For most individuals, purchasing a home represents the single largest financial transaction of their lives. A pivotal element of this massive investment is the mortgage interest rate – a seemingly small percentage that can translate into tens or even hundreds of thousands of dollars over the lifetime of a loan. Understanding what constitutes a “good” interest rate isn’t merely about finding the lowest number; it’s about navigating a complex landscape of economic factors, personal financial health, and strategic decision-making. This comprehensive guide will demystify mortgage interest rates, helping you discern what a truly advantageous rate looks like for your unique situation.

Understanding Mortgage Interest Rates: The Basics

Before delving into what makes a rate “good,” it’s crucial to grasp the fundamental concepts underpinning mortgage interest. This foundational knowledge empowers you to approach the homebuying process with confidence and make informed choices.

What is a Mortgage Interest Rate?

At its simplest, a mortgage interest rate is the cost of borrowing money to buy a house, expressed as a percentage of the loan amount. It’s what you pay the lender for the privilege of using their capital. This rate directly influences your monthly mortgage payment and, more significantly, the total amount you’ll repay over the life of the loan. A higher interest rate means a higher monthly payment and a greater overall cost.

Fixed vs. Adjustable-Rate Mortgages (ARMs)

Mortgages primarily come in two forms, each with distinct implications for your interest rate:

- Fixed-Rate Mortgages: With a fixed-rate mortgage, the interest rate remains constant for the entire duration of the loan, typically 15 or 30 years. This offers predictability and stability, as your principal and interest payment will never change. Homeowners appreciate fixed rates during periods of rising interest rates, as their payments remain unaffected. However, if rates fall significantly, their only option to benefit is through refinancing.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an interest rate that changes periodically after an initial fixed period (e.g., 3/1 ARM, 5/1 ARM, 7/1 ARM). For instance, a 5/1 ARM has a fixed rate for the first five years, after which it adjusts annually based on a pre-determined index plus a margin set by the lender. ARMs often start with lower rates than fixed-rate mortgages, making them attractive for borrowers who plan to sell or refinance before the fixed period ends, or those who anticipate their income increasing substantially. The risk, however, lies in the potential for rates to rise, leading to significantly higher monthly payments.

Annual Percentage Rate (APR) vs. Interest Rate

While often used interchangeably, the interest rate and the Annual Percentage Rate (APR) are distinct and crucial for comparison.

- Interest Rate: This is the rate at which interest is calculated on your loan balance. It determines the principal and interest portion of your monthly payment.

- Annual Percentage Rate (APR): The APR is a broader measure of the total cost of borrowing money, encompassing not only the interest rate but also most other fees associated with the loan, such as origination fees, discount points, mortgage insurance, and closing costs. It’s designed to give consumers a more comprehensive “true cost” of the loan over its full term. When comparing loan offers, the APR is often a more accurate metric for gauging the overall expense, though it’s still essential to scrutinize the individual fees included. A lower APR generally indicates a cheaper loan.

Factors Influencing Your Mortgage Interest Rate

The interest rate you are offered on a house isn’t arbitrary; it’s the culmination of various economic forces and your personal financial profile. Understanding these determinants is key to improving your chances of securing a favorable rate.

Economic Indicators (Federal Reserve, Inflation, Bond Market)

Macroeconomic conditions play a significant role in setting the baseline for mortgage rates:

- Federal Reserve Policy: While the Fed doesn’t directly set mortgage rates, its actions, particularly adjustments to the federal funds rate, influence the broader interest rate environment. When the Fed raises rates, borrowing costs across the economy tend to increase, and vice versa.

- Inflation: Lenders are wary of inflation because it erodes the purchasing power of future repayments. To compensate for this risk, they typically charge higher interest rates during periods of high or anticipated inflation.

- The Bond Market: Mortgage rates are closely tied to the yields on U.S. Treasury bonds, particularly the 10-year Treasury note. Mortgage-backed securities (MBS), which are packaged mortgages sold to investors, compete with these bonds for investment. When bond yields rise, mortgage rates generally follow suit.

Your Credit Score and Credit History

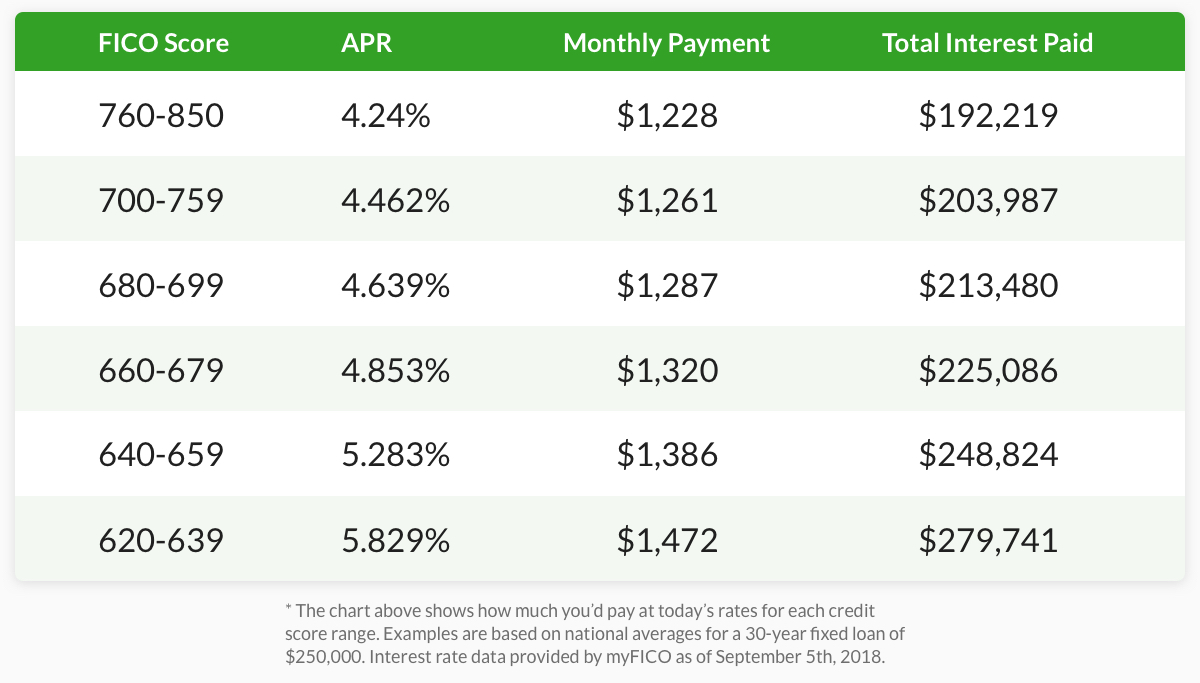

Your creditworthiness is paramount. Lenders use your credit score (e.g., FICO score) as a quick indicator of your likelihood to repay debt. A higher credit score (generally above 740-760) signals lower risk to lenders, making you eligible for their most competitive interest rates. Conversely, a lower credit score may lead to a higher interest rate to compensate the lender for the increased risk. Your credit history, which includes payment punctuality, debt levels, and types of credit, provides a detailed narrative of your financial responsibility.

Your Down Payment Amount

A larger down payment reduces the amount you need to borrow, which can translate into a better interest rate. Lenders view a substantial down payment as a sign of financial stability and reduced risk. If you put down less than 20% of the home’s purchase price, you’ll typically be required to pay Private Mortgage Insurance (PMI), which adds to your monthly housing costs.

Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio is the amount of your loan compared to the home’s appraised value, expressed as a percentage. For example, a $160,000 loan on a $200,000 home has an LTV of 80%. A lower LTV (meaning a larger down payment) generally correlates with a lower interest rate because the lender faces less risk if the property value declines.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is the percentage of your gross monthly income that goes towards debt payments. Lenders typically look at two types: the front-end ratio (housing costs only) and the back-end ratio (all monthly debt payments). A lower DTI ratio indicates that you have more disposable income to cover your mortgage payments, making you a less risky borrower and potentially qualifying you for a better rate.

Loan Term and Type (e.g., 15-year vs. 30-year, FHA, VA, Conventional)

- Loan Term: Shorter loan terms (e.g., 15-year mortgages) typically come with lower interest rates than longer terms (e.g., 30-year mortgages). While the monthly payments are higher for a 15-year loan, you pay significantly less interest over the life of the loan.

- Loan Type: Different mortgage programs cater to various borrower needs:

- Conventional Loans: These are not backed by a government agency and often require good credit and a reasonable down payment.

- FHA Loans: Insured by the Federal Housing Administration, these offer more flexible credit requirements and lower down payments, making homeownership accessible to more people, but they come with mandatory mortgage insurance premiums.

- VA Loans: Guaranteed by the Department of Veterans Affairs, these offer eligible veterans, service members, and their spouses competitive rates, no down payment requirements, and no private mortgage insurance.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are for eligible rural and suburban homebuyers, often requiring no down payment.

Each loan type carries a different risk profile for lenders, influencing the rates offered.

Lender-Specific Factors

Even with identical borrower profiles and economic conditions, different lenders may offer slightly varied rates. This is due to their internal cost structures, risk appetites, profit margins, and current volume of business. This underscores the importance of shopping around.

How to Determine if a Rate is “Good” for You

The concept of a “good” interest rate is highly subjective. What’s excellent for one borrower might be merely acceptable for another, depending on their financial situation, goals, and the prevailing market conditions.

Comparing Current Market Rates (Industry Benchmarks)

One of the most immediate ways to gauge a rate is by comparing it to current industry averages. Financial news outlets, online mortgage calculators, and direct quotes from multiple lenders can provide a snapshot of what rates are generally available. If an offer is significantly higher than the average for someone with your credit profile, it’s worth questioning. Conversely, a rate noticeably below the average is likely a strong contender. However, remember that advertised “best rates” often apply to borrowers with perfect credit and substantial down payments.

Your Personal Financial Goals

A “good” rate aligns with your broader financial strategy:

- Long-Term Stability vs. Short-Term Savings: If you plan to stay in your home for many years, a slightly higher fixed rate that offers payment predictability might be “better” than a lower initial ARM rate that could skyrocket. If you anticipate selling within a few years, a lower ARM rate might be ideal.

- Monthly Payment Affordability: Can you comfortably afford the monthly payment, including principal, interest, taxes, and insurance (PITI)? A low interest rate is only good if the resulting payment doesn’t strain your budget, leaving room for savings, emergencies, and other financial goals.

- Total Cost of Ownership: Consider the total amount you will pay over the life of the loan. A 15-year mortgage will have higher monthly payments but a significantly lower total interest cost compared to a 30-year mortgage with a lower monthly payment. Your definition of “good” might lean towards minimizing long-term cost, even if it means higher short-term payments.

Calculating the Long-Term Cost

Don’t just look at the monthly payment; calculate the total interest paid over the life of the loan. Even a quarter-point difference in the interest rate on a $300,000, 30-year mortgage can add up to tens of thousands of dollars over time. Online mortgage calculators are invaluable tools for this comparison. They allow you to input different rates and terms to visualize the long-term financial impact.

The “Good Rate” Illusion: Beyond the Number

Sometimes, a seemingly “good” rate might come with hidden costs or trade-offs. For example:

- Points: Lenders may offer a lower interest rate if you pay “discount points” upfront – essentially prepaying interest. One point equals 1% of the loan amount. You need to calculate if the savings from the lower rate outweigh the upfront cost of the points, especially if you plan to move or refinance within a few years.

- Fees: Compare all closing costs and fees between lenders. A loan with a slightly higher interest rate but significantly lower fees might have a better overall APR than a loan with a lower interest rate but hefty fees.

- Prepayment Penalties: Some loans, though less common now, might include penalties for paying off your mortgage early. Ensure your loan agreement doesn’t contain such clauses if you anticipate accelerating payments or refinancing.

Strategies to Secure a Favorable Interest Rate

While you can’t control the broader economy, there are concrete steps you can take to position yourself for the best possible interest rate.

Improve Your Credit Score

This is perhaps the most impactful step. A strong credit score tells lenders you are a reliable borrower. To improve your score:

- Pay all bills on time, every time.

- Reduce your credit card balances to keep your credit utilization low (ideally below 30%).

- Avoid opening new credit accounts before applying for a mortgage.

- Review your credit report for errors and dispute any inaccuracies.

Increase Your Down Payment

Aiming for a larger down payment reduces your Loan-to-Value (LTV) ratio, making you a less risky borrower. A 20% down payment is the gold standard, often eliminating the need for Private Mortgage Insurance (PMI) and potentially securing a better rate. Even if you can’t reach 20%, every additional percentage point helps.

Shop Around for Lenders (Get Multiple Quotes)

This cannot be stressed enough. Don’t simply go with the first lender you talk to, or even your current bank. Apply with at least three to five different lenders – including national banks, local credit unions, and online lenders. Each lender has different underwriting guidelines, fee structures, and rate sheets. Getting multiple quotes within a short period (typically 14-45 days, depending on the credit scoring model) will usually count as a single inquiry on your credit report, so it won’t significantly impact your score. Use these quotes to negotiate, as some lenders may be willing to match or beat a competitor’s offer.

Consider Mortgage Points

As mentioned earlier, paying discount points upfront can lower your interest rate. If you have the cash available and plan to stay in the home for a long time (typically more than 5-7 years, but calculate your break-even point), buying down the rate can be a wise investment. Conversely, if you’re short on cash or anticipate moving soon, paying points might not be financially beneficial.

Understand Refinancing Opportunities

A “good” rate isn’t fixed for life, especially if you have an ARM or if market rates drop significantly after you’ve secured a fixed-rate mortgage. Refinancing involves taking out a new loan to pay off your existing mortgage, often to secure a lower interest rate or change loan terms. Keep an eye on market trends, and if rates fall substantially, explore whether refinancing makes financial sense for you. Factor in closing costs associated with refinancing when making this decision.

The Long-Term Impact of Your Interest Rate

The interest rate you secure today will resonate throughout the entire lifecycle of your homeownership, influencing far more than just your initial monthly payment. Understanding these long-term implications is vital for holistic financial planning.

Total Cost of Ownership

The most obvious long-term impact is on the total amount you will pay for your home. Over 15, 20, or 30 years, even a seemingly small difference of a quarter or half percentage point in your interest rate can translate into tens of thousands of dollars in additional interest payments. This extra money could otherwise be invested, saved, or used for other financial goals. A lower interest rate directly reduces the overall cost of your mortgage, leaving you with more wealth in the long run.

Monthly Payment Affordability

Your interest rate is a primary determinant of your monthly principal and interest payment. A lower rate means a lower monthly outlay, enhancing your cash flow and making homeownership more affordable. This increased affordability can reduce financial stress, free up funds for other living expenses, savings, or investments, and provide a greater buffer against unexpected costs. Conversely, a higher rate can stretch your budget thin, leaving little room for discretionary spending or financial setbacks.

Building Home Equity

Home equity is the portion of your home that you truly own, calculated as the market value of your home minus your outstanding mortgage balance. A lower interest rate means a larger portion of your monthly payment goes towards paying down the principal rather than just covering interest charges, especially in the early years of the loan. This accelerates the rate at which you build equity in your home. Building equity faster is advantageous because it increases your net worth, provides a potential source of funds (e.g., via a home equity loan or line of credit), and offers a greater return if you sell the property.

Financial Flexibility and Future Planning

Securing a truly good interest rate enhances your overall financial flexibility. With lower monthly payments or a faster path to equity, you have more options for future planning:

- Earlier Mortgage Payoff: You might be able to make additional principal payments, further accelerating your equity growth and shaving years off your loan term.

- Investment Opportunities: The savings from a lower rate can be redirected towards retirement accounts, college funds, or other investment vehicles, compounding your wealth over time.

- Life Events: A less burdensome mortgage allows greater adaptability during significant life events, such as career changes, starting a family, or unexpected health issues.

- Refinancing Leverage: If you secure a great rate initially, and market conditions shift favorably, you’ll be in an even stronger position if you choose to refinance in the future to further optimize your terms or pull out equity.

In conclusion, “what is a good interest rate on a house” is not a question with a single, universal answer. It’s a dynamic equation influenced by the economy, your personal financial health, and your specific goals. By understanding the underlying mechanics, diligently preparing your finances, and strategically shopping for the best terms, you can confidently secure an interest rate that is not just low, but truly good for your long-term financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.