Navigating the landscape of home financing can feel like deciphering a complex code, especially when interest rates are in flux. For many homebuyers, the traditional 30-year fixed-rate mortgage is the default choice, offering the peace of mind of a consistent payment. However, as the real estate market evolves, “hybrid” products have gained significant traction. One such product that has piqued the interest of savvy borrowers is the 10/6 Adjustable-Rate Mortgage (ARM).

A 10/6 ARM represents a middle ground between the absolute stability of a fixed-rate loan and the initial affordability of an adjustable-rate loan. By understanding the mechanics, risks, and rewards of this specific financial instrument, borrowers can determine if it aligns with their long-term financial goals or if it poses an unnecessary risk to their equity.

What Exactly is a 10/6 ARM?

The 10/6 ARM is a type of hybrid mortgage where the interest rate remains fixed for an initial period and then adjusts periodically for the remainder of the loan term. To understand how it works, we must break down the two numbers in its name.

The Meaning of “10” and “6”

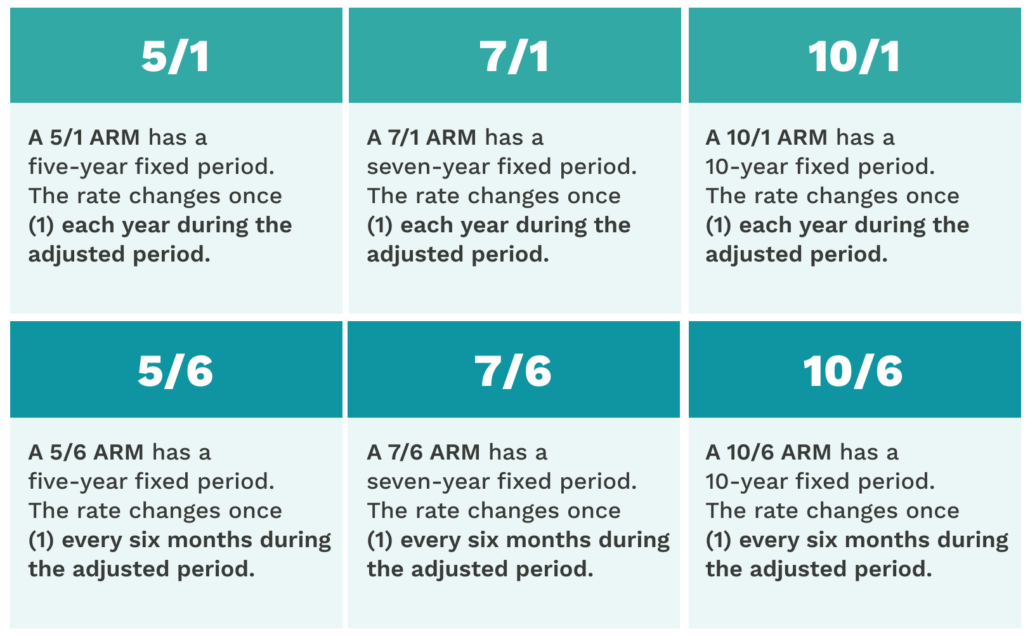

In a 10/6 ARM, the first number—10—represents the “fixed-rate period.” For the first 120 months (10 years) of the loan, your interest rate is locked. This provides a decade of predictable monthly payments, which is significantly longer than the more common 3/6 or 5/6 ARMs.

The second number—6—refers to the “adjustment frequency” once the fixed period expires. In this case, the interest rate can change every six months. Historically, most ARMs adjusted annually (e.g., a 10/1 ARM), but the industry has largely shifted toward a six-month adjustment cycle to better reflect real-time market volatility.

How the Adjustment Phase Works

After the initial 10-year period ends, the loan enters its adjustable phase. Your new interest rate is calculated by adding a “margin” to a specific “index.” While your payment was stable for the first decade, the subsequent years could see your monthly obligation rise or fall significantly depending on the health of the economy and the benchmark interest rates set by central banks.

The Mechanics of Rate Adjustments: Index, Margin, and Caps

To truly master the concept of a 10/6 ARM, a borrower must look beyond the initial “teaser” rate and understand the mathematical formula that governs the loan’s future. The total interest rate during the adjustable period is known as the “fully indexed rate.”

The Role of the SOFR Index

Most modern 10/6 ARMs are tied to the Secured Overnight Financing Rate (SOFR). This index replaced the older LIBOR (London Interbank Offered Rate) as the standard benchmark for many consumer loans. The SOFR is based on the rates that institutions pay each other for overnight loans backed by U.S. Treasury securities. Because it is based on actual transactions rather than estimates, it is considered a very transparent and reliable index.

When your 10-year fixed period ends, the lender looks at the current SOFR value. They then add a “margin”—a fixed percentage points (often around 2% to 3%)—that stays the same for the life of the loan.

Understanding Interest Rate Caps

To prevent borrowers from facing “payment shock” (a sudden, massive increase in monthly payments), 10/6 ARMs come with interest rate caps. These are legal limits on how much your rate can increase. There are typically three types of caps:

- Initial Cap: Limits how much the rate can rise at the first adjustment (after year 10).

- Periodic Cap: Limits how much the rate can rise during any single six-month adjustment period.

- Lifetime Cap: The absolute maximum interest rate you could ever pay, regardless of how high market rates climb.

For example, a “5/2/5” cap structure means your rate can’t go up more than 5% at the first adjustment, no more than 2% in any subsequent six-month period, and no more than 5% above the original starting rate over the life of the loan.

Comparing the 10/6 ARM to Traditional Fixed-Rate Mortgages

The primary reason borrowers choose a 10/6 ARM over a 30-year fixed-rate mortgage is the initial interest rate. Because the borrower is taking on the risk of future rate fluctuations, the lender usually offers a lower “introductory” rate during the first 10 years.

The “Interest Rate Cliff” Risk

The 30-year fixed-rate mortgage is a “set it and forget it” product. You know exactly what you will owe in year 2, year 15, and year 29. With a 10/6 ARM, you face what some financial advisors call the “interest rate cliff.” At the start of year 11, if the SOFR has skyrocketed, your monthly payment could jump by hundreds or even thousands of dollars.

However, because the fixed period is a full decade, many borrowers feel they have enough of a “buffer” to build equity or increase their income before that cliff arrives.

Cost-Benefit Analysis for Long-Term Homeowners

If you plan to live in your home for 30 years, a fixed-rate mortgage is almost always the safer bet. But statistics show that the average homeowner sells or refinances every seven to ten years. If you are certain you will move or upgrade your home within a decade, the 10/6 ARM allows you to enjoy a lower interest rate for the entire duration of your stay without ever reaching the adjustable phase. In this scenario, you are essentially getting a 10-year fixed loan at a discount.

Is a 10/6 ARM Right for You? Pros, Cons, and Strategic Scenarios

Choosing a mortgage is not just about finding the lowest rate; it is about matching the loan’s structure to your life’s timeline. The 10/6 ARM is a specialized tool that serves specific financial profiles exceptionally well, while being a poor fit for others.

When the 10/6 ARM Makes Financial Sense

- The “Transitional” Buyer: If you are a professional who expects to be relocated for work within 10 years, or if you are buying a “starter home” that you know you will outgrow as your family expands, the 10/6 ARM is an excellent choice. You save money on interest during the years you actually live in the home.

- The High-Income Growth Expectation: If you are early in a high-earning career (such as a medical resident or a junior law partner), you may opt for the lower initial payments of a 10/6 ARM now, knowing that in 10 years, your income will be significantly higher, allowing you to easily absorb a rate hike or pay off the balance entirely.

- Current High-Rate Environment: When standard mortgage rates are high, the discount offered by an ARM can make the difference between a home being affordable or out of reach.

Potential Pitfalls and Market Volatility

The greatest risk of the 10/6 ARM is the “unforeseen life event.” If you plan to move in year 9 but the housing market crashes and you find yourself “underwater” (owing more than the home is worth), you may be unable to sell or refinance. You would then be forced to stay in the home and face the six-month rate adjustments, which could happen during a period of high inflation and rising interest rates.

Furthermore, the 6-month adjustment period is more aggressive than the old 1-year standard. This means that in a rising-rate environment, your mortgage payment could increase twice a year, making budgeting much more difficult than it would be with a more stable loan product.

Planning Your Exit Strategy

No one should enter a 10/6 ARM without a clear “exit strategy.” Because the loan becomes inherently more volatile after year 10, you must have a plan for what happens when the clock runs out.

Refinancing Before the Adjustment

The most common exit strategy is to refinance the loan into a fixed-rate mortgage before the 10-year mark. If interest rates have dropped since you originally took out the loan, you can lock in a low fixed rate for the remaining life of the mortgage. However, this strategy assumes you will have enough equity in the home to qualify for a refinance and that your credit score remains healthy.

Accelerated Debt Paydown

Another strategy is to use the monthly savings from the lower 10/6 ARM rate to pay down the principal of the loan aggressively. By making extra payments during the first 10 years, you reduce the total balance upon which the future adjustable interest will be calculated. If you manage to pay off a significant portion of the principal, even a sharp increase in the interest rate in year 11 may result in a monthly payment that is still manageable because it is based on a much smaller loan amount.

Conclusion

The 10/6 ARM is a sophisticated financial tool that offers a unique blend of short-term stability and long-term flexibility. It is particularly attractive in a high-interest-rate environment where every percentage point counts toward monthly affordability. By providing a 10-year fixed window, it offers significantly more security than shorter-term ARMs, making it a viable option for a wide range of homeowners.

However, the “6” in the 10/6 ARM serves as a reminder that the market is always moving. Borrowers must weigh the immediate savings of a lower rate against the long-term uncertainty of semi-annual adjustments. As with any significant financial decision, the key to success lies in honest self-assessment: How long do you really plan to stay in the home, and how much volatility can your monthly budget truly withstand? For those with a clear 10-year plan, the 10/6 ARM may just be the smartest way to finance the American dream.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.