortgage, the default, and requests the court to issue a judgment permitting the sale of the property to satisfy the outstanding debt. Concurrently, the homeowner will be “served” with a summons and a copy of the complaint, formally notifying them of the lawsuit and providing a deadline to respond.

Court Proceedings and Judgment

Upon receiving the summons, the homeowner has a limited time (typically 20-30 days, depending on the state) to file an answer with the court. In their answer, the homeowner can admit or deny the allegations in the complaint and raise any legal defenses they may have (e.g., predatory lending practices, improper notice, errors in calculation). If the homeowner fails to respond, the court may issue a “default judgment” in favor of the lender. If an answer is filed, the case proceeds through litigation, which may involve discovery, motions, and potentially a trial. If the court finds that the homeowner is in default and the lender has followed all legal procedures, it will issue a “judgment of foreclosure and order of sale,” legally authorizing the lender to proceed with selling the property.

Public Auction and Sale

Once a judgment of foreclosure is granted, the court typically appoints a referee, commissioner, or sheriff to oversee the sale of the property. The sale is usually conducted as a public auction, often held at the courthouse or a designated public location. Prior to the auction, public notice of the sale must be provided through advertisements in local newspapers or other prescribed methods, allowing potential bidders to prepare. The property is typically sold to the highest bidder, who must then complete the purchase according to the terms set forth by the court. The proceeds from the sale are used to pay off the outstanding mortgage debt, legal fees, and other associated costs.

Deficiency Judgments and Redemption Rights

A critical aspect of judicial foreclosure is the potential for a “deficiency judgment.” If the proceeds from the foreclosure sale are insufficient to cover the entire outstanding mortgage debt, the lender may be able to seek a deficiency judgment against the homeowner for the remaining balance. The availability and amount of deficiency judgments vary by state and can have significant financial implications for the borrower. Some states have “anti-deficiency” laws that protect homeowners from this outcome.

Furthermore, many states provide a “right of redemption” in judicial foreclosures. This allows the homeowner, for a specified period after the foreclosure sale (the “statutory redemption period”), to reclaim their property by paying the full amount owed to the successful bidder or the lender, including the sale price, interest, and costs. The duration of this redemption period varies widely by state, from a few days to over a year, and provides a final opportunity for the homeowner to save their property.

Financial Implications for Homeowners

A judicial foreclosure carries profound financial consequences for homeowners, extending far beyond the loss of the property itself. Understanding these implications is crucial for making informed decisions during financial distress.

Credit Score Impact

The immediate and most significant financial impact of a judicial foreclosure is the severe damage to a homeowner’s credit score. A foreclosure typically remains on a credit report for seven years, drastically lowering the score by hundreds of points. This impact begins even before the final judgment, as missed mortgage payments are reported to credit bureaus. A low credit score makes it extremely challenging to secure new loans, credit cards, or even rental housing at favorable rates for years to come, potentially locking individuals out of mainstream financial products.

Future Borrowing Challenges

Beyond the immediate credit score drop, a foreclosure creates a lasting black mark on a borrower’s financial history. Obtaining another mortgage, an auto loan, or any significant credit will become exceedingly difficult. Lenders will view the individual as a high-risk borrower due to the past default. While it’s not impossible to secure financing after a foreclosure, it often requires waiting several years (typically 3-7 years, depending on the loan type and circumstances), rebuilding credit diligently, and often paying significantly higher interest rates and fees on any approved loans.

Potential for Deficiency Judgments

As mentioned, a deficiency judgment is a court order compelling the borrower to pay the difference between the outstanding mortgage balance and the amount the property sold for at auction, plus associated costs. This means that even after losing their home, homeowners could still be legally obligated to pay a substantial sum to their former lender. The possibility of a deficiency judgment adds another layer of financial burden and uncertainty, and homeowners must be aware of their state’s laws regarding these judgments. In some cases, lenders may pursue collection efforts, including wage garnishments or bank account levies, to satisfy a deficiency judgment.

Alternatives and Prevention Strategies

Facing the prospect of judicial foreclosure is daunting, but homeowners are not without options. Proactive engagement and understanding available alternatives can often mitigate the most severe outcomes.

Loan Modification and Forbearance

One of the first steps for homeowners facing financial hardship is to contact their lender immediately. Lenders often prefer to avoid foreclosure, which can be costly and time-consuming for them. They may offer loan modification programs, which involve permanently changing the terms of the mortgage to make payments more affordable. This could include lowering the interest rate, extending the loan term, or even reducing the principal balance in some cases. Another option is forbearance, a temporary agreement allowing the borrower to reduce or pause mortgage payments for a set period, with the understanding that the missed payments will be repaid later. These solutions require prompt action and transparent communication with the lender.

Short Sale and Deed-in-Lieu of Foreclosure

If saving the home is not feasible, homeowners can explore options that allow them to transition out of the property while potentially minimizing the negative financial impact compared to a full foreclosure. A short sale occurs when the lender agrees to allow the homeowner to sell the property for less than the outstanding mortgage balance. The proceeds from the sale go directly to the lender, who then forgives the remaining debt (or a portion of it). This avoids the public record of a foreclosure and can be less damaging to credit. A deed-in-lieu of foreclosure is another agreement where the homeowner voluntarily transfers the property deed directly to the lender to satisfy the mortgage debt, avoiding the formal court process. Both short sales and deeds-in-lieu require lender approval and can impact credit, though typically less severely than a completed judicial foreclosure.

Seeking Financial and Legal Counsel

Perhaps the most critical prevention strategy is to seek professional guidance early. A qualified housing counselor, certified by the Department of Housing and Urban Development (HUD), can provide free or low-cost advice on navigating financial difficulties, understanding foreclosure alternatives, and negotiating with lenders. Additionally, consulting with a real estate attorney specializing in foreclosure defense is invaluable. An attorney can review the specifics of a homeowner’s situation, identify any potential legal defenses against foreclosure, explain state-specific redemption rights and deficiency judgment laws, and represent the homeowner in court proceedings. Early intervention with expert advice significantly increases the chances of finding a favorable resolution.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.