In the intricate world of business finance, where every transaction carries weight and every record contributes to a company’s financial narrative, the humble business check remains a cornerstone. Far more than just a piece of paper, a business check is a formal financial instrument that facilitates payments, maintains meticulous records, and underpins the professional integrity of countless enterprises, from fledgling startups to multinational corporations. While digital payment methods have surged in popularity, understanding the fundamental nature, strategic advantages, and proper management of business checks is crucial for any finance professional, business owner, or entrepreneur navigating the complexities of modern commerce. This article delves deep into what a business check entails, its significance, and how it continues to play a vital role in robust financial management.

Understanding the Fundamentals of a Business Check

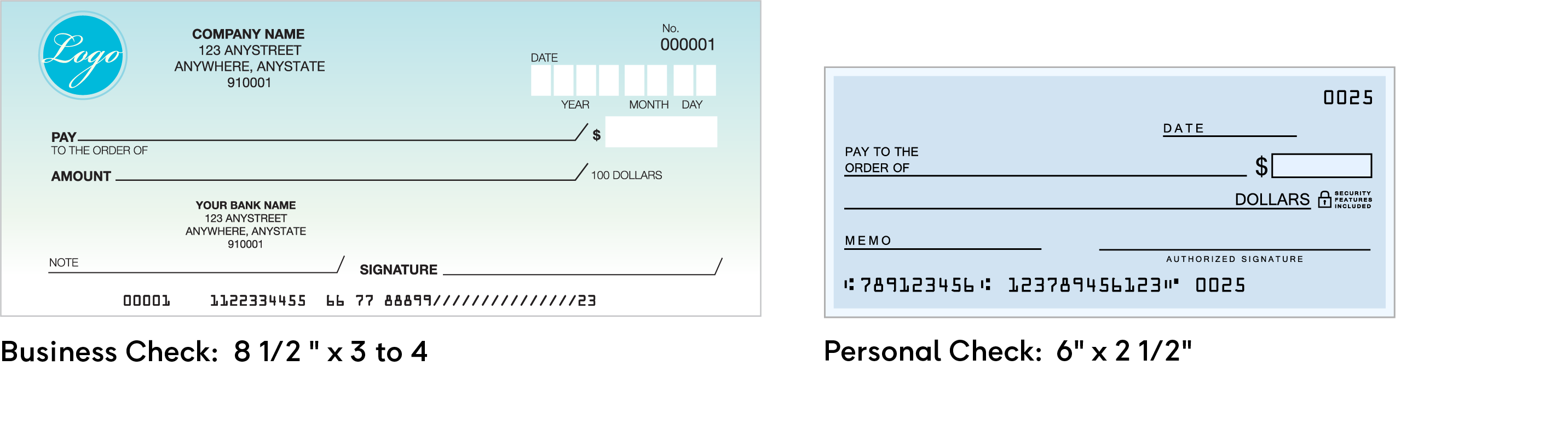

At its core, a business check is a payment order drawn by a business on its bank account, instructing the bank to pay a specific sum of money to a designated payee. It serves as a tangible representation of a financial transaction, offering a level of detail and control often unparalleled by other payment methods. Grasping its basic components and purpose is the first step toward leveraging this powerful financial tool effectively.

Key Elements and Anatomy

Every business check is replete with critical information that ensures its validity and traceability. These elements are standardized and crucial for processing and record-keeping:

- Payer’s Information: Located typically in the upper left corner, this includes the business’s name, address, and sometimes its logo. This clearly identifies who is issuing the payment.

- Date: The date the check is written, which dictates when the check can be cashed or deposited.

- Payee’s Name: The specific individual or entity to whom the payment is being made, written clearly after “Pay to the Order of.”

- Monetary Amount (Numeric): The exact amount of the payment, written in numerical form in a designated box, ensuring clarity and preventing alteration.

- Monetary Amount (Written): The same amount, spelled out in words, to prevent discrepancies and reduce the risk of fraud. In case of a conflict between the numeric and written amounts, the written amount typically takes precedence.

- Bank Name and Address: Identifies the financial institution holding the business’s account.

- Memo Line: An optional but highly useful section for noting the purpose of the payment (e.g., “Invoice #123,” “Rent – April,” “Payroll”). This aids in reconciliation and record-keeping.

- Signature Line: The authorized signature of the business owner or a designated representative, validating the payment instruction. Without a valid signature, the check is null and void.

- Account and Routing Numbers: Found at the bottom of the check in MICR (Magnetic Ink Character Recognition) ink. The routing number identifies the bank, and the account number identifies the specific business account from which funds will be drawn. These are essential for electronic processing.

- Check Number: A unique sequential number, usually in the upper right corner and sometimes in the MICR line, used for tracking and reconciliation.

The Legal and Financial Purpose

Beyond being a simple payment method, a business check holds significant legal and financial weight. Legally, a check is considered a negotiable instrument, meaning it can be transferred from one party to another. When a business issues a check, it legally obligates its bank to pay the specified amount from its account, provided sufficient funds are available. Financially, checks serve multiple purposes: they facilitate payment for goods and services, employee salaries, taxes, and other operational expenses. They also act as a robust paper trail, providing verifiable proof of payment that is invaluable for audits, dispute resolution, and comprehensive financial reporting. This inherent traceability makes them a preferred choice for transactions requiring formal documentation.

Differentiating from Personal Checks

While the fundamental mechanics are similar, business checks are distinctly different from personal checks, tailored to meet the specific demands of commercial operations. Personal checks are drawn from an individual’s personal checking account, typically used for household expenses and personal transactions. Business checks, conversely, are drawn from a dedicated business bank account. This separation is crucial for:

- Legal Compliance: Many business structures (e.g., corporations, LLCs) require maintaining separate finances to preserve limited liability and ensure legal compliance.

- Taxation: Commingling personal and business funds can complicate tax preparation and increase the risk of IRS scrutiny. Business checks simplify expense tracking and income reporting.

- Professionalism: Paying vendors, employees, or contractors with a professionally branded business check projects an image of legitimacy and reliability, reinforcing trust and professionalism.

- Financial Tracking: A dedicated business checking account and the use of business checks make it significantly easier to categorize expenses, manage cash flow, and generate accurate financial statements.

The Strategic Advantages of Utilizing Business Checks

In an era increasingly dominated by digital transactions, the continued relevance of business checks is often questioned. However, for many businesses, they offer distinct strategic advantages that contribute to robust financial health and operational efficiency. These benefits extend beyond mere payment processing, touching upon areas of financial control, security, and professional presentation.

Enhanced Financial Tracking and Record-Keeping

One of the primary benefits of business checks is the unparalleled level of detail they provide for financial tracking. Each check inherently creates a physical and digital record of a transaction. The memo line allows for specific categorization, linking payments directly to invoices, projects, or expense categories. This meticulous detail is invaluable for:

- Auditing: Checks provide a clear, undeniable paper trail for auditors, simplifying the verification of expenses and revenues.

- Budgeting: By tracking spending through checks, businesses can gain clearer insights into where their money is going, facilitating more accurate budget forecasting.

- Tax Preparation: Categorized check payments simplify the process of identifying deductible expenses and fulfilling tax obligations, reducing the time and complexity associated with tax season.

- Dispute Resolution: In the event of a payment dispute, a cancelled check or a copy thereof serves as concrete proof of payment, detailing the amount, date, and payee.

Professionalism and Trust in Transactions

For many businesses, particularly those dealing with vendors, contractors, or clients who prefer traditional payment methods, issuing a business check conveys a strong sense of professionalism and legitimacy. A custom-designed check, often featuring the company logo and branding, reinforces corporate identity and signals that the business operates with integrity and organization. This professional presentation can:

- Build Vendor Relationships: Timely and formally presented payments can strengthen relationships with suppliers, potentially leading to better terms or discounts.

- Instill Client Confidence: For service-based businesses, a professional payment method for refunds or disbursements can enhance client trust and satisfaction.

- Legitimize Small Businesses: For new or small businesses, using business checks helps establish a credible image, distinguishing them from individuals and signaling their commitment to formal business practices.

Flexibility and Control Over Payments

While digital payments offer speed, business checks offer a unique blend of flexibility and control that can be strategically advantageous. Checks allow for:

- Scheduled Payments: Businesses can write checks in advance and post-date them, ensuring payments are processed only when due, optimizing cash flow management.

- Payment Hold: Unlike immediate electronic transfers, checks provide a small window where payment can potentially be stopped or voided if an error is discovered or circumstances change before the check is cashed.

- Remote Payments: Checks can be easily mailed to payees who may not have access to or prefer not to use digital payment platforms, reaching a broader range of recipients.

- Accountability: The requirement for a physical signature and the detailed information on a check add layers of accountability for both the payer and the payee.

Security Features and Fraud Prevention

Despite common misconceptions, modern business checks incorporate several security features designed to prevent fraud and protect business funds. These measures include:

- Microprinting: Tiny lines of text, often found on borders or signature lines, that are legible only under magnification and difficult to counterfeit.

- Watermarks: Invisible to the naked eye, these become visible when held up to light, proving the authenticity of the check paper.

- Chemical Void Protection: Special paper that reacts to chemical alterations (like ink eradication), revealing a “VOID” message.

- Toner Adhesion: Features that prevent the easy removal of toner from laser-printed checks.

- Security Inks: Inks that prevent alteration or reproduction.

- Sequential Numbering: Makes it easy to identify missing checks or track their usage, deterring internal fraud.

While no payment method is entirely immune to fraud, these built-in security features, combined with sound internal controls, significantly enhance the safety of business check transactions.

Types of Business Checks and Their Practical Applications

The term “business check” can encompass various forms, each designed to meet specific financial needs within a commercial context. Understanding these different types allows businesses to select the most appropriate instrument for diverse payment scenarios, optimizing efficiency and maintaining financial rigor.

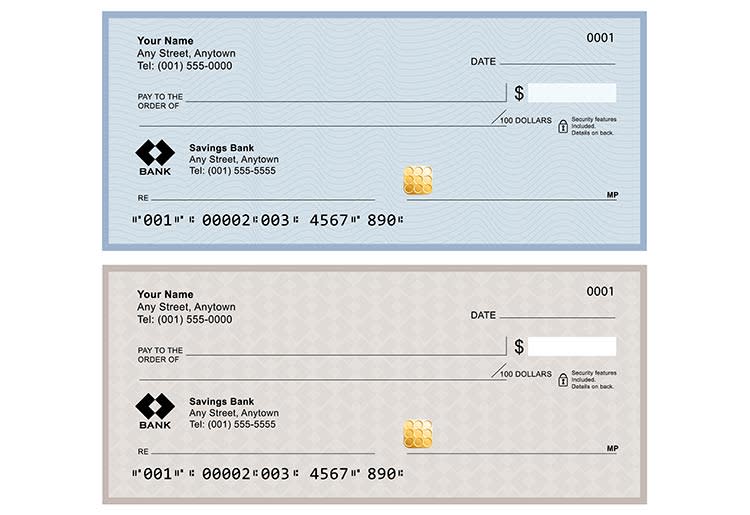

Standard Business Checks

These are the most common type of business check, resembling enlarged versions of personal checks, often supplied in a three-per-page format. They are widely used for general expenses, vendor payments, and operational disbursements. Their design often allows for ample space for the business’s branding and detailed memo entries.

- Applications: Paying suppliers, utility bills, rent, consultants, one-off expenses, and any other general disbursement from the business account.

- Advantages: Versatile, easy to use, widely accepted, and provides a clear paper trail for reconciliation.

Payroll Checks

Specifically designed for paying employees, payroll checks often come with an attached stub that details earnings, deductions (taxes, benefits, etc.), and net pay. This stub is crucial for employees to understand their compensation and for businesses to comply with payroll regulations.

- Applications: Distributing wages and salaries to employees.

- Advantages: Provides detailed documentation for both employer and employee, simplifies tax reporting, and serves as an official record of income. While direct deposit is prevalent, payroll checks are still common for new employees, those without bank accounts, or in specific industries.

Voucher Checks

Voucher checks are a highly detailed variant, typically having one or two perforated stubs (vouchers) attached to the main check. These stubs are used to record extensive transaction details, such as multiple invoice numbers, discount amounts, or a breakdown of services. One stub is often kept by the payee, and the other by the payer for their records.

- Applications: Payments to vendors with multiple invoices, complex expense reimbursements, or situations requiring extensive documentation for accounting purposes.

- Advantages: Eliminates the need for separate remittance advices, streamlines reconciliation for both parties, and provides a comprehensive audit trail.

Money Orders and Certified Checks

While not strictly “business checks” in the sense of being drawn directly from a business’s checking account, money orders and certified checks are important related financial tools that businesses might utilize for specific payment guarantees.

- Money Orders: Purchased from banks, post offices, or certain retail outlets, a money order is a prepaid payment instrument. It’s often used when a business needs to pay an individual or entity that doesn’t accept personal checks, or when cash is not advisable, but a guarantee of funds is needed up to a certain amount.

- Certified Checks: Issued by a bank, a certified check guarantees that the funds are available and have been set aside from the payer’s account. The bank validates the signature and “certifies” the check, making it a highly secure payment method. Businesses often use these for large transactions, real estate dealings, or when a high degree of payment assurance is required.

- Cashier’s Checks: Similar to certified checks, a cashier’s check is drawn directly on the bank’s own funds, not the customer’s account. This makes it an even more secure option as the bank itself is the guarantor. Businesses might use cashier’s checks for significant purchases where absolute payment certainty is paramount.

Each of these types serves a distinct function, enabling businesses to manage their financial obligations with precision, professionalism, and appropriate levels of security.

Best Practices for Managing and Securing Business Check Transactions

Effective management of business checks extends beyond simply writing and sending them. It involves establishing robust internal controls, diligent record-keeping, and proactive security measures to safeguard funds and maintain accurate financial records. Adhering to best practices is paramount for mitigating risks and ensuring smooth financial operations.

Maintaining Accurate Check Registers

A check register (or check ledger) is an essential tool for tracking every check issued and every transaction affecting the business checking account. Whether manual or digital, an accurate register should include:

- Check Number: For easy reference.

- Date: When the check was written.

- Payee: Who received the payment.

- Amount: The exact sum paid.

Purpose/Memo: A brief description of the expense or reason for payment. - Balance: The running balance of the checking account after each transaction.

Regularly updating the check register ensures that a business always knows its cash position, prevents overdrafts, and simplifies reconciliation with bank statements.

Safeguarding Against Fraud

Despite advanced security features on checks, businesses must implement internal controls to minimize the risk of check fraud, both internal and external.

- Secure Storage: Blank checks should be stored in a locked, secure location, accessible only to authorized personnel.

- Segregation of Duties: The person responsible for writing checks should ideally not be the same person who authorizes payments, reconciles bank statements, or handles deposits. This creates a system of checks and balances.

- Controlled Access: Limit the number of employees who have access to check stock, signature stamps, and accounting software that generates checks.

- Positive Pay: Consider enrolling in positive pay services offered by banks. This fraud prevention service compares checks presented for payment against a list of checks the business has authorized, flagging any discrepancies for review.

- Ink and Handwriting: Always use indelible ink when writing checks. Avoid leaving large spaces where additional numbers or words could be added.

- Regular Audits: Periodically audit check-writing and reconciliation processes to identify and rectify any vulnerabilities.

Reconciliation and Audit Preparation

Monthly bank reconciliation is a critical financial process that involves comparing the business’s internal financial records (like the check register) with the bank’s statement. This process helps to:

- Identify Discrepancies: Catch errors made by the bank or the business, such as incorrect amounts, missing transactions, or duplicate entries.

- Detect Fraud: Uncover unauthorized transactions or forged checks that may have cleared the account.

- Track Outstanding Checks: Identify checks that have been issued but not yet cashed by the payee, crucial for accurate cash flow forecasting.

- Prepare for Audits: Ensures that all financial records are consistent and verifiable, streamlining annual audits and tax preparations.

Prompt and thorough reconciliation is a cornerstone of sound financial management, providing assurance that all check transactions are accurately recorded and accounted for.

Integrating with Accounting Software

Modern accounting software (e.g., QuickBooks, Xero, Sage) can significantly streamline the process of managing business checks. Integration offers several advantages:

- Automated Check Printing: Software can automatically populate check details and print checks, saving time and reducing manual errors.

- Digital Register: The software maintains a digital check register, automatically updating account balances with each printed check.

- Seamless Reconciliation: Many platforms can directly import bank statements, automating much of the reconciliation process and flagging potential issues.

- Expense Categorization: Checks can be automatically categorized within the software, simplifying budgeting and tax reporting.

- Reporting: Generate comprehensive reports on expenses, vendor payments, and cash flow directly from the integrated data.

Leveraging technology in this way enhances efficiency, accuracy, and control over business check transactions, allowing finance teams to focus on strategic analysis rather than manual data entry.

The Evolving Landscape: Business Checks in the Digital Age

The advent of digital payment solutions has undoubtedly transformed the financial landscape, leading many to question the long-term viability of traditional payment methods like business checks. However, rather than disappearing, business checks are adapting, complementing digital systems, and maintaining their niche in a diversified payment ecosystem. Their enduring value lies in their specific advantages for documentation, control, and accessibility.

Complementing Digital Payment Systems

While electronic funds transfers (EFTs), automated clearing house (ACH) payments, wire transfers, and online payment gateways offer speed and convenience, they do not universally replace the need for checks. In many scenarios, checks serve as a valuable complement:

- Hybrid Payment Strategies: Businesses often employ a hybrid approach, using digital payments for recurring bills and high-volume transactions, while reserving checks for one-off payments, situations requiring detailed physical documentation, or dealing with payees who prefer traditional methods.

- Contingency Planning: Checks can serve as a reliable backup payment method in cases of digital system outages, cybersecurity incidents, or technical difficulties with online platforms.

- International Transactions (Specific Cases): While wire transfers dominate international payments, in certain contexts, particularly for smaller, less frequent cross-border transactions or those involving entities in regions with less developed digital infrastructure, a business check might still be a viable, albeit slower, option.

The key is not to view checks and digital payments as mutually exclusive but as tools within a broader financial toolkit, each with its optimal use case.

Digital Check Printing and Automation

Technology has also enhanced the creation and management of checks themselves. Digital check printing capabilities within accounting software allow businesses to:

- Customize Checks: Easily print professional, branded checks on demand, often using blank check stock, which is more secure than pre-printed checks.

- Automate Data Entry: Information from invoices and vendor records can be automatically populated onto checks, eliminating manual input errors.

- Batch Printing: For businesses with numerous payments, software enables batch printing of checks, significantly accelerating the process compared to manual writing.

- Digital Records: Every check printed through software is automatically recorded in the digital ledger, enhancing accuracy and ease of reconciliation.

Furthermore, services like remote deposit capture (RDC) allow businesses to digitally deposit checks received from customers by scanning them, reducing trips to the bank and speeding up fund availability.

When to Choose Checks Over Electronic Payments

Making an informed decision between checks and electronic payments requires a careful evaluation of the specific transaction and business needs.

- For Documentation and Audit Trails: Checks are often preferred for transactions where a verifiable, physical paper trail is critical, such as certain legal settlements, tax payments, or large capital expenditures that may undergo intense scrutiny.

- For Security and Fraud Control (Specific Types): While digital payments have robust security, checks with features like positive pay and certified checks offer unique layers of fraud protection that some businesses prioritize for sensitive transactions.

- For Payee Preference or Capability: If a vendor, contractor, or individual prefers receiving a physical check, or lacks the infrastructure to accept digital payments, checks remain the most accessible option.

- For Control Over Timing: Post-dating checks or the inherent float time before a check clears can offer businesses more precise control over cash flow than immediate digital transfers.

- For Expense Reimbursements (Certain Cases): For employee expense reimbursements, a check provides a clear record and can be easier to manage than individual digital transfers, especially if the employee doesn’t have direct deposit set up for reimbursements.

In conclusion, the business check, far from becoming obsolete, continues to serve as a vital financial instrument. Its enduring value lies in its unique combination of detailed record-keeping, robust security features, professional presentation, and the flexibility it offers in various payment scenarios. By understanding its anatomy, leveraging its strategic advantages, adhering to best practices, and integrating it wisely within a modern financial framework, businesses can ensure that checks remain a powerful and effective tool for managing their finances responsibly and efficiently.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.