The closure of a bank account, whether initiated by the customer or the institution, is a significant financial event. While it can sometimes be a deliberate choice to consolidate finances or move to a better institution, it can also be an unexpected and unsettling experience when a bank decides to terminate the relationship. Understanding the implications, processes, and potential consequences is crucial for navigating this situation smoothly and safeguarding your financial well-being. This article delves into the multifaceted realities of bank account closures, focusing specifically on the financial ramifications and the practical steps involved.

Understanding the Reasons Behind Account Closure

Banks, like any business, have policies and criteria that govern their relationships with customers. While a customer can typically close an account with relative ease, the situation becomes more complex when the bank initiates the closure. This is rarely an arbitrary decision and is usually driven by specific triggers designed to mitigate risk for the institution.

Bank-Initiated Closures: Common Triggers

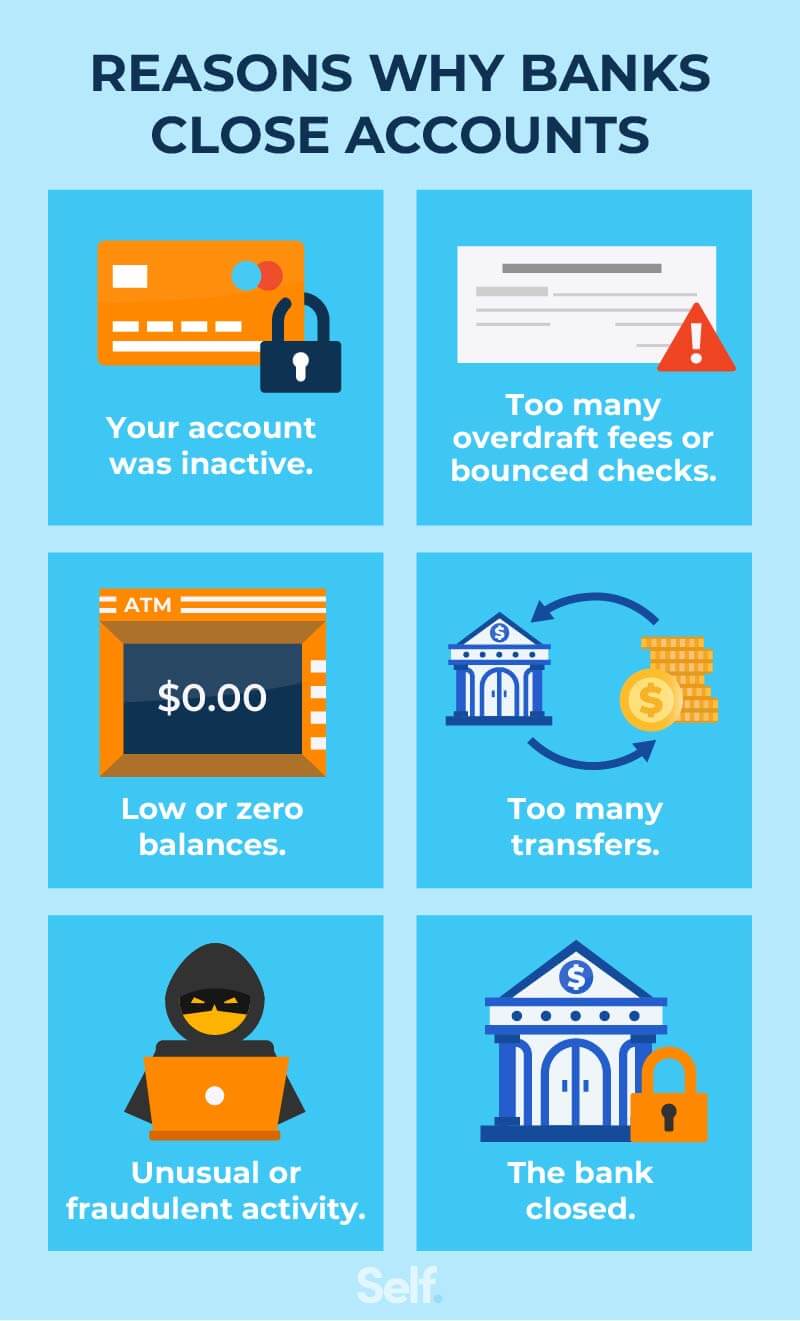

When a bank decides to close an account, it’s typically for reasons that signal a heightened risk or violation of the bank’s terms of service. These reasons can broadly be categorized into several key areas:

- High-Risk Activity: Banks are obligated to monitor transactions for suspicious patterns that could indicate illegal activities, such as money laundering or fraud. Unusually large or frequent international transfers, a sudden influx of cash from unknown sources, or multiple transactions that resemble structuring (breaking down large sums into smaller ones to avoid reporting thresholds) can all raise red flags. While innocent customers might engage in such activities due to legitimate reasons, banks often err on the side of caution.

- Negative Balance and Overdrafts: Consistently maintaining a negative balance or frequently incurring overdraft fees without prompt resolution can lead to account closure. This indicates a lack of financial responsibility and a potential burden on the bank due to the costs associated with managing delinquent accounts. While occasional, small overdrafts might be tolerated, a pattern of such behavior is a strong indicator for closure.

- Suspicious or Fraudulent Activity: If a bank suspects your account is being used for fraudulent purposes, either by you or by someone else who has gained unauthorized access, they may close it to prevent further losses. This can include being on a list of individuals or entities associated with financial crimes, or if your account is linked to a fraudulent transaction originating elsewhere.

- Non-Compliance with Terms of Service: Every bank has a set of terms and conditions that customers agree to when opening an account. Violating these terms, even unintentionally, can lead to closure. This might include providing false information during the application process, engaging in activities explicitly prohibited by the bank (e.g., using the account for certain business purposes without disclosure), or failing to update essential personal information.

- Dormancy and Inactivity: While less common as a sole reason for closure, accounts that remain inactive for extended periods can sometimes be closed, particularly if they have a negative balance due to accumulated fees. Banks incur costs for maintaining accounts, and dormant accounts represent a liability without any benefit. They may also be closed to comply with regulations regarding unclaimed property.

- Legal or Regulatory Requirements: In some instances, a bank may be compelled to close an account due to legal orders, sanctions, or regulatory changes. This could involve accounts associated with individuals or entities on watchlists, or if the nature of the account holder’s activities falls outside permissible regulations.

Customer-Initiated Closures: Strategic Financial Decisions

On the other hand, customers choose to close accounts for a variety of proactive financial management reasons. These closures are typically planned and executed with a clear objective in mind.

- Seeking Better Products or Services: The financial landscape is constantly evolving, with new banks and credit unions emerging and existing ones revamping their offerings. Customers may close accounts to switch to an institution that provides more competitive interest rates, lower fees, better online banking tools, or more convenient branch locations.

- Consolidating Finances: Many individuals find themselves with multiple accounts across different institutions. Closing redundant accounts and consolidating their banking activities with one or a few trusted providers can simplify financial management, reduce the number of statements to track, and potentially qualify for better relationship benefits.

- Reducing Fees and Costs: Some bank accounts come with monthly maintenance fees, ATM fees, or other charges that can add up. If these fees are not offset by benefits or minimum balance requirements, customers may opt to close these accounts and move to fee-free alternatives.

- Simplifying Financial Life: For individuals whose financial needs are becoming simpler, or who are downsizing their assets, maintaining a complex web of accounts may become burdensome. Closing unnecessary accounts can declutter their financial life.

- Personal Circumstances: Major life events, such as moving to a new country, a significant change in income, or the need to divest from certain financial entities, can also prompt account closures.

The Process of Account Closure: What to Expect

The mechanics of account closure can differ slightly depending on whether the bank or the customer initiates it, but the general steps involve ensuring all outstanding obligations are settled and distributing any remaining funds.

Bank-Initiated Closure Procedures

When a bank decides to close an account, they are generally required to provide a notice to the account holder. This notice serves as a formal communication of their decision and outlines the timeframe for closure.

- Notification Period: Banks typically provide a grace period, often 30 to 60 days, before closing the account. This allows the customer time to make alternative arrangements and transfer funds. The exact notice period can vary based on the bank’s policy and the specific reason for closure.

- Settlement of Obligations: Before the account can be formally closed, any outstanding balances, including negative balances, accrued fees, or pending transactions, must be settled. If the account has a negative balance, the bank will expect the customer to deposit sufficient funds to cover the deficit. Failure to do so can have further financial repercussions.

- Fund Distribution: If there are funds remaining in the account, the bank will typically issue a check for the balance, or, if arrangements are made, transfer the funds to another account. It’s crucial to provide the bank with a correct mailing address to ensure you receive your funds promptly.

- Reporting to Credit Bureaus (Indirect Impact): While banks don’t directly report account closures to credit bureaus in the same way they report delinquencies, a bank-initiated closure, especially if due to negative balances or unresolved debts, can indirectly affect your creditworthiness. If the bank has to send the outstanding debt to a collection agency, this will certainly be reported.

Customer-Initiated Closure Procedures

Closing an account as a customer is generally a more straightforward process, designed for customer convenience.

- Clearing Outstanding Transactions: It’s essential to ensure all pending checks have cleared, automatic payments have been rerouted, and any outstanding debit card transactions have been finalized. Closing an account with pending transactions can lead to bounced checks and further complications.

- Settling Any Balances: If there is a negative balance, you will need to deposit funds to clear it. If there’s a positive balance, you can choose to withdraw the cash, receive a cashier’s check, or transfer the funds to another account.

- Formal Request: Customers typically need to formally request the account closure. This can often be done in person at a branch, over the phone, or sometimes through secure messaging within the bank’s online portal. You may be asked to fill out a form and provide identification.

- Confirmation of Closure: Always request written confirmation from the bank that your account has been closed. This document can be vital for record-keeping and resolving any potential future discrepancies.

The Financial Repercussions and Next Steps

The closure of a bank account, particularly an unexpected one, can have significant financial implications that extend beyond simply losing access to your funds. Proactive management and understanding these consequences are vital.

Immediate Financial Disruptions

- Access to Funds: The most immediate impact is the loss of direct access to the funds in the closed account. If the closure is sudden and unexpected, it can leave you without readily available cash for daily expenses. This can lead to a cascade of problems, including inability to pay bills, purchase necessities, or cover emergency expenses.

- Impact on Automatic Payments and Direct Deposits: All automatic bill payments, subscriptions, and direct deposits (like your salary) linked to the closed account will cease to function. This can result in late payment fees, service disruptions, and missed income. It’s crucial to immediately update your banking information with any entities that send you money or withdraw funds from your account.

- Overdraft and Penalty Fees: If the closure is due to a negative balance, the bank may continue to accrue overdraft fees and other penalties until the balance is settled. Furthermore, if the debt remains unpaid, it could be sent to a collection agency, incurring additional fees and negatively impacting your credit score.

Long-Term Financial Implications

- Credit Score Impact: While banks don’t typically report the act of closing an account itself to credit bureaus, a closure resulting from negative balances, defaulted debts, or involvement in fraudulent activities can lead to severe credit damage. A collection account or a judgment against you from the bank for an outstanding debt will be a significant negative mark on your credit report, making it harder to obtain loans, credit cards, or even rent an apartment in the future.

- Difficulty Opening New Accounts: Banks often share information about customers whose accounts have been closed, particularly for problematic reasons. If your account was closed by the bank due to high-risk activity, frequent overdrafts, or suspected fraud, you may find it difficult to open an account with other financial institutions. This is often managed through a shared database like ChexSystems, which tracks account closure information.

- Finding a New Banking Relationship: Being flagged in systems like ChexSystems can present a significant hurdle in establishing a new banking relationship. You might need to opt for “second chance” banking accounts, which often come with higher fees and stricter monitoring, or explore credit unions that may have more lenient policies.

Steps to Take After an Account Closure

Regardless of who initiated the closure, certain steps are essential to mitigate the damage and re-establish financial stability.

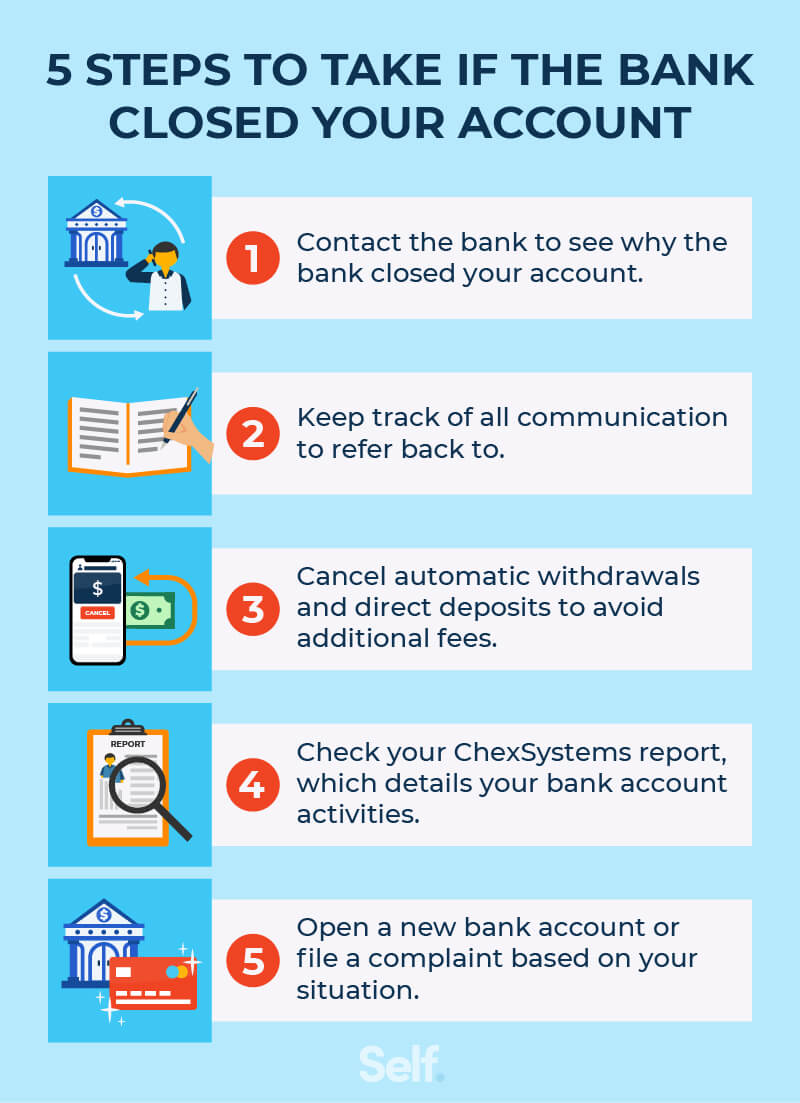

- Understand the Reason: If the closure was bank-initiated, try to understand the specific reason. Request a written explanation if one wasn’t provided with the initial notification. This understanding is key to addressing the root cause and preventing future issues.

- Settle Any Outstanding Balances: This is paramount. Work with the bank to clear any negative balances and accumulated fees. Ignoring this will lead to further financial penalties and credit damage.

- Redirect Automatic Payments and Direct Deposits: Immediately update your banking information with your employer, utility companies, subscription services, and any other entity that sends or receives payments from your account. This prevents missed payments and potential late fees.

- Monitor Your Credit Report: Regularly check your credit report for any inaccuracies or new negative entries that may have resulted from the account closure, especially if the debt was sent to collections.

- Seek a New Banking Relationship: If you need a new bank account, research institutions that offer second-chance accounts or have more flexible approval processes. Be prepared to explain the circumstances of your previous account closure, if necessary.

- Review Your Financial Habits: If the closure was due to your own financial management issues (e.g., overdrafts), take this as an opportunity to review your spending habits, create a budget, and implement strategies to improve your financial discipline.

The closure of a bank account is a serious financial event that can have lasting consequences if not handled correctly. By understanding the potential reasons, the procedural steps, and the subsequent financial ramifications, individuals can navigate this challenge more effectively and work towards restoring their financial health and re-establishing a secure banking relationship.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.