A Broker Price Opinion (BPO) is a critical financial tool in the real estate sector, offering an estimated value of a property prepared by a licensed real estate broker or agent. Unlike a full-fledged appraisal, a BPO provides a more cost-effective and time-efficient alternative, primarily utilized by financial institutions, investors, and loan servicers for various purposes that don’t legally mandate a Uniform Standards of Professional Appraisal Practice (USPAP)-compliant appraisal. Understanding the nuances of a BPO is essential for anyone involved in property finance, from lenders managing portfolios to investors evaluating distressed assets.

The Core Concept of a Broker Price Opinion

At its heart, a BPO is a professional opinion of a property’s likely selling price, formulated by a local real estate expert who possesses an intimate understanding of current market conditions. This opinion is typically requested when a quick, reasonably accurate valuation is needed without the exhaustive process and higher cost associated with a traditional appraisal.

Differentiating BPOs from Appraisals

While both BPOs and appraisals aim to determine a property’s value, they differ significantly in their methodology, depth, regulatory oversight, and intended use.

An appraisal is a comprehensive, highly regulated valuation performed by a state-licensed or certified appraiser. It adheres strictly to USPAP guidelines, requiring a detailed inspection of the property, an extensive analysis of comparable sales, and often incorporates multiple valuation approaches (sales comparison, cost, and income approaches). Appraisals are legally mandated for federally related transactions, such as most residential mortgage originations, ensuring a robust, unbiased, and extensively documented valuation suitable for underwriting decisions and investor protection. They are typically more expensive and take longer to complete.

A Broker Price Opinion, conversely, is a less formal, quicker, and more cost-effective valuation. It relies heavily on the broker or agent’s local market expertise, recent sales data from the Multiple Listing Service (MLS), and a more limited property inspection, often an exterior “drive-by” observation. BPOs are typically presented in a standardized report format but are not subject to the same stringent federal regulations as appraisals. They are designed for situations where a full appraisal is not legally required or economically feasible, offering a practical solution for institutions needing to assess collateral value rapidly.

When a BPO is Utilized

The specific scenarios where BPOs prove invaluable primarily revolve around efficiency and cost management within financial operations. Their application is widespread across the lifecycle of a real estate asset, especially within institutional contexts:

- Foreclosure and Real Estate Owned (REO) Properties: Lenders and servicers frequently use BPOs to determine an appropriate list price for properties acquired through foreclosure or to evaluate the potential recovery value of a property during the foreclosure process. This aids in setting realistic expectations for disposition.

- Short Sales: In situations where a property owner owes more than the property’s market value, a BPO helps lenders assess the property’s current worth to determine if accepting a sale price lower than the outstanding mortgage balance is a viable loss mitigation strategy.

- Loan Modifications and Workouts: When a borrower faces financial distress, a BPO can help re-evaluate the collateral value for loan modifications, allowing lenders to adjust terms based on current market realities.

- Portfolio Valuation: Financial institutions with large portfolios of real estate assets use BPOs for ongoing valuation monitoring, risk management, and capital allocation decisions without the prohibitive cost of appraising every property annually.

- Home Equity Lines of Credit (HELOCs): In certain scenarios, particularly for smaller HELOCs or subsequent draws, lenders may opt for a BPO over an appraisal to assess current property equity, provided regulatory requirements allow.

- Loss Mitigation Strategies: Beyond short sales and modifications, BPOs inform decisions regarding deeds-in-lieu of foreclosure and other workout options, helping lenders quantify potential losses or recoveries.

- Secondary Market Transactions: Entities buying or selling mortgage portfolios often rely on BPOs for a rapid assessment of the underlying collateral’s value.

The Process of Generating a BPO

The creation of a BPO follows a structured process, ensuring a consistent approach to valuation, albeit with less depth than an appraisal.

Data Collection and Analysis

Upon receiving a BPO order from a client (typically a lender, servicer, or asset manager), the licensed real estate broker or agent initiates the valuation process. The core of this process involves:

- Subject Property Information: Gathering basic details about the property, including its address, legal description, and any available public records data.

- Market Research: The agent delves into the Multiple Listing Service (MLS) and other proprietary databases to identify recent sales and active listings of comparable properties (comps) within the subject property’s immediate vicinity. Key criteria for comps include similar property type, size, age, condition, and location.

- Property Observation:

- Exterior BPO (Drive-by): This is the most common type. The agent observes the property’s exterior, noting its condition, curb appeal, neighborhood characteristics, and any apparent external features or issues. No interior access is granted.

- Interior BPO (Occupied/Unoccupied): Less frequent but still used, an interior BPO involves the agent gaining access to the property to assess its internal condition, layout, and features. This provides a more accurate picture but is more time-consuming and costly than an exterior BPO.

- Neighborhood Analysis: Evaluating the overall condition, desirability, amenities, and market trends of the neighborhood where the property is located. This includes factors like school districts, proximity to services, and general upkeep of surrounding homes.

- Market Conditions Assessment: Analyzing broader market trends such as average days on market, inventory levels, price trends (increasing, stable, or decreasing), and supply-demand dynamics.

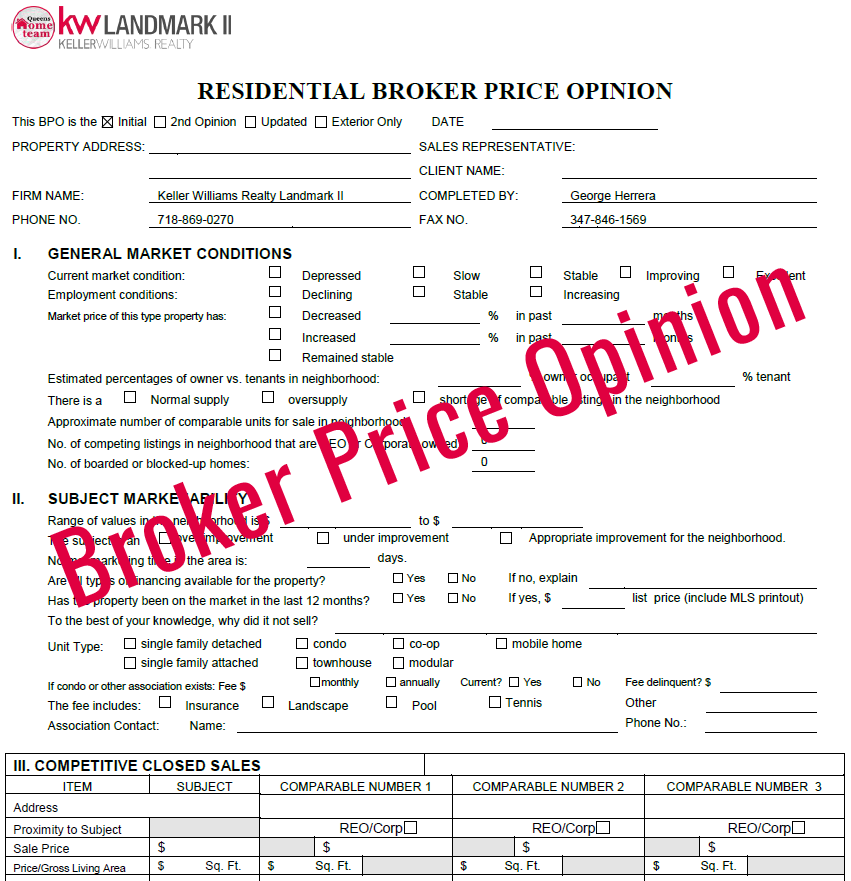

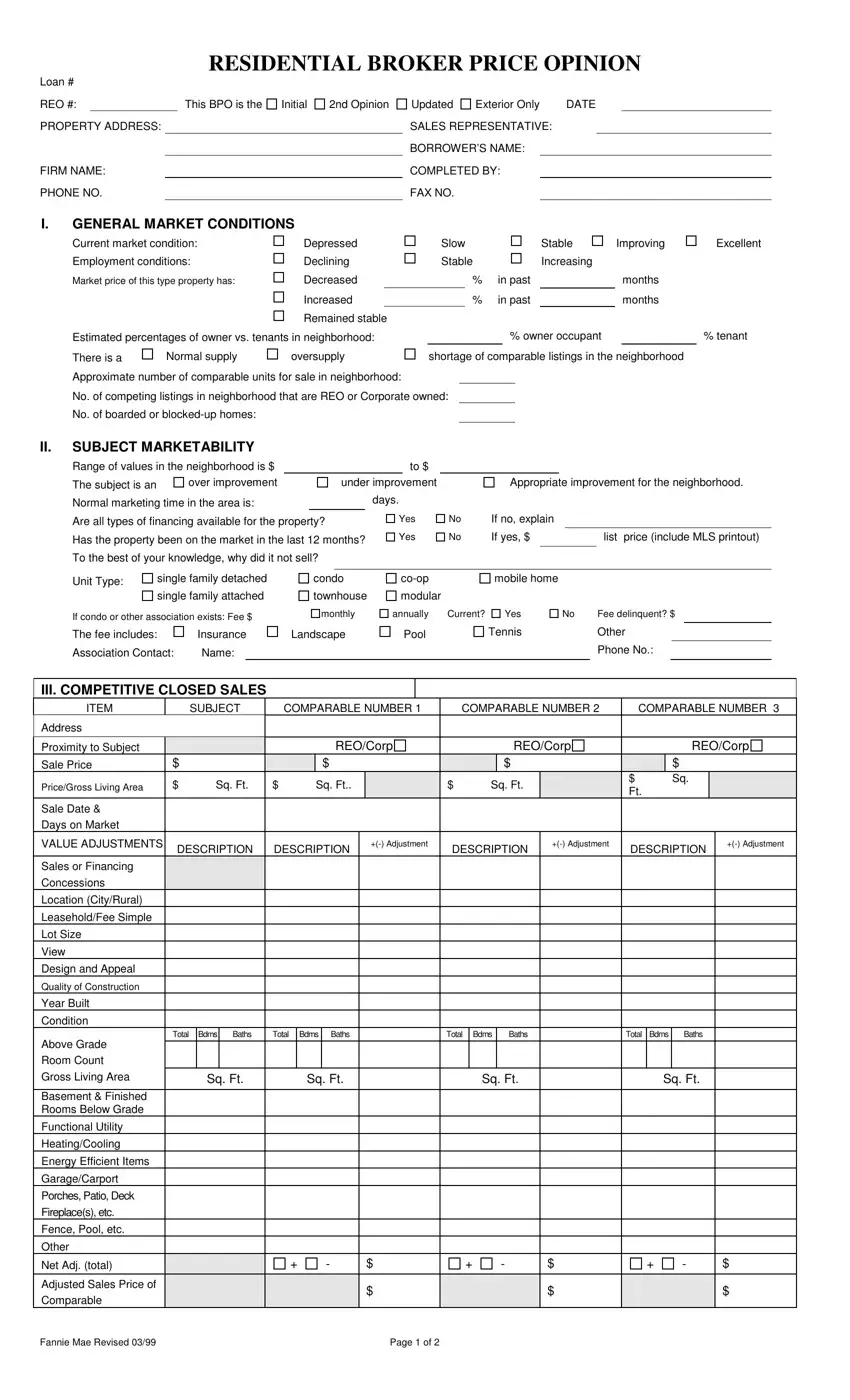

Key Components of a BPO Report

Once the data is collected and analyzed, the broker compiles a report that typically includes the following elements:

- Subject Property Details: Comprehensive information about the property being valued.

- Neighborhood Analysis: A summary of the subject property’s immediate area, including its characteristics and market trends.

- Market Conditions: A broader overview of the local real estate market, assessing its health and direction.

- Comparable Sales and Listings: A detailed list of 3-5 recently sold properties and 2-3 active listings that are similar to the subject property, along with adjustments made for differences (e.g., size, features, condition) to arrive at a comparable value.

- Property Condition Assessment: An evaluation of the property’s physical state, based on the type of BPO performed (exterior or interior). For exterior BPOs, this focuses on visible wear, required maintenance, or significant defects.

- Repair Estimates: If relevant, particularly for distressed properties, an estimated cost of necessary repairs to bring the property to market standard.

- Photos: A collection of images of the subject property (front, rear, street scene) and the comparable properties to support the condition assessment and valuation.

- Estimated Value Range and Recommended Value: The report concludes with a range of possible values for the property and the broker’s single recommended estimated value.

- Agent Certification and Disclosures: The broker’s certification that the BPO was prepared impartially and professionally, along with any necessary disclosures regarding the scope of work and limitations.

Advantages and Limitations for Financial Stakeholders

BPOs offer distinct advantages, primarily in speed and cost, making them an indispensable tool for financial entities. However, their limitations necessitate a clear understanding of when they are appropriate and when a more rigorous valuation is required.

Benefits for Lenders, Investors, and Servicers

The strategic use of BPOs provides significant operational and financial benefits:

- Cost-Effectiveness: BPOs are substantially less expensive than full appraisals, which translates to considerable savings for institutions managing large volumes of properties or assets. This cost efficiency is crucial in loss mitigation and REO management where multiple valuations may be needed.

- Speed and Efficiency: The turnaround time for a BPO is significantly shorter, often days compared to weeks for an appraisal. This rapid valuation capability is critical in fast-paced markets, foreclosure timelines, or situations requiring immediate financial decisions.

- Local Market Expertise: Real estate brokers and agents are immersed in their local markets daily. Their granular knowledge of neighborhood dynamics, current buyer demand, and recent transaction intricacies often provides a highly relevant and up-to-the-minute market perspective.

- Flexibility: Clients can order different types of BPOs (exterior vs. interior) based on their specific needs and the information required, providing a tailored valuation solution.

Acknowledging BPO Limitations

Despite their advantages, BPOs come with inherent limitations that must be understood and managed:

- Less Regulatory Oversight: BPOs are not subject to the Uniform Standards of Professional Appraisal Practice (USPAP), meaning there’s less standardization in methodology and reporting compared to appraisals. This can lead to greater variability in quality and consistency across different providers.

- Potential for Bias/Conflict of Interest: While brokers strive for objectivity, their primary role is often transactional. Though professional ethics demand impartiality, BPOs lack the stringent independence requirements imposed on appraisers, which could theoretically introduce subtle biases.

- Limited Scope: Exterior-only BPOs, by their nature, cannot account for interior property conditions, hidden defects, or significant upgrades/deteriorations not visible from the street. This can lead to inaccuracies if interior condition deviates significantly from market expectations.

- Not Suitable for All Transactions: Due to their lesser regulatory framework and limited scope, BPOs cannot be used for federally related mortgage transactions that require an appraisal by law.

- Reliance on Agent Judgment: The quality of a BPO heavily depends on the individual agent’s experience, judgment, and access to accurate data, which can vary.

Regulatory Landscape and Professional Standards

While BPOs are not governed by USPAP, their widespread use by financial institutions has led to certain regulatory guidelines and best practices to ensure their reliability.

Ensuring Accuracy and Compliance

Federal regulatory bodies, such as the Office of the Comptroller of the Currency (OCC), the Consumer Financial Protection Bureau (CFPB), and the Federal Deposit Insurance Corporation (FDIC), provide guidance for financial institutions regarding the appropriate use of BPOs. These guidelines emphasize:

- Robust Vendor Management: Institutions must have strong policies and procedures for selecting, overseeing, and reviewing the performance of BPO providers. This includes ensuring agents are licensed, experienced, and adhere to client-specific instructions.

- Quality Control: Implementing internal quality control processes to review BPO reports for accuracy, consistency, completeness, and adherence to established methodologies. This might involve re-validating comparable sales or reviewing the adjustments made.

- Appropriate Use Cases: Clearly defining when a BPO is acceptable versus when a full appraisal is mandatory, ensuring compliance with all lending regulations.

- Professionalism and Ethics: While not USPAP, industry associations often provide guidelines and ethical standards for BPO preparation, promoting responsible practice among real estate professionals.

- Standardization by National Providers: Many national BPO companies have developed their own rigorous training, quality control, and standardized reporting templates to ensure consistency and compliance across their networks of agents, addressing some of the inherent variability.

Strategic Integration of BPOs in Real Estate Finance

The strategic integration of BPOs within financial operations represents a sophisticated approach to managing real estate risk and maximizing efficiency.

Enhancing Decision-Making and Risk Management

BPOs serve as a powerful tactical tool for financial institutions, significantly impacting their decision-making processes and risk management frameworks:

- Facilitating Agile Loss Mitigation: By providing quick and affordable valuations, BPOs enable lenders to make timely decisions on loss mitigation strategies such as short sales, loan modifications, or deeds-in-lieu. This agility can minimize potential losses by allowing for quicker asset disposition or restructuring.

- Optimizing REO Asset Management: For real estate owned (REO) portfolios, BPOs are crucial for setting initial list prices, monitoring market value fluctuations over time, and adjusting marketing strategies. This iterative valuation helps in maximizing recovery values and reducing holding costs.

- Informing Portfolio Valuation and Stress Testing: Large lenders and investors use BPOs for ongoing monitoring of their real estate collateral portfolios. These valuations feed into stress tests and capital adequacy assessments, providing a dynamic view of potential risks and informing capital allocation decisions.

- Supporting Investment Decisions: Real estate investors often utilize BPOs for initial due diligence on potential property acquisitions, especially for distressed assets, offering a rapid and cost-effective way to gauge a property’s likely market value before committing to more extensive evaluations.

- Dynamic Risk Assessment: The ability to obtain quick, updated property values allows financial institutions to continuously assess the risk profile of their loan portfolios, particularly in volatile markets. This aids in proactive risk identification and mitigation.

In essence, BPOs act as a vital bridge between the need for accurate property valuation and the demands for speed and cost-efficiency in a complex financial landscape. Their strategic application, combined with robust oversight and a clear understanding of their limitations, empowers financial stakeholders to make more informed and timely decisions, ultimately contributing to healthier balance sheets and more resilient financial operations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.