When navigating the complex landscape of home financing, the terminology can often feel like a foreign language. Among the various loan products available, the 10/1 Adjustable Rate Mortgage (ARM) stands out as a unique hybrid vehicle. It combines the stability of a fixed-rate loan with the potential flexibility of an adjustable-rate structure, making it a powerful—albeit sometimes misunderstood—tool in a homebuyer’s financial arsenal. Understanding whether this mortgage product aligns with your long-term goals requires a deep dive into its mechanics, its inherent risks, and the specific life scenarios where it shines.

The Anatomy of a 10/1 ARM

To comprehend a 10/1 ARM, it is helpful to break the name down into its two primary components: the fixed period and the adjustment interval.

![]()

Understanding the Fixed-Rate Window

The “10” in 10/1 refers to the initial period during which your interest rate remains locked. For the first ten years of the loan, your principal and interest payments will not change, regardless of what is happening in the broader financial markets. This provides a significant degree of predictability, rivaling that of a traditional 30-year fixed-rate mortgage. During this decade, you can budget with confidence, knowing exactly what your housing costs will be.

The Adjustment Phase

The “1” indicates how frequently the rate will adjust once that initial ten-year period concludes. After the first decade, your interest rate will be subject to change once every year. These adjustments are tied to a financial index—usually the Secured Overnight Financing Rate (SOFR) or a similar benchmark—plus a “margin” defined by your lender. When the index rises, your interest rate rises; when it falls, your rate may follow suit.

Weighing the Benefits of the 10/1 Structure

Many borrowers gravitate toward the 10/1 ARM because it offers an attractive middle ground. It is designed for individuals who are confident that their current home is not their “forever” home, or for those who anticipate significant changes in their financial profile within the next decade.

Lower Initial Interest Rates

Historically, lenders offer lower initial interest rates on 10/1 ARMs compared to 30-year fixed-rate mortgages. Because the lender is shifting some of the long-term interest rate risk onto the borrower after the ten-year mark, they incentivize the product by keeping the initial rate competitive. For a borrower who plans to sell the property or refinance the loan before the end of the tenth year, this translates to substantial interest savings.

Budgeting Predictability for a Decade

While some borrowers fear the word “adjustable,” a decade is a long time in the world of personal finance. Ten years is often long enough to raise children, advance significantly in a career, or benefit from home equity appreciation. By choosing a 10/1 ARM, you lock in a stable payment for a duration that exceeds the average time most Americans spend in a single primary residence. In this sense, the 10/1 ARM functions almost exactly like a fixed-rate loan for the vast majority of the time the borrower actually owns the property.

Risks and Protective Measures

While the benefits are clear, entering into an adjustable-rate agreement without understanding the potential downside is a recipe for financial stress. The primary risk is the “payment shock” that can occur once the adjustment period begins.

The Impact of Interest Rate Volatility

If the financial climate changes and interest rates spike by the time your eleventh year rolls around, your mortgage payment could increase significantly. It is vital to model different scenarios: what would your monthly payment look like if your rate climbed by 2% or 3% after year ten? If that number causes alarm, you must have a clear exit strategy in place, such as selling the home or refinancing into a fixed-rate loan before the adjustment period kicks in.

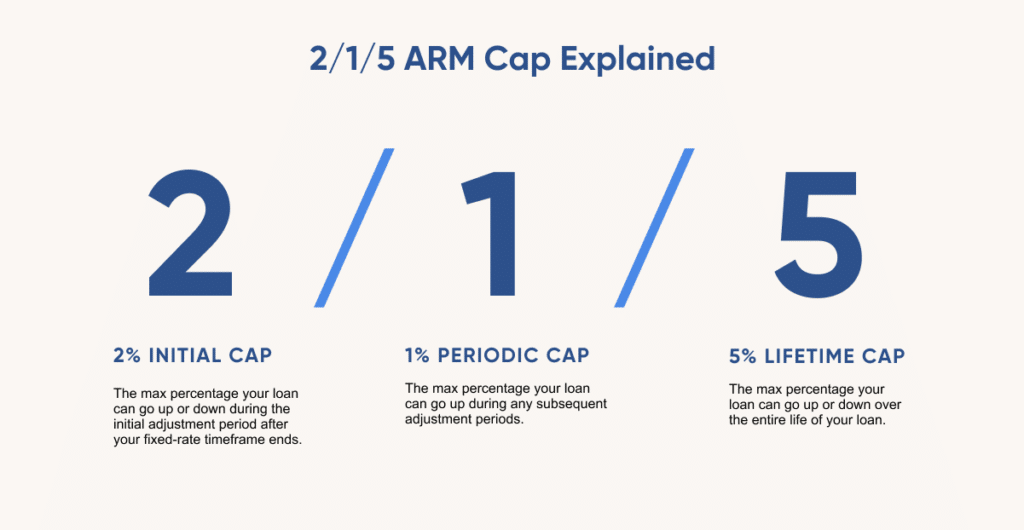

Understanding Rate Caps

To protect borrowers from runaway costs, 10/1 ARMs come with built-in safeguards known as “rate caps.” These caps limit how much your interest rate can change at any given adjustment interval and over the life of the loan.

- Initial Adjustment Cap: This limits how much the rate can increase the first time it adjusts.

- Subsequent Adjustment Cap: This limits how much the rate can change during each annual adjustment after the first.

- Lifetime Cap: This sets the absolute ceiling for how high your interest rate can go over the entire life of the mortgage.

Before signing your closing documents, ensure you are fully aware of these caps. They serve as your primary defense against extreme market volatility and provide a “worst-case scenario” framework that you can use to stress-test your financial plan.

Is a 10/1 ARM Right for You?

Choosing a mortgage is not just about the interest rate; it is about matching the financial product to your life plan. A 10/1 ARM is not a one-size-fits-all solution, but it is an excellent fit for specific borrower archetypes.

The “Step-Up” Homebuyer

If you are currently purchasing a home that you view as a mid-term transition—perhaps a starter home or a property you intend to upgrade within the next decade—the 10/1 ARM is highly efficient. By keeping your monthly payment lower during the initial ten years, you can apply the extra cash toward other financial goals, such as aggressively paying down other debts, increasing your retirement contributions, or building a home improvement fund.

The Career-Focused Professional

Young professionals or those in industries with rapid income growth often benefit from these products. If you anticipate that your income will be significantly higher in ten years, you may feel comfortable with the idea of refinancing or even paying off the balance early. For these borrowers, the 10/1 ARM serves as a bridge, offering a low cost of entry while providing ample time to build the equity or the cash reserves necessary to pivot to a different financial structure later.

The Debt-Averse Conservative

If you are the type of person who loses sleep over the possibility of a rate hike, a 10/1 ARM might not be the best choice. Even though the risk of adjustment is ten years away, the psychological weight of an adjustable loan is real. If your priority is absolute peace of mind and you intend to stay in your home for 30 years, a standard 30-year fixed-rate mortgage is generally the superior choice, regardless of the potential savings an ARM might offer.

Conclusion: Strategic Financial Planning

The 10/1 Adjustable Rate Mortgage is a versatile instrument that favors the well-informed. It provides a unique balance of lower initial costs and long-term payment stability, but it demands a proactive approach to financial management.

To utilize this product effectively, you must maintain a disciplined timeline. Treat the tenth year as a milestone date on your calendar. Well before that year arrives, evaluate your financial health, your equity position, and the current interest rate environment. Determine whether your best course of action is to sell the property, refinance into a new fixed-rate mortgage, or accept the adjusted rate if it remains competitive.

By viewing the 10/1 ARM not as a permanent debt structure, but as a strategic phase in your overall wealth-building journey, you can leverage it to maximize your cash flow and optimize your homeownership experience. As with all major financial decisions, consult with a mortgage professional who can provide a detailed amortization schedule and help you compare the long-term cost of a 10/1 ARM against a traditional fixed-rate loan. With the right data and a clear vision for your future, the 10/1 ARM can be a powerful partner in your pursuit of financial stability and homeownership success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.