Navigating the world of real estate finance requires a keen eye for detail and an understanding of how different loan structures impact your long-term wealth. Among the various financial instruments available to homebuyers and investors, the balloon mortgage stands out as one of the most unique—and potentially volatile—options. While traditional fixed-rate mortgages are designed for stability over 15 or 30 years, a balloon mortgage operates on a different logic, prioritizing short-term cash flow over long-term security.

In this guide, we will dissect the mechanics of the balloon mortgage, explore its strategic benefits for specific financial profiles, and examine the significant risks that borrowers must navigate to avoid financial catastrophe.

How a Balloon Mortgage Works: Structure and Mechanics

At its core, a balloon mortgage is a type of loan that does not fully amortize over the course of its term. In a standard mortgage, your monthly payments are calculated so that by the end of the loan period, the balance is zero. A balloon mortgage, however, separates the payment calculation from the actual life of the loan.

The Amortization Schedule vs. The Loan Term

The most distinctive feature of a balloon mortgage is the discrepancy between the “amortization period” and the “loan term.” For example, a borrower might take out a seven-year balloon mortgage. However, the monthly payments are calculated as if it were a 30-year fixed-rate mortgage.

This structure allows the borrower to enjoy the relatively low monthly payments associated with a long-term loan. For the duration of the term—usually five to ten years—the borrower pays principal and interest (or sometimes just interest) based on that 30-year schedule. This provides immediate relief to the borrower’s monthly budget, making the property more “affordable” in the short term.

The Final “Balloon” Payment

The defining moment of this financial instrument is the end of the loan term. Because the monthly payments were not high enough to pay off the entire principal within the five or seven-year window, a massive balance remains. This remaining balance is known as the “balloon payment.”

When the term expires, the entire outstanding principal—often hundreds of thousands of dollars—becomes due in a single lump sum. If a borrower took a $400,000 loan with a 7-year balloon, they might still owe $350,000 at the end of the seventh year. The borrower must then either pay this amount in cash, sell the property to cover the debt, or refinance the loan into a new mortgage.

The Strategic Advantages of Balloon Loans

Given the looming threat of a massive lump-sum payment, one might wonder why anyone would choose a balloon mortgage. In the realm of personal finance and real estate investment, however, these loans can be powerful tools when used with precision.

Lower Monthly Payments and Improved Cash Flow

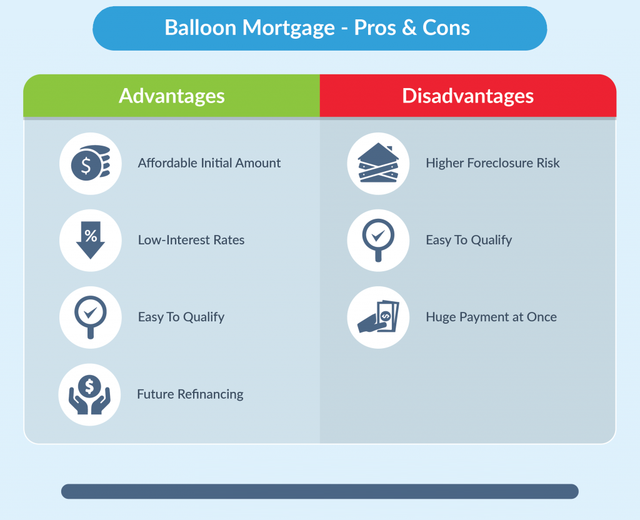

The primary draw of a balloon mortgage is the interest rate. Historically, balloon mortgages often carry lower interest rates than traditional 30-year fixed-rate mortgages. Because the lender is only committed to the loan for a short period (e.g., five years instead of thirty), they take on less long-term interest rate risk and can pass some of those savings to the borrower.

For a business owner or an individual with a variable income, the reduced monthly obligation can significantly improve monthly cash flow. This extra liquidity can be reinvested into other assets, used to fund business operations, or kept as a safety net.

Short-Term Financing for Investors and Flippers

Balloon mortgages are particularly popular among real estate investors and “house flippers.” If an investor plans to purchase a property, renovate it, and sell it within two to three years, the long-term stability of a 30-year mortgage is irrelevant.

In this scenario, the investor cares only about minimizing holding costs. A balloon mortgage provides the lowest possible monthly payment during the renovation phase. Since the investor intends to sell the property long before the balloon payment comes due, the “risk” of the lump sum is effectively neutralized by their exit strategy.

Significant Risks and Potential Pitfalls

While the advantages are clear for short-term holders, the balloon mortgage is widely considered one of the riskier products in the financial market. The danger lies in the assumption that the borrower will be in a position to pay or refinance when the clock runs out.

The Refinancing Risk

Most borrowers who take out a balloon mortgage do not intend to pay the final sum in cash. Instead, they plan to refinance the debt into a traditional mortgage before the term ends. This plan, however, relies on factors outside the borrower’s control: interest rates and credit lending standards.

If interest rates have spiked by the time the balloon payment is due, the borrower may find that they cannot afford the monthly payments on a new, traditional loan. Furthermore, if lending standards tighten—as they did during the 2008 financial crisis—the borrower might find that no bank is willing to offer a refinance, regardless of their credit score.

Market Fluctuations and Negative Equity

The second major risk is the value of the property itself. To refinance or sell the home to cover the balloon payment, the property must be worth at least as much as the remaining balance. If the local real estate market enters a downturn and the home’s value drops, the borrower may find themselves “underwater”—owing more on the balloon payment than the house is worth.

In this situation, the borrower cannot sell the house to pay off the debt without bringing extra cash to the closing table, and banks are unlikely to refinance a loan for more than the property’s appraised value. This often leads to a “default trap” where the borrower is forced into foreclosure.

Is a Balloon Mortgage Right for You? Key Considerations

Choosing a balloon mortgage is not a decision to be made lightly. It requires a sophisticated understanding of one’s financial trajectory and a high tolerance for risk.

Qualifying Factors and Borrower Profiles

Lenders typically reserve balloon mortgages for borrowers with strong credit profiles and substantial assets. Because the “exit” from the loan is so critical, the lender needs to see that the borrower has a high probability of either earning significantly more in the future or having the liquidity to handle a crisis.

Ideally, a balloon mortgage candidate is someone who:

- Expects a significant windfall (such as an inheritance or business sale) before the term ends.

- Is a corporate professional who moves every few years and intends to sell the home quickly.

- Is an investor with a proven track record of quick turnarounds.

Exit Strategies: Selling vs. Refinancing

Before signing the paperwork for a balloon loan, a borrower must have a “Plan A,” “Plan B,” and “Plan C.”

- Plan A is usually selling the property for a profit or refinancing at a lower rate.

- Plan B might involve using personal savings or liquidating other investments to pay down the balance.

- Plan C is the contingency for a market crash.

Without a clear, documented exit strategy, a balloon mortgage transitions from a financial tool into a financial gamble.

Alternatives to Balloon Mortgages in Today’s Market

For those who find the concept of a balloon payment too daunting, there are other ways to achieve lower initial payments without the “all-or-nothing” risk of a lump sum.

Adjustable-Rate Mortgages (ARMs)

An Adjustable-Rate Mortgage (ARM) offers a lower initial interest rate for a set period (like 5, 7, or 10 years), similar to a balloon loan. However, instead of the entire balance becoming due at the end of that period, the interest rate simply adjusts to current market levels. While your monthly payment might increase significantly, you aren’t faced with the immediate need to produce hundreds of thousands of dollars or lose your home.

Fixed-Rate Options with Interest-Only Periods

Some lenders offer interest-only mortgages where the borrower is only required to pay the interest for the first several years. This achieves the goal of low monthly payments. After the interest-only period ends, the loan converts into a standard amortizing loan. This provides a smoother transition than a balloon payment, though it results in much higher payments later in the loan’s life.

Conclusion

A balloon mortgage is a sophisticated financial instrument that prioritizes immediate cash flow and short-term flexibility. For the right borrower—typically a savvy investor or a short-term resident with a guaranteed exit strategy—it can be a brilliant way to leverage capital.

However, for the average homebuyer seeking the “American Dream” of long-term homeownership, the balloon mortgage is often a dangerous path. The history of the housing market is littered with stories of borrowers who assumed they could “just refinance later,” only to be caught in a pincer movement of falling home prices and rising interest rates. In the world of money and finance, the balloon mortgage reminds us of a fundamental truth: the lower the payment today, the higher the risk tomorrow. Always ensure your financial foundation is solid enough to handle the “pop” when the balloon finally reaches its ceiling.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.