In the realm of personal finance and wealth management, the transfer of assets between generations is one of the most critical, yet often misunderstood, processes. While most people are familiar with the term “heir,” the legal and financial world utilizes more specific terminology to describe how wealth changes hands. One such term is “devisee.”

Understanding what a devisee is—and the financial responsibilities that come with the title—is essential for anyone involved in estate planning, whether you are drafting a will or expecting to receive an inheritance. At its core, being a devisee involves the receipt of real property through a last will and testament. However, the financial implications extend far beyond simply receiving a deed.

Defining the Devisee: The Legal and Financial Context

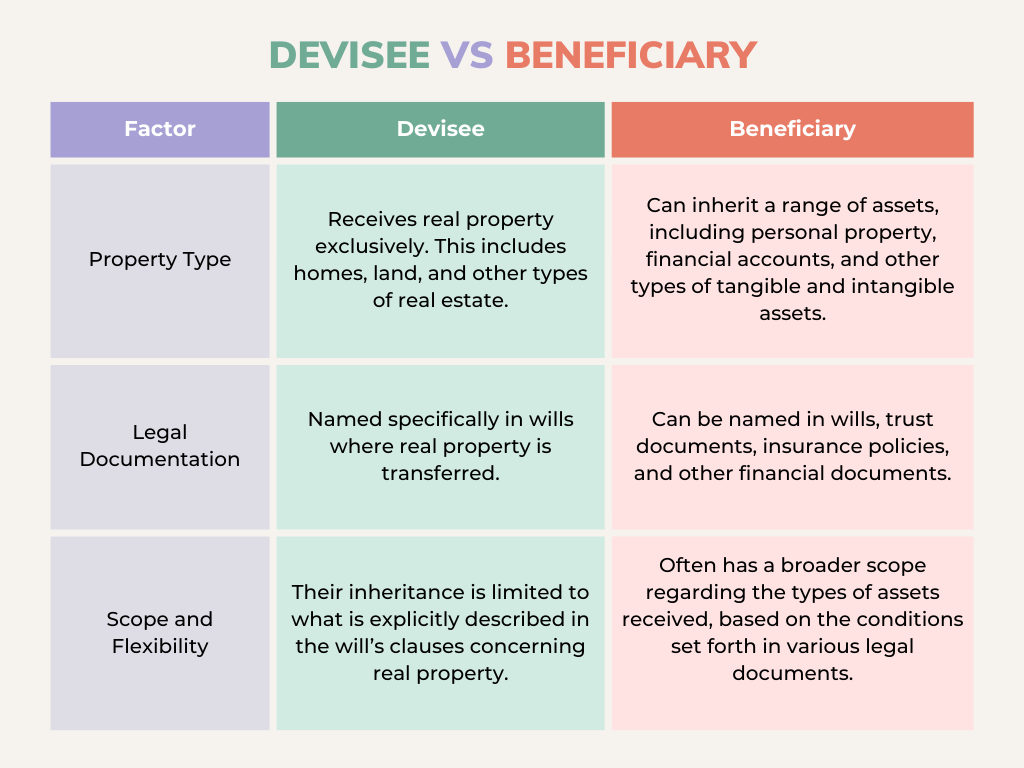

To understand the role of a devisee, one must first look at the structure of a will. When an individual (the testator) passes away, their assets are distributed according to their written instructions. These assets are generally categorized into two groups: personal property (cash, jewelry, stocks) and real property (land, homes, commercial buildings). A devisee is specifically a person or entity designated to receive real property.

Devisee vs. Heir: Key Differences

The terms “devisee” and “heir” are frequently used interchangeably in casual conversation, but in financial and legal contexts, they represent very different statuses. An heir is someone who is legally entitled to inherit property under the laws of intestacy when a person dies without a will. This is usually a spouse, child, or close relative.

In contrast, a devisee is created solely by the existence of a valid will. You do not need to be related to the deceased to be a devisee. A testator can name a friend, a business partner, or even a charitable organization as a devisee of their real estate. From a financial planning perspective, being a devisee is a matter of designated intent rather than biological right.

Devise vs. Bequest: Distinguishing Real Property from Personal Property

Another crucial distinction in estate finance is the difference between a “devise” and a “bequest.”

- A Devise refers to a gift of real estate (land or buildings).

- A Bequest refers to a gift of personal property (money, cars, heirlooms).

If you are named in a will to receive a lakefront cottage, you are a devisee receiving a devise. If you are named to receive a $50,000 savings account, you are technically a legatee receiving a bequest. While the distinction may seem pedantic, it becomes vital during the probate process, as different rules may apply to how these assets are taxed, appraised, and transferred.

The Financial Significance of Being a Devisee

Receiving real estate through a will is a significant financial event that can drastically alter an individual’s net worth. However, it also introduces a suite of financial considerations, ranging from immediate valuation concerns to long-term tax liabilities.

Transfer of Title and Valuation

The moment a person becomes a devisee, the financial clock starts ticking on the property’s valuation. For tax purposes, the property is typically valued at its “fair market value” as of the date of the testator’s death. This is known as a “stepped-up basis.”

In the world of personal finance, the stepped-up basis is one of the most powerful wealth-building tools available. If the deceased bought a home for $100,000 forty years ago and it is worth $1,000,000 at the time of their death, the devisee’s tax basis becomes $1,000,000. If the devisee sells the property immediately, they owe zero capital gains tax. Understanding this valuation is critical for a devisee when deciding whether to hold the asset as an investment or liquidate it for cash.

Tax Implications for the Devisee

While the federal estate tax only applies to very high-net-worth estates, many states impose their own inheritance or estate taxes. As a devisee, the financial burden of these taxes depends on the language of the will and state law. In some cases, the estate pays the taxes before distribution; in others, the devisee may be responsible for a portion of the inheritance tax based on the value of the real estate received.

Beyond inheritance taxes, the devisee must immediately account for ongoing carrying costs. This includes property taxes, homeowners’ association (HOA) fees, and insurance premiums. A devisee who is unprepared for these recurring expenses may find that their “windfall” quickly becomes a financial drain.

Navigating the Probate Process for Real Estate Assets

The transition from being a “named devisee” to a “property owner” occurs through probate—the court-supervised process of authenticating a will and distributing assets. For the devisee, this period is characterized by legal oversight and financial transparency.

The Role of the Executor in Property Distribution

The executor (or personal representative) of the estate acts as the fiduciary bridge between the deceased’s wishes and the devisee’s acquisition. The executor is responsible for ensuring the property is maintained during probate, paying any outstanding utilities, and eventually executing a “Deed of Distribution” to formally transfer the title to the devisee.

For the devisee, maintaining a professional relationship with the executor is paramount. Financial delays often occur during probate if there are disputes or if the estate lacks the liquidity to pay off debts. In some instances, if the estate has more debt than liquid assets, the executor may be forced to sell the devised property to satisfy creditors, leaving the devisee with nothing or only the remaining proceeds.

Potential Liens and Encumbrances on Devised Property

A devisee does not always receive a “clean” asset. Real estate often comes with financial “attachments” such as mortgages, equity lines of credit, or tax liens. In many jurisdictions, the law assumes that the property passes “subject to” the mortgage unless the will specifically instructs the executor to pay off the debt using other estate funds.

This means a devisee must conduct due diligence. Receiving a $500,000 home with a $450,000 mortgage provides a much different financial outlook than receiving the same home debt-free. A devisee must assess whether they can qualify to refinance the debt or if they have the liquidity to pay it off to protect their new equity.

Incorporating Devises into Your Personal Finance Strategy

Whether you are the one planning your estate or the one receiving an inheritance, the “devise” is a strategic tool in wealth preservation. It allows for the surgical distribution of wealth, ensuring that specific real estate assets remain within certain circles or serve specific financial purposes.

Specific vs. General Devises

When drafting a will, a person can make a “specific devise” or a “residuary devise.”

- Specific Devise: “I give my primary residence at 123 Maple St. to my daughter.” This gives the devisee priority. If the estate needs to sell assets to pay debts, specific devises are usually the last to be touched.

- Residuary Devise: “I give the remainder of my real estate to my son.” This covers any property not specifically mentioned.

From a financial planning perspective, being a specific devisee is a more secure position. If you are a residuary devisee, your inheritance is more susceptible to being diminished by the estate’s debts and expenses.

Planning for the Future: Protecting Your Real Estate Assets

For those looking to leave a legacy, understanding the role of the devisee helps in crafting a more robust financial plan. Simply naming a devisee is often not enough. To ensure a smooth transfer of wealth, many financial advisors recommend:

- Liquidity Planning: Ensuring the estate has enough cash to pay taxes and debts so the real estate doesn’t have to be sold.

- Title Audits: Regularly checking that property titles are clear to prevent legal headaches for the devisee during probate.

- Communication: Informing the intended devisee of the gift so they can incorporate the asset into their own long-term financial plan.

Conclusion: The Devisee as a Steward of Wealth

Being a devisee is more than just a legal designation; it is a significant financial responsibility. It represents the culmination of one person’s wealth-building efforts being passed to the next generation. By understanding the nuances of real property transfer, the benefits of the stepped-up basis, and the potential pitfalls of probate and encumbrances, a devisee can transform an inheritance into a lasting financial foundation.

In the complex landscape of personal finance, knowledge is the most valuable asset. Whether you are currently a devisee or are planning to name one in your own estate, understanding the mechanics of this role ensures that wealth is not just transferred, but preserved and grown for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.