In the world of personal finance and investment, precision is the bedrock of success. While we are often introduced to numbers through simple fractions in primary education, the professional world of “Money” operates almost exclusively on decimals and percentages. When someone asks, “what is 1/4 into a decimal,” the immediate mathematical answer is 0.25. However, in the context of your bank account, your investment portfolio, or the global economy, 0.25 represents far more than a simple division of one by four. It represents 25 percent—a quarter of a whole—that can dictate the trajectory of interest rates, profit margins, and dividend yields.

Understanding how to transition between fractions and decimals is the first step in mastering financial tools. Whether you are calculating the interest on a high-yield savings account or determining the commission on a stock trade, the ability to view 1/4 as 0.25 allows for more sophisticated financial modeling and better decision-making.

The Mathematical Foundation of Financial Precision

Before diving into complex market strategies, one must understand why the decimal form of a fraction is the preferred language of finance. Fractions like 1/4 are conceptual; they represent a piece of a pie. Decimals like 0.25 are computational; they represent a specific value that can be easily multiplied, added, and integrated into software algorithms.

The Mechanics of Conversion

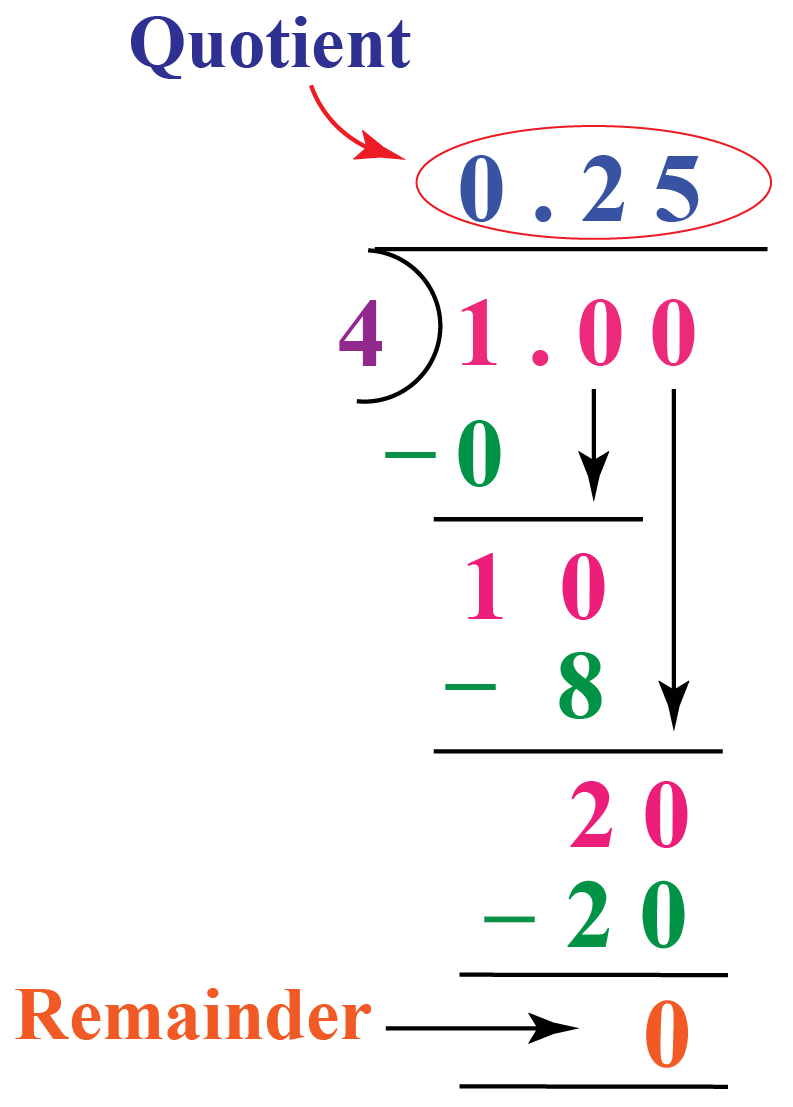

To convert the fraction 1/4 into a decimal, you simply divide the numerator (1) by the denominator (4). Because 1 cannot be divided by 4 as a whole number, we use a decimal point and add zeros, making it 1.00 divided by 4, which equals 0.25. In financial terms, this is the equivalent of saying that for every dollar, 1/4 represents 25 cents. While this seems elementary, this conversion is the basis for calculating “basis points”—the standard unit of measure for interest rates and bond yields.

Why Decimals Dominate Modern Finance

In the era of algorithmic trading and digital banking, decimals allow for infinite granularity. In the past, stock prices were actually quoted in fractions (e.g., a stock might be trading at 10 1/4). However, the financial industry moved to “decimalization” in the early 2000s. This shift from 1/4 to 0.25 allowed for narrower “spreads” (the difference between the buying and selling price), saving investors billions of dollars in transaction costs. By understanding 1/4 as 0.25, you are aligning your mental framework with the modern digital economy.

Interest Rates and the “Quarter-Point” Movement

Perhaps the most significant application of the 1/4 decimal conversion is found in central banking. When the Federal Reserve or other central banks discuss changing interest rates, they almost always move in increments of a “quarter-point.”

Understanding 25 Basis Points

In financial jargon, 1% is equal to 100 basis points. Therefore, 1/4 of a percentage point is 0.25%, or 25 basis points. When you hear a news report stating that the Fed has raised rates by a quarter-point, they are increasing the cost of borrowing by 0.25. This seemingly small decimal shift has a massive ripple effect on the economy. It changes the interest rate on your credit card, the monthly payment on your adjustable-rate mortgage, and the yield on your government bonds.

The Impact on Debt and Mortgages

For a homeowner with a $400,000 mortgage, a difference of 1/4 (0.25) in an interest rate can mean tens of thousands of dollars over the life of a 30-year loan. By converting that fraction into a decimal, you can use financial calculators to see the real-world impact. Professional financial planning requires looking past the fraction to the decimal reality: a 6.25% interest rate vs. a 6.50% interest rate is the difference between financial freedom and prolonged debt.

Investment Ratios and Portfolio Management

In the realm of investing, the number 0.25 (or 1/4) appears frequently in asset allocation and dividend distributions. Successful investors use these decimals to maintain balance and ensure their risk is managed effectively.

The “Quarterly” Dividend Cycle

Most publicly traded companies in the United States pay dividends on a quarterly basis—four times a year. Each payment represents 1/4 of the total annual dividend yield. If a stock has an annual yield of 4%, each quarterly payment is 1% (or 0.01 in decimal form). However, if you are calculating the “payout ratio” (the proportion of earnings paid out as dividends), seeing that a company pays out 1/4 of its earnings (0.25) tells you that the company is retaining 75% of its profits for future growth. This decimal insight helps an investor determine if a dividend is sustainable.

Asset Allocation: The 25% Rule

Many financial advisors suggest a diversified portfolio divided into four main categories: Domestic Stocks, International Stocks, Bonds, and Cash equivalents. In this “Four-Pillar” strategy, each category holds 1/4 of the total value. By viewing this as 0.25 of your total net worth, you can easily rebalance your portfolio. If your domestic stocks grow and now represent 0.30 (30%) of your portfolio, you know you must sell 0.05 (5%) to return to your target 0.25 (25%) allocation. This mathematical discipline is what separates emotional “gamblers” from professional wealth managers.

Business Finance: Profit Margins and Scalability

For entrepreneurs and small business owners, converting 1/4 into 0.25 is essential for understanding the health of a business. Profit margins are rarely discussed in fractions; they are analyzed as decimals to ensure accuracy in scaling.

Calculating Gross Profit Margins

If it costs a business $75 to produce a product that sells for $100, the profit is $25. As a fraction of the total revenue, that is 25/100, or 1/4. In a professional business report, this is expressed as a 0.25 gross margin (or 25%). Business owners must monitor this decimal closely. If rising supply chain costs reduce that 0.25 margin to 0.20, the business has lost 20% of its profitability, even if the total sales volume remains the same.

The Importance of the 25% Buffer

In business budgeting, it is a common “rule of thumb” to set aside 1/4 of your gross income for taxes and emergency overhead. By mentally converting 1/4 into 0.25, a business owner can automate their finances. For every dollar that enters the business account, 0.25 is immediately moved to a high-yield tax savings account. This decimal-based automation prevents the common “cash flow crunch” that sinks most startups in their first three years.

Tools and Strategies for Financial Conversion

To truly master the transition from 1/4 to 0.25 in a financial context, one must utilize the right digital tools. In the modern age, we no longer need to do long division by hand, but we do need to know how to input these values into software.

Spreadsheets and Formula Logic

In programs like Microsoft Excel or Google Sheets, entering “1/4” might sometimes be interpreted as a date (January 4th). To use this value for financial modeling, you must format the cell as a “Number” or “Percentage,” which automatically displays the decimal 0.25. Professional financial analysts use formulas like =1/4 to ensure that their spreadsheets remain dynamic. If a stake in a company changes from 1/4 to 1/5, the decimal updates from 0.25 to 0.20, instantly recalculating the entire sheet’s projected earnings.

Leveraging Financial Calculators

Whether you are using a mortgage calculator or a compound interest tool, these engines require decimal inputs. If a loan offers a “quarter-point discount,” you cannot type “1/4” into the software; you must understand it as 0.25. Mastering this simple conversion allows you to shop for the best financial products with confidence, ensuring you are not misled by marketing jargon that hides the true decimal cost of a loan or investment fee.

Conclusion: Why 0.25 is the Key to Wealth

While the question “what is 1/4 into a decimal” may seem like a simple math problem, its applications in the world of money are profound. To be financially literate is to be comfortable with decimals. 0.25 is the heartbeat of the quarterly earning season, the standard increment of Federal Reserve policy, and the baseline for a well-diversified portfolio.

By moving away from the abstract world of fractions and embracing the precise world of decimals, you gain a clearer view of your financial health. You begin to see that a 0.25% fee on a mutual fund isn’t “just a fraction”—it’s a significant portion of your future wealth. You realize that a 1/4 increase in your savings rate (from 0.00 to 0.25 of your income) can shorten your path to retirement by decades. In finance, every decimal point counts, and 0.25 is one of the most powerful numbers in your arsenal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.