In the modern financial landscape, banks are often viewed as monolithic structures of brick and mortar or, increasingly, as icons on a smartphone screen. Yet, at its core, a bank is the primary engine of the global economy. It is a highly regulated financial institution licensed to receive deposits and make loans. However, the definition of a bank has evolved significantly from the ancient grain warehouses of Mesopotamia to the high-frequency digital ledgers of today.

Understanding what a bank is—and how it functions—is essential for anyone looking to master their personal finance, grow a business, or navigate the complexities of the modern investment world. This guide explores the fundamental roles of banking, the diverse types of institutions that exist, and how they serve as the backbone of wealth creation and economic stability.

The Fundamental Role of Banking in the Global Economy

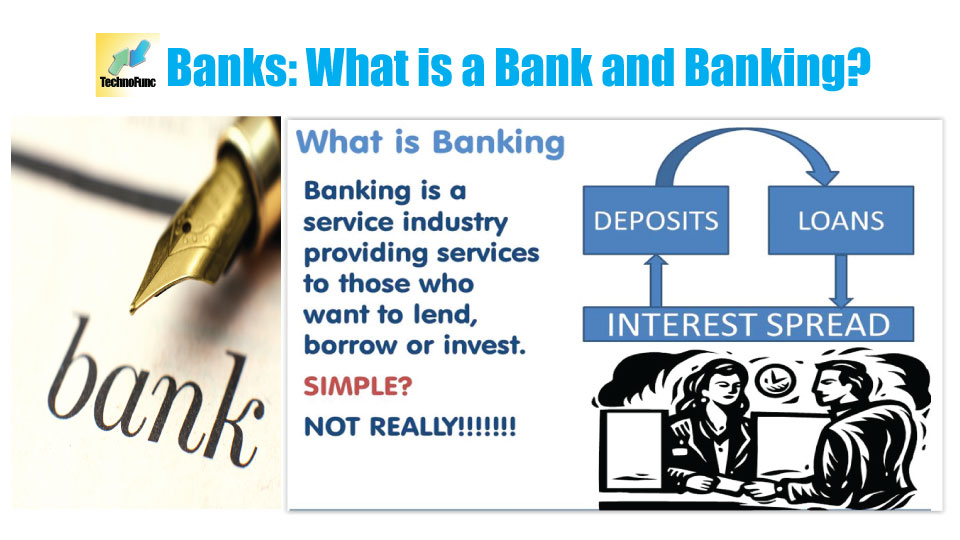

The primary function of a bank is to act as a financial intermediary. In the simplest terms, a bank sits between people who have extra money (savers) and people who need money (borrowers). By pooling the resources of thousands of depositors, banks can provide the large-scale capital necessary for individuals to buy homes and for businesses to expand.

Intermediation: Connecting Savers and Borrowers

When you deposit money into a savings account, you are effectively lending that money to the bank. In exchange, the bank provides you with security, liquidity (the ability to withdraw your money), and often a small amount of interest. The bank then takes the bulk of those deposits and lends them to borrowers—such as a family looking for a mortgage or a startup seeking a business loan. This process of “financial intermediation” ensures that capital does not sit idle but is instead put to work generating economic value.

Facilitating the Payment System

Beyond lending, banks are the gatekeepers of the global payment system. Without banks, every transaction would require a physical exchange of cash or barter. Banks provide the infrastructure for credit cards, debit cards, wire transfers, and direct deposits. By maintaining a ledger of who owns what, banks allow for the seamless transfer of value across the globe in seconds. This efficiency is what allows modern commerce to function at its current scale.

The Concept of Fractional Reserve Banking

One of the most misunderstood aspects of banking is “fractional reserve banking.” Most people assume that if they deposit $1,000, the bank keeps that exact $1,000 in a vault. In reality, banks are only required to keep a small fraction of their deposits (the reserve) on hand. The rest is lent out to generate profit. This system allows the money supply to expand, fueling economic growth, but it also necessitates strict government regulation to ensure that banks remain “liquid” enough to meet withdrawal demands.

Common Types of Banking Institutions

Not all banks are created equal. Depending on your financial needs—whether you are looking for a place to keep your paycheck, a way to take your company public, or a specialized loan for a farm—different types of institutions serve different purposes.

Retail Banks: The Personal Finance Hub

Retail banks are the most common type of bank for the average consumer. They focus on individual consumers, offering services such as checking and savings accounts, certificates of deposit (CDs), mortgages, auto loans, and personal credit cards. Retail banks can be massive national chains with thousands of branches or smaller community banks that focus on local relationships and personalized service.

Commercial Banks: Driving Business Growth

While retail banks focus on individuals, commercial banks focus on businesses. They provide the vital “blood flow” for the economy by offering commercial loans, lines of credit, and cash management services to small businesses and large corporations alike. Commercial banks help businesses manage their payroll, finance their inventory, and bridge the gap between paying for raw materials and receiving payment from customers.

Investment Banks: Navigating Capital Markets

Investment banks do not typically take deposits from the public. Instead, they act as intermediaries between large corporations and investors. Their primary roles include underwriting new debt and equity securities (helping a company “go public” via an IPO), facilitating corporate mergers and acquisitions (M&A), and providing complex financial advisory services. These institutions are the architects of the high-stakes world of Wall Street.

Central Banks: The Regulators of the Monetary System

A central bank—such as the Federal Reserve in the United States or the European Central Bank in the EU—is not a bank for the public. It is a “bank for banks.” Central banks are responsible for managing a nation’s currency, controlling inflation through interest rate adjustments, and ensuring the stability of the entire financial system. They act as the “lender of last resort” during financial crises to prevent the banking system from collapsing.

How Banks Generate Revenue and Manage Risk

Banks are businesses, and like any business, they must generate a profit to survive. However, their revenue models are unique because their “product” is money itself.

The Net Interest Margin (NIM)

The most traditional way a bank makes money is through the “spread,” or the Net Interest Margin. This is the difference between the interest the bank pays to depositors (an expense) and the interest it charges to borrowers (income). For example, if a bank pays you 1% interest on your savings account but charges a homeowner 7% on a mortgage, the 6% difference covers the bank’s operating costs and provides a profit margin.

Fee-Based Services and Commissions

In recent decades, banks have diversified their income streams by leaning heavily into fees. These include service charges for maintaining an account, overdraft fees, ATM fees, and foreign transaction fees. On the commercial and investment side, banks earn substantial commissions for advisory roles, wealth management services, and facilitating trades in the stock and bond markets.

Risk Management: Credit, Market, and Liquidity Risks

Making money in banking is a balancing act of risk.

- Credit Risk: The danger that a borrower will default on a loan. Banks use credit scores and collateral to mitigate this.

- Market Risk: The risk that the value of the bank’s investments (like government bonds) will drop due to changing interest rates.

- Liquidity Risk: The risk that too many depositors will want their money back at the same time (a “bank run”), exceeding the cash the bank has on hand.

The Evolution of Banking: From Brick-and-Mortar to Digital Neo-Banks

The banking industry is currently undergoing its most significant transformation since the invention of the credit card. The digital revolution has fundamentally changed how we interact with our money.

Online Banking and Mobile Apps

What was once a novelty is now a requirement. Traditional banks have invested billions into mobile technology, allowing customers to deposit checks via their cameras, transfer money instantly through Zelle or Venmo, and monitor their spending in real-time. This shift has reduced the importance of physical bank branches, leading many institutions to close physical locations in favor of a “digital-first” strategy.

The Rise of Fintech and Neo-Banks

A new breed of financial institutions, known as “neo-banks” or “challenger banks” (such as Chime, Revolut, or Monzo), has emerged. These companies operate entirely online without any physical branches. Because they have lower overhead costs, they often offer higher interest rates on savings and lower fees than traditional banks. While some are fully licensed banks, others are “fintech” companies that partner with traditional banks to provide the underlying financial infrastructure.

Security and Fraud Prevention in the Digital Age

As banking moves online, the nature of security has shifted. Physical bank robberies are rare; today, the battle is fought against hackers and identity thieves. Banks now employ sophisticated AI algorithms to detect unusual spending patterns and use multi-factor authentication (MFA) to protect accounts. The security of a bank is no longer just about the thickness of a vault door, but the strength of its encryption and the resilience of its servers.

How to Choose the Right Bank for Your Financial Goals

Choosing where to keep your money is one of the most important personal finance decisions you will make. The “best” bank depends entirely on your specific needs and financial habits.

Evaluating Interest Rates and Fees

If your goal is to grow your emergency fund, you should look for a High-Yield Savings Account (HYSA), often found at online-only banks. Conversely, if you frequently withdraw cash, you should prioritize a bank with a large, fee-free ATM network. Always read the fine print regarding “monthly maintenance fees”—many banks will waive these if you maintain a minimum balance or have a recurring direct deposit.

Accessibility and Technological Integration

For many, the quality of a bank’s mobile app is more important than the location of its nearest branch. Consider whether the bank integrates well with other financial tools you use, such as budgeting apps or investment platforms. If you own a business, you may need a bank that offers robust desktop features for wire transfers and payroll management.

Understanding FDIC and NCUA Insurance

In the United States, your deposits are generally protected by the Federal Deposit Insurance Corporation (FDIC) for banks, or the National Credit Union Administration (NCUA) for credit unions. This insurance typically covers up to $250,000 per depositor, per institution. In the rare event of a bank failure, this government backing ensures that your hard-earned money is safe. Always verify that any institution you choose is FDIC or NCUA insured.

Conclusion

A bank is far more than a place to store your cash; it is a dynamic participant in your financial journey. Whether it is providing the capital for your first home, offering the digital tools to manage your daily spending, or protecting your wealth through economic cycles, the banking system is central to modern life. By understanding the mechanisms of how banks operate, the types of institutions available, and the shift toward digital innovation, you can make more informed decisions and leverage the banking system to achieve your long-term financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.