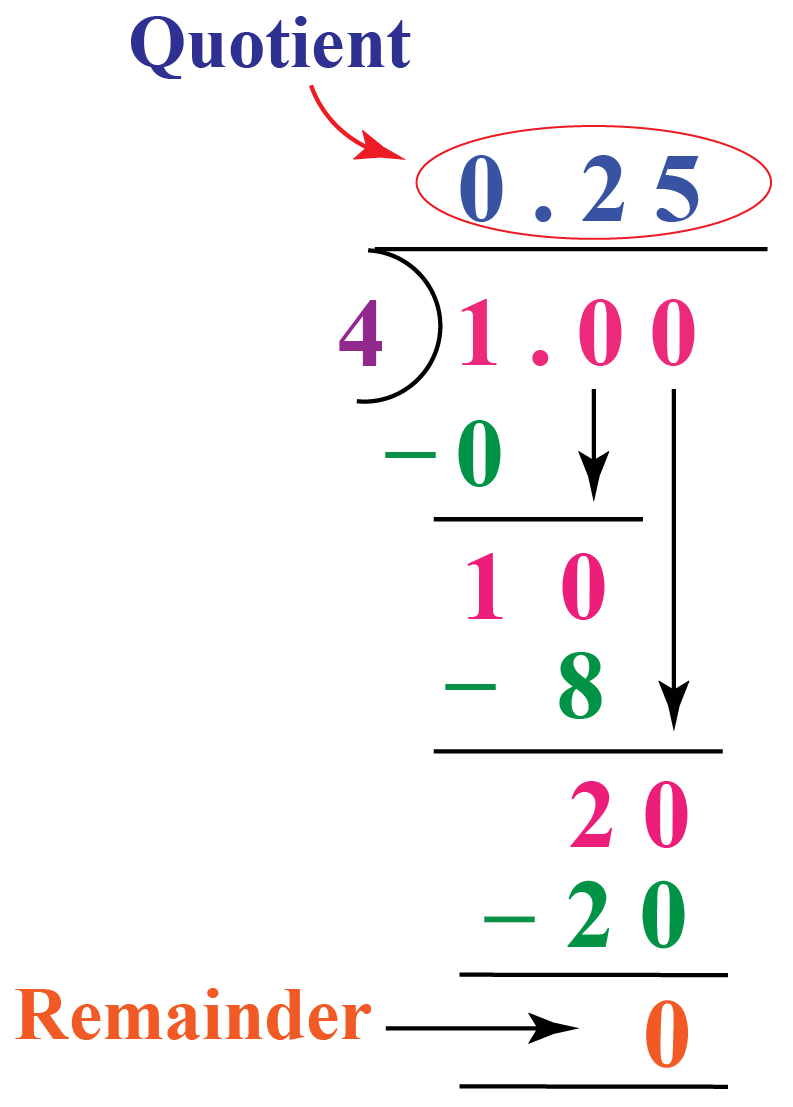

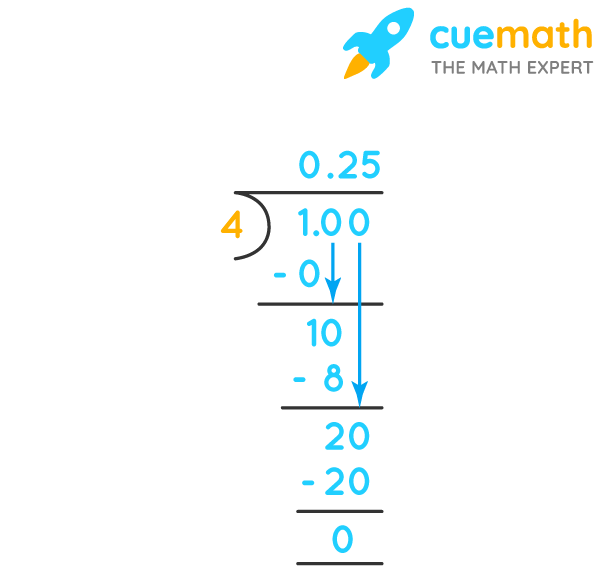

In the world of mathematics, converting a mixed fraction into a decimal is a fundamental skill. To answer the core question: 4 and 1/4 as a decimal is 4.25. While this conversion is straightforward—dividing the numerator (1) by the denominator (4) to get 0.25 and adding it to the whole number (4)—the implications of this specific number in the realm of finance are profound.

In the financial sector, we rarely see 4 and 1/4 written as a fraction. Instead, it appears as 4.25%, a figure that often serves as a pivot point for interest rates, dividend yields, and mortgage benchmarks. Understanding the transition from a simple fraction to a decimal is the first step in mastering the “basis point” language of bankers, investors, and financial analysts.

The Mathematics of Finance: Why Decimal Precision Matters

The conversion of 4 and 1/4 to 4.25 is more than a classroom exercise; it is the language of precision in modern banking. In finance, decimals allow for granular calculations that fractions cannot easily support, especially when compounding interest or calculating the “time value of money.”

Converting 4 and 1/4 to 4.25

To convert any mixed fraction to a decimal, you follow a two-step process. First, address the fractional component (1/4). By dividing 1 by 4, you arrive at 0.25. Second, you combine this with the whole number. Thus, 4 + 0.25 equals 4.25. In financial terms, if you are looking at an interest rate of 4 and 1/4 percent, you are dealing with a decimal rate of 0.0425 when used in formulas. This precision is vital because even a thousandth of a decimal point can result in thousands of dollars of difference over the life of a multi-million dollar loan or an investment portfolio.

The Precision of Decimals in Global Markets

Global markets operate on “basis points” (BPS). One basis point is equal to 1/100th of 1%, or 0.01. Therefore, the “1/4” in 4 and 1/4 represents 25 basis points. When the Federal Reserve adjusts interest rates, they rarely move in whole numbers; they move in increments of 25 basis points. Understanding that 4.25 contains exactly twenty-five “hundredths” allows investors to communicate effectively with brokers and understand how a “quarter-point” shift impacts their net worth.

4.25% in the World of Interest Rates and Mortgages

Perhaps the most common place a consumer will encounter the number 4.25 is in the mortgage market. For decades, 4.25% has been viewed as a psychological and historical benchmark for “affordable” long-term debt. When a 30-year fixed-rate mortgage sits at 4.25%, the math of homeownership changes significantly compared to higher or lower brackets.

Fixed-Rate Mortgages and Monthly Payments

If you were to take out a $400,000 mortgage at 4 and 1/4 percent (4.25%), your principal and interest payment would remain stable for the life of the loan. In this scenario, the decimal 4.25 is used by the bank’s amortization software to calculate how much of your monthly payment goes toward interest versus principal. Because the decimal is slightly higher than 4.00, the “extra” 0.25 represents a significant sum of interest over 30 years. On a $400,000 loan, that 0.25% difference can equate to over $20,000 in additional interest paid over the life of the loan. This highlights why understanding the decimal value of your interest rate is a critical component of personal debt management.

The Federal Reserve and Basis Points

The “quarter-point” move is the standard tool of central banks. When the news reports that the Fed has raised rates to 4.25%, they are signaling a tightening of the money supply. This decimal figure influences everything from the prime rate (which affects credit cards) to the yield on government bonds. For a business owner looking for finance, seeing 4 and 1/4 as a decimal (4.25) is the signal to calculate the “Weighted Average Cost of Capital” (WACC). If the cost of borrowing is 4.25%, any internal project must generate a return higher than this decimal to be considered profitable.

Investment Yields: Analyzing a 4.25% Return

For investors, 4.25% is often seen as a “yield” figure. Whether you are looking at a Certificate of Deposit (CD), a government bond, or a high-yield savings account, the decimal 4.25 represents the annual return on your capital.

High-Yield Savings Accounts (HYSA) and CDs

In a high-interest environment, many fintech banks offer rates around 4.25% APY (Annual Percentage Yield). This is a significant jump from the 0.01% rates seen in traditional “big box” banks. By understanding that 4 and 1/4 is 4.25, an investor can quickly calculate their earnings. For every $10,000 deposited at a 4.25% rate, the account holder earns $425 in interest per year. This simple decimal multiplication is the foundation of “passive income” planning and allows savers to compare different financial products with ease.

Dividend Stocks and REITs

In the stock market, 4.25% is a common dividend yield for mature companies or Real Estate Investment Trusts (REITs). When a stock is described as having a “4 and 1/4 percent yield,” it means the annual dividends paid out per share divided by the current stock price equals 0.0425. For an income-focused investor, this decimal is the “hurdle rate.” If inflation is running at 3%, a 4.25% yield provides a “real” return of 1.25%. Without converting that 1/4 into .25, the comparative analysis against inflation and other assets becomes cumbersome and prone to error.

Real Estate and Commercial Finance Applications

Beyond residential mortgages, the number 4.25 plays a vital role in commercial real estate valuation, specifically through “Cap Rates” and debt coverage metrics.

Capitalization Rates (Cap Rates)

A “Cap Rate” is the ratio of Net Operating Income (NOI) to the property asset value. If an apartment complex is trading at a “4 and a quarter cap,” it means the property generates a 4.25% return on its purchase price before mortgage considerations. In high-demand markets like New York or San Francisco, a 4.25 cap is often considered a strong valuation. Investors use this decimal to determine if they are overpaying for an asset. A move from a 4% cap to a 4.25% cap might seem small, but on a $10 million building, that 0.25% represents a $25,000 difference in annual income or a significant shift in the underlying property value.

Debt Service Coverage Ratios (DSCR)

Commercial lenders use the decimal 4.25 to stress-test loans. They want to ensure that a business can cover its debt even if interest rates rise. If a borrower has a loan at 4.25%, the lender calculates the DSCR to ensure the business’s cash flow is significantly higher than the 4.25% interest obligation. For the business owner, knowing the decimal equivalent of their interest rate allows them to manage their “leverage” effectively, ensuring that their cost of debt does not outpace their revenue growth.

Tools for Financial Precision

In the modern era, we don’t have to do these conversions in our heads, but we must know how to input them into the tools that manage our money.

Using Financial Calculators

Whether you are using a physical TI-BA II Plus or an online mortgage calculator, these tools do not accept “4 and 1/4” as an input. They require the decimal format. Mastering the input of 4.25 into the “I/Y” (Interest per Year) field is essential for any student of finance or professional investor. Incorrectly entering the fraction can lead to catastrophic errors in calculating future value (FV) or present value (PV).

Excel and Spreadsheet Mastery for Personal Finance

For those who track their net worth or business expenses in Excel or Google Sheets, the decimal 4.25 is the only way to perform automated calculations. Using the cell format for “Percentage” will automatically turn “0.0425” into “4.25%.” This allows users to build complex financial models—such as retirement projectors or debt snowball spreadsheets—that accurately reflect the reality of their financial situation.

In conclusion, while the question “what is 4 and 1/4 as a decimal” originates in basic arithmetic, its true value is found in the world of money. Whether you are signing a mortgage, choosing a savings account, or evaluating a commercial real estate deal, 4.25 is a number that defines the cost of capital and the potential for wealth creation. By translating this fraction into a decimal, you gain the clarity needed to navigate the complexities of the modern financial landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.