In the landscape of personal and business finance, few terms are as ubiquitous—and yet as frequently misunderstood—as the “budget.” To the uninitiated, a budget often feels like a financial straightjacket, a list of restrictions designed to suck the joy out of spending. However, for those who have mastered their money, a budget is the exact opposite: it is a roadmap to freedom, a strategic plan for wealth accumulation, and a powerful tool for aligning one’s daily actions with their long-term life goals.

At its core, a budget is an itemized summary of expected income and expenses for a specific period. But beyond the numbers on a screen, it is a psychological contract with oneself. It is the process of giving every dollar a job before it leaves your hand. Whether you are managing a household, a side hustle, or a scaling corporation, understanding the mechanics of a budget is the first step toward financial sovereignty.

The Anatomy of a Modern Budget: More Than Just Tracking

To understand what a budget is, one must first distinguish between “tracking” and “budgeting.” Tracking is reactive; it tells you where your money went after it is gone. Budgeting is proactive; it tells your money where to go before the month begins. A professional-grade budget serves as a diagnostic tool for your financial health and a predictive model for your future wealth.

The Core Components: Income vs. Expenses

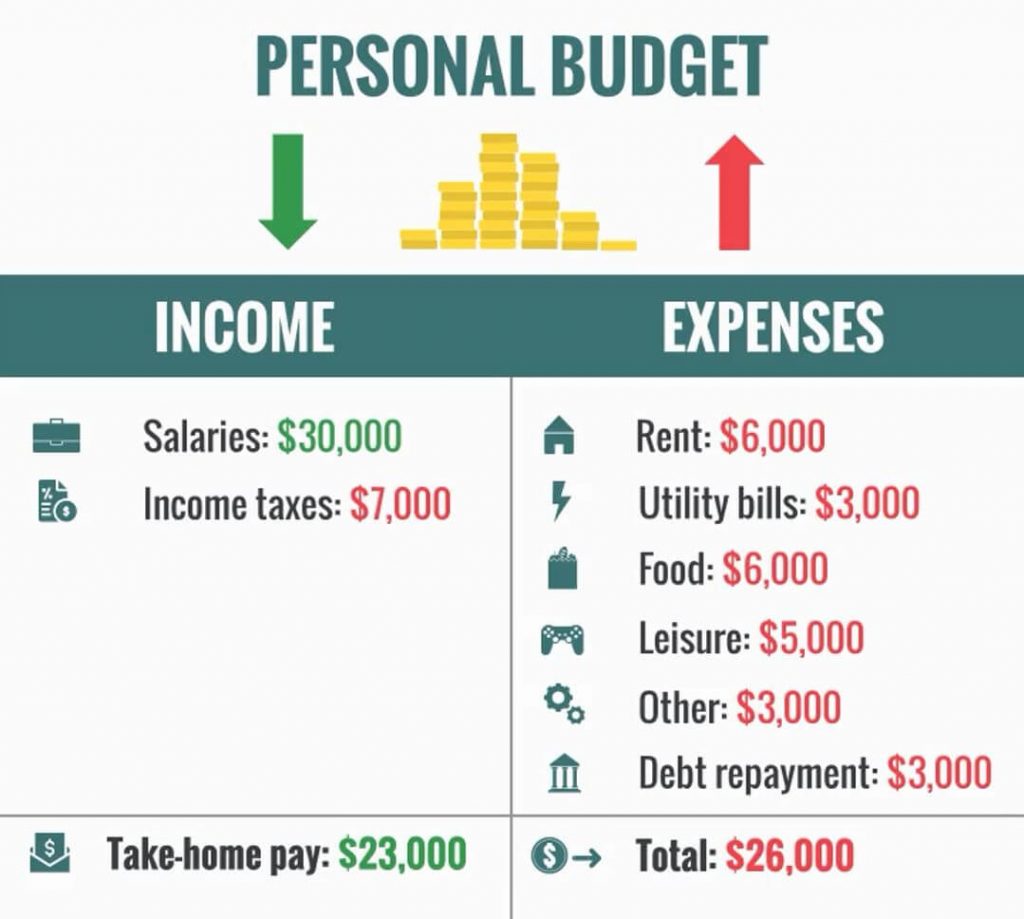

Every budget begins with two primary pillars: Income and Expenses. In the context of personal finance, income should always be calculated as “net income”—the amount that actually hits your bank account after taxes and 401(k) contributions. On the other side of the ledger are expenses, which are typically divided into fixed costs (rent, insurance, car payments) and variable costs (groceries, entertainment, utilities). The goal of a successful budget is to ensure that the delta between these two—the surplus—is maximized and directed toward productive assets.

The Psychology of Intentional Spending

Budgeting is fundamentally an exercise in prioritization. When you create a budget, you are forced to confront the reality of your opportunity costs. Every dollar spent on a luxury today is a dollar plus potential interest that cannot be invested for tomorrow. This doesn’t mean you shouldn’t spend; it means you should spend with intent. A well-designed budget allows for guilt-free spending because you have already accounted for your savings, bills, and future goals.

Strategic Budgeting Frameworks: Choosing Your Methodology

There is no “one-size-fits-all” approach to money management. The best budget is the one you can actually stick to. Over the decades, several frameworks have emerged as industry standards for managing personal and business cash flow.

The 50/30/20 Rule

Popularized by Senator Elizabeth Warren, this is perhaps the most accessible framework for beginners. It suggests allocating 50% of your net income to “Needs” (housing, food, basic utilities), 30% to “Wants” (lifestyle choices, dining out, hobbies), and 20% to “Savings and Debt Repayment.” This method is effective because it provides a high-level overview without requiring the user to track every penny, making it ideal for those who find granular detail overwhelming.

Zero-Based Budgeting

Zero-based budgeting (ZBB) is the gold standard for those who want total control over their finances. The philosophy is simple: Income minus Expenses equals Zero. This does not mean you have zero dollars in your bank account; it means that every single dollar of your income is assigned to a specific category—including savings, investments, and emergency funds. If you earn $5,000 this month, you must give all $5,000 a destination. This method eliminates “leakage,” where small, unmonitored purchases slowly erode your wealth.

The Envelope System and Sinking Funds

For those who struggle with overspending in specific categories, the Envelope System (either physical or digital) is a game-changer. You set a strict limit for categories like “Groceries” or “Entertainment,” and once that “envelope” is empty, spending stops for the month. Complementary to this is the concept of “Sinking Funds”—setting aside small amounts monthly for large, infrequent expenses like annual car insurance or holiday gifts. This prevents the “budget shock” that often occurs when an irregular expense ruins an otherwise perfect month.

The Mechanics of Building a Sustainable Financial Plan

Constructing a budget requires more than just a list of numbers; it requires a systematic process that accounts for the volatility of real life. A budget that is too rigid will break, while one that is too loose will be ignored.

Identifying and Categorizing Historical Data

The first step in creating a budget is looking backward. Most financial experts recommend reviewing the last three months of bank statements to identify patterns. You may think you spend $400 a month on food, but the data might reveal it’s actually $700. Categorizing these historical expenses into “Essentials,” “Lifestyle,” and “Obligations” provides the baseline data needed to set realistic targets for the future.

Setting “SMART” Financial Goals

A budget without a goal is just a math project. To stay motivated, your budget must be linked to specific, measurable, achievable, relevant, and time-bound (SMART) goals. Are you budgeting to build a six-month emergency fund? To pay off $20,000 in high-interest credit card debt? Or to capitalize a new side hustle? When your budget has a “Why,” the “How” becomes much easier to manage.

The Role of Financial Tools and Automation

In the modern era, manual spreadsheets are increasingly being replaced by sophisticated financial tools. Apps that sync with your bank accounts can provide real-time updates on your spending. However, the most powerful tool in the budgeting arsenal is automation. By automating transfers to savings and investment accounts on payday, you “pay yourself first,” ensuring that your financial goals are met before you have the chance to spend the money on discretionary items.

Advanced Budgeting: From Personal Finance to Business Growth

Once you have mastered the personal budget, the same principles can be applied to more complex financial scenarios, such as side hustles, freelance work, or small business management. In these contexts, budgeting transitions from a survival tool to a growth engine.

Managing Cash Flow for Side Hustles

For those earning online income or running a side business, the budget becomes a “Cash Flow Statement.” It is vital to separate personal and business finances. A business budget tracks “Burn Rate” (how much you spend to stay operational) and “ROI” (Return on Investment). By budgeting specifically for business expenses—such as software subscriptions, marketing, and inventory—you can clearly see if your venture is actually profitable or if it is merely an expensive hobby.

Integrating the Budget with an Investment Strategy

A budget is the primary feeder for an investment portfolio. In professional money management, the budget is used to identify the “Investable Surplus.” This is the capital that can be deployed into the stock market, real estate, or retirement accounts. Without a budget, most people find that their “surplus” mysteriously vanishes by the end of the month. By institutionalizing your savings through a budget, you create a consistent stream of capital that can benefit from the power of compound interest over time.

Overcoming Common Pitfalls and Sustaining the Habit

The reason most budgets fail is not a lack of math skills; it is a lack of flexibility and psychological resilience. Financial life is rarely a straight line, and a budget must be able to curve with the road.

Dealing with Irregular Income and Emergencies

One of the biggest hurdles to budgeting is irregular income, common among freelancers and commission-based professionals. The solution is the “Hill and Valley” approach: budgeting based on your lowest-earning month and using “surplus” months to build a buffer. Additionally, no budget is complete without an Emergency Fund. This is the safety net that prevents a flat tire or a medical bill from turning into a high-interest debt crisis.

Avoiding “Budget Burnout”

Many people start a budget with extreme intensity, cutting all “fun” spending, only to quit three weeks later. This is known as budget burnout. To maintain a budget long-term, it must include “blow money”—a small, no-questions-asked amount for pure enjoyment. Financial health is a marathon, not a sprint. If your budget doesn’t allow for an occasional coffee or a movie night, it isn’t a sustainable plan; it’s a temporary penance.

Conclusion: The Budget as a Tool for Empowerment

Ultimately, a budget is a declaration of your values. It shows, in cold hard numbers, what you truly care about. If you say you value travel but your budget shows 40% of your income going to dining out, the budget is providing you with the clarity needed to realign your life.

By defining your income, choosing a framework like the 50/30/20 rule or Zero-Based Budgeting, and using technology to automate your goals, you transform the budget from a chore into a competitive advantage. In the world of money, those who have a plan always end up working for those who don’t. Mastering “what is a budget” is the first step toward ensuring that you are the one in control of your financial destiny.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.