A General Investment Account (GIA), also known as a non-ISA investment account or a taxable investment account, is a fundamental building block for individuals looking to grow their wealth beyond traditional savings accounts and tax-advantaged wrappers like ISAs (Individual Savings Accounts). In essence, it’s a flexible, unrestricted investment vehicle that allows you to hold a wide range of assets, from stocks and bonds to funds and exchange-traded funds (ETFs), without the annual contribution limits or specific withdrawal rules often associated with tax-efficient accounts. While GIAs don’t offer the same tax benefits as ISAs, their flexibility, accessibility, and unlimited growth potential make them an indispensable tool in a diversified investment strategy for many.

Understanding the nuances of a GIA is crucial for anyone serious about long-term financial planning. It’s the gateway to actively participating in the financial markets, and while it comes with tax obligations, these are often outweighed by the potential for significant returns and the freedom to invest as much as you wish.

The Fundamentals of a General Investment Account

At its core, a General Investment Account is a brokerage account. This means you open it with a financial institution, such as a stockbroker, bank, or an online investment platform. Once funded, you gain access to a marketplace where you can buy and sell various financial instruments. The key differentiator from other types of accounts lies in its tax treatment and its lack of specific investment restrictions beyond those imposed by regulations or the platform itself.

What Can You Invest In?

The breadth of investment options available within a GIA is one of its primary advantages. Unlike some specialized accounts that might restrict investments to specific asset classes, a GIA offers a comprehensive menu. This allows investors to tailor their portfolios precisely to their risk tolerance, financial goals, and market outlook.

Equities (Stocks)

When you invest in equities, you are essentially buying a small piece of ownership in a publicly traded company. This can range from the largest multinational corporations to smaller, emerging businesses. The value of your investment fluctuates with the company’s performance, market sentiment, and broader economic conditions. Investors can profit from equities through two main avenues: capital appreciation (the stock price increasing) and dividends (a portion of the company’s profits distributed to shareholders).

Bonds

Bonds represent a loan made by an investor to a borrower, typically a government or a corporation. In return for the loan, the borrower promises to pay the investor regular interest payments (coupon payments) and to repay the principal amount on a specified maturity date. Bonds are generally considered less volatile than stocks, offering a more predictable income stream and a degree of capital preservation. However, they are not risk-free; bond prices can fall if interest rates rise or if the borrower’s creditworthiness declines.

Funds (Mutual Funds and ETFs)

For investors who prefer a diversified approach without managing individual stocks or bonds, funds are an excellent option.

- Mutual Funds: These pool money from many investors to invest in a diversified portfolio of securities, managed by professional fund managers. They can focus on specific sectors, geographies, or investment styles.

- Exchange-Traded Funds (ETFs): Similar to mutual funds in that they hold a basket of assets, ETFs are traded on stock exchanges like individual stocks. This offers greater flexibility in buying and selling throughout the trading day. Many ETFs are designed to passively track a particular index (e.g., the S&P 500), offering broad market exposure at a typically lower cost than actively managed mutual funds.

Other Investments

Depending on the platform, a GIA may also provide access to other investment types, such as investment trusts, options, futures, and even alternative investments like real estate investment trusts (REITs). The specific offerings will vary by brokerage.

How Does It Work?

Opening a GIA is typically a straightforward process. You’ll need to choose a reputable financial institution, complete an application, and provide personal identification and financial details. Once approved, you can fund the account via bank transfer, cheque, or other methods.

- Placing Trades: Once funded, you can log into your online account to research investments, place buy and sell orders, and monitor your portfolio. Orders are typically executed at the prevailing market price, although specific order types (e.g., limit orders) can provide more control over the price at which a trade is executed.

- Portfolio Management: Your GIA acts as a central hub for all your investments. You can view your holdings, track their performance, and rebalance your portfolio as needed to align with your investment strategy.

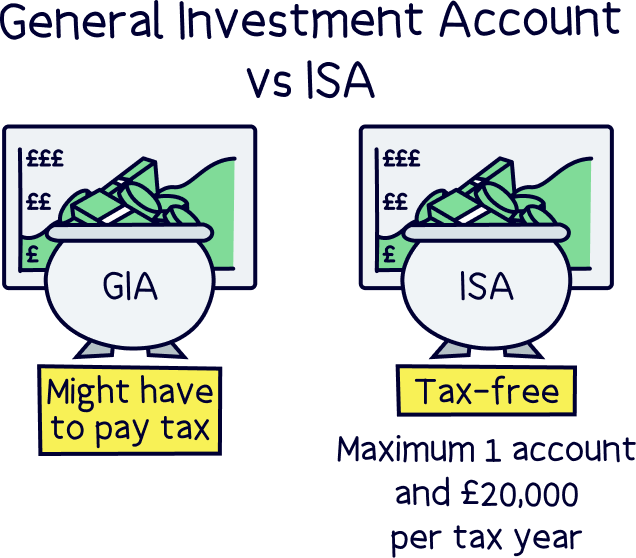

- Withdrawals: A significant advantage of a GIA is its flexibility regarding withdrawals. You can generally withdraw your funds at any time, subject to the settlement period of the assets you are selling. However, it’s important to be aware that any profits made from selling investments in a GIA are subject to Capital Gains Tax.

Tax Implications of a General Investment Account

The primary distinction between a GIA and tax-advantaged accounts like ISAs lies in their tax treatment. While GIAs offer immense flexibility, any profits or income generated are subject to taxation. Understanding these tax obligations is crucial for effective financial planning and for maximizing your net returns.

Capital Gains Tax (CGT)

Capital Gains Tax is levied on the profit you make when you sell an asset that has increased in value since you bought it. In a GIA, this applies to the sale of shares, funds, or any other investments that appreciate.

- The Annual Exempt Amount: Each tax year, individuals have an allowance known as the Annual Exempt Amount. This is the amount of capital gain you can make before you need to pay CGT. Any gains above this threshold are subject to CGT.

- Tax Rates: The rate of CGT you pay depends on your income tax band. For most individuals, the CGT rate on assets other than residential property is typically lower than their income tax rate. This means that even if you exceed the exempt amount, the tax burden might be manageable, especially for lower to mid-range earners.

- Calculating Gains: To calculate your capital gain, you subtract the cost of acquiring the asset (including any transaction fees) from the proceeds of selling it. It’s vital to keep meticulous records of all your transactions to accurately calculate your gains and losses.

- Capital Losses: If you sell an asset for less than you bought it for, you incur a capital loss. These losses can be offset against capital gains made in the same tax year, or they can be carried forward to future tax years to reduce future CGT liabilities. This ability to offset losses is a key advantage of a GIA.

Income Tax

If the investments within your GIA generate income, such as dividends from stocks or interest from bonds, this income is also taxable.

- Dividend Tax: Dividends received from UK companies and certain other qualifying dividends are subject to dividend tax. There is a separate Dividend Allowance, which allows a certain amount of dividend income to be received tax-free. Above this allowance, dividends are taxed at specific rates, which vary depending on your income tax band.

- Interest Tax: Interest earned from bonds or other debt instruments held within a GIA is subject to income tax at your marginal rate. For most individuals, this will be taxed at their standard or higher income tax rate.

- Personal Savings Allowance: If you earn savings interest (which can include interest from bonds), you may be able to benefit from the Personal Savings Allowance. This allows a certain amount of savings interest to be received tax-free each year, depending on your income tax band.

Tax Year Considerations

It’s important to note that tax rules and allowances can change, so it’s always advisable to stay informed about the current tax year’s regulations. The UK tax year runs from April 6th to April 5th. Planning your investment activities, especially around selling assets or realizing gains, can help you optimize your tax position by making full use of your allowances.

Strategic Advantages of a General Investment Account

While the tax implications of a GIA are a significant consideration, its strategic advantages in terms of flexibility, accessibility, and potential for long-term growth are undeniable. For many investors, the ability to invest freely and without the constraints of tax wrappers makes it a cornerstone of their financial strategy.

Unrestricted Investment Potential

Unlike ISAs, which may have restrictions on certain types of investments (though these have become more liberal over time), a GIA typically offers access to a much broader universe of financial products. This allows investors to implement more sophisticated investment strategies and to take advantage of niche opportunities as they arise. Whether it’s investing in overseas markets, specific industry sectors, or alternative asset classes, the GIA provides the freedom to do so.

Unlimited Contribution and Growth Potential

One of the most compelling aspects of a GIA is the absence of annual contribution limits. You can invest as much or as little as you wish, making it ideal for those with substantial capital to invest or for those who are gradually accumulating wealth over time. Furthermore, there is no limit to how much your investments can grow within a GIA. While ISAs have annual caps, your GIA can continue to grow indefinitely. This unlimited growth potential is particularly attractive for long-term wealth accumulation, retirement planning, and estate planning.

Flexibility for Various Financial Goals

The GIA’s flexibility extends to its suitability for a wide array of financial goals.

- Short to Medium-Term Goals: While it’s generally advisable to avoid investing money you might need in the very short term due to market volatility, a GIA can be used for medium-term goals (e.g., saving for a house deposit in 5-10 years) where you can tolerate some risk for potentially higher returns than a standard savings account.

- Long-Term Goals: For long-term objectives like retirement, funding higher education for children, or simply building substantial wealth over decades, the GIA’s growth potential, coupled with its flexibility, makes it an excellent choice.

- Supplementing Tax-Advantaged Accounts: Many investors use GIAs to supplement their ISA allowances. Once you’ve maximized your ISA contributions, a GIA becomes the natural next step for further investing. It also serves as a vehicle to diversify tax liabilities, as not all your investment growth needs to be concentrated in tax-wrapped wrappers.

Rebalancing and Portfolio Diversification

The GIA is the ideal platform for active portfolio management. You can easily rebalance your holdings to maintain your desired asset allocation. If stocks have performed exceptionally well, you might sell some to buy more bonds to bring your portfolio back into alignment with your risk profile. This is crucial for managing risk and ensuring your portfolio remains aligned with your long-term objectives. The ability to hold a diverse range of assets within one account simplifies this process.

Who Should Consider a General Investment Account?

The General Investment Account is not a one-size-fits-all solution, but its characteristics make it a valuable tool for a broad spectrum of investors. The decision to open and utilize a GIA typically hinges on an individual’s financial situation, investment experience, and long-term aspirations.

Investors Who Have Maximized ISA Allowances

For individuals who consistently contribute the maximum amount to their ISAs each tax year, a GIA becomes the logical next step for further investment. When your tax-efficient wrappers are full, and you still have funds available for investment, the GIA offers an unrestricted avenue to continue growing your wealth. It allows you to leverage market opportunities beyond the limitations imposed by ISA annual allowances.

Individuals Seeking Greater Investment Flexibility

The inherent flexibility of a GIA is a significant draw. Unlike some pension schemes or other structured investment products that might have lock-in periods or specific withdrawal conditions, GIAs offer considerable freedom. Investors who value the ability to access their funds relatively easily, or who want the liberty to invest in a very wide range of assets without constraint, will find a GIA highly appealing. This could include those who anticipate needing access to their capital for significant life events in the medium to long term, or those who simply prefer not to be bound by the rules of tax-advantaged accounts.

Those with Substantial Capital to Invest

For individuals with significant sums of money to invest, a GIA is often essential. The annual limits on ISAs, while generous, can be quickly reached by those with substantial wealth. A GIA provides an unlimited capacity to invest, allowing for the deployment of larger amounts of capital into the markets with the aim of generating significant returns over time. This is particularly relevant for individuals with inherited wealth, successful business owners, or those with high earning capacities who are diligent savers.

Investors Looking for Diversification of Tax Liabilities

While GIAs are taxable, they offer a way to diversify your tax exposure. By holding investments across both taxable (GIA) and tax-efficient (ISA) accounts, you can strategically manage your overall tax burden. For instance, you might hold assets that are expected to generate higher income or capital gains in your ISA to benefit from tax-free growth, while using the GIA for assets that might produce less taxable income or for more speculative investments. This diversification of tax treatment can be a powerful tool in optimizing your net investment returns.

Novice Investors Starting Out

For those new to investing, a GIA can serve as an excellent learning platform. Many online investment platforms offer user-friendly interfaces for opening and managing GIAs, often with educational resources to help beginners understand the market. Starting with smaller amounts in a GIA allows new investors to gain practical experience in buying and selling investments, understanding market fluctuations, and managing a portfolio, all while becoming familiar with the tax implications of investing. As they gain confidence and knowledge, they can then strategically allocate funds to ISAs or other investment vehicles.

In conclusion, the General Investment Account is a foundational investment tool that offers unparalleled flexibility and growth potential. While it requires careful consideration of tax implications, its ability to accommodate unlimited contributions and a vast array of investment options makes it an indispensable component of a comprehensive financial strategy for a wide range of individuals looking to build and preserve wealth over the long term.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.