When it comes to personal finance, few tools are as misunderstood yet as powerful as the Health Savings Account (HSA). Often overshadowed by more traditional retirement vehicles like the 401(k) or the Roth IRA, the HSA is frequently viewed merely as a way to pay for current doctor’s visits or prescriptions. This narrow view leads many to a common anxiety: the fear that any money left in the account at the end of the year will simply vanish.

If you have ever asked, “What happens to unused HSA funds?” the short answer is: they stay exactly where they are. Unlike the Flexible Spending Account (FSA), which is notorious for its “use it or lose it” provision, the HSA is a permanent financial asset. Understanding how these unused funds behave—and how they can be leveraged—is a cornerstone of sophisticated personal finance management.

The Perpetuity of HSA Capital: Why Your Balance Never Expires

The most significant advantage of an HSA is that the account holder owns the funds in perpetuity. There is no expiration date on the capital you contribute. Whether you leave the money in the account for twelve months or forty years, it remains yours until you choose to spend it.

The Myth of “Use It or Lose It”

Many employees confuse the HSA with the FSA. In an FSA, the IRS generally requires that funds be spent within the plan year, with only minor “carryover” or “grace period” exceptions. The HSA is governed by entirely different tax codes. Because an HSA is a private custodial account (similar to an IRA), the balance automatically rolls over from year to year. This makes the HSA a “long-term” vehicle rather than a “current-year” budget tool.

Portability and Job Transitions

Another critical aspect of unused HSA funds is portability. Because the money belongs to the individual and not the employer, the funds stay with you even if you change jobs, retire, or leave the workforce entirely. If you have built up a balance of $10,000 in unused funds and decide to pivot to a new career, that money follows you. You can even choose to move the funds to a different HSA provider through a trustee-to-trustee transfer to seek lower fees or better investment options.

The Triple Tax Advantage: Turning Unused Funds into Wealth

To understand why keeping unused funds in an HSA is a brilliant financial move, one must understand the “triple tax advantage.” In the world of money management, this is the “Holy Grail” of tax efficiency, outperforming even the standard 401(k).

Tax-Deductible Contributions

Every dollar you contribute to an HSA reduces your taxable income for the year. If you contribute the maximum allowed by the IRS, you are effectively lowering your tax bill while building a liquid reserve for health costs. For those who contribute through payroll deductions, these funds often also escape FICA taxes (Social Security and Medicare), providing an immediate savings of roughly 7.65% before the money is even invested.

Tax-Free Growth and Earnings

This is where “unused” funds become powerful. When you don’t spend your HSA balance, you can invest it in the financial markets. Most HSA providers allow users to invest their balance in stocks, bonds, and mutual funds once they hit a minimum threshold (often $1,000). Any interest, dividends, or capital gains earned within the account are 100% tax-free. Over decades, this tax-free compounding can turn a modest health fund into a significant six-figure asset.

Tax-Free Withdrawals for Medical Expenses

The final leg of the triple tax advantage is the withdrawal. When you use your HSA funds for qualified medical expenses—ranging from surgery and dental work to contact lenses and physical therapy—the withdrawal is not taxed. Unlike a 401(k), where you pay taxes upon withdrawal, or a Roth IRA, where you contribute after-tax dollars, the HSA allows you to bypass taxes at every single stage of the process, provided the funds are used for health-related costs.

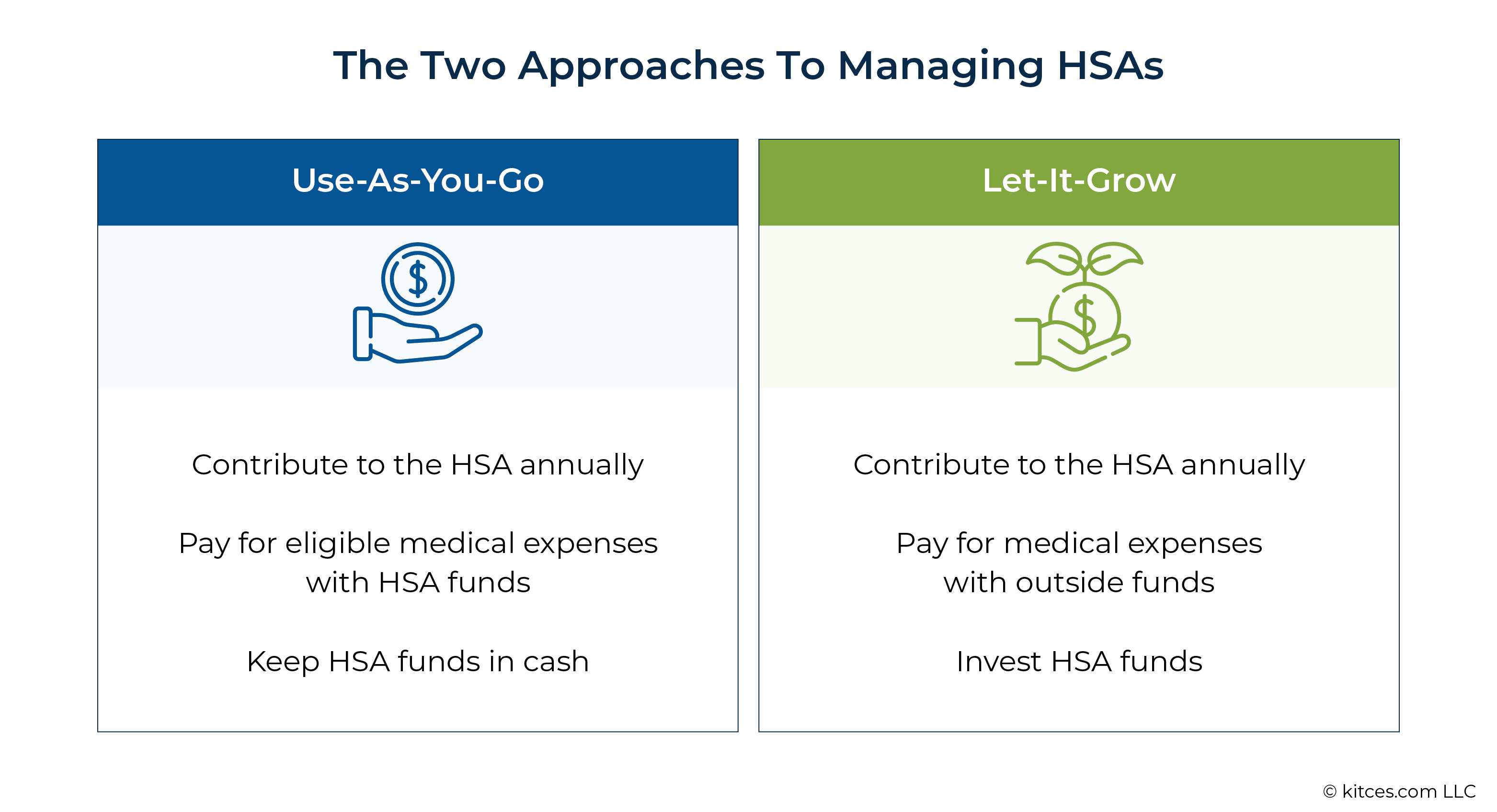

Strategic Long-Term Management: The “Stealth IRA” Strategy

For those who have the financial stability to pay for current out-of-pocket medical expenses using their regular income, the HSA evolves into what financial planners call a “Stealth IRA.” By intentionally leaving HSA funds unused for decades, you create a powerhouse retirement account.

The “Shoebox” Reimbursement Method

The IRS currently has no deadline for when you must reimburse yourself for a medical expense. This is a massive loophole for savvy investors. If you incur a $2,000 medical bill today, you can pay for it out of your checking account, save the receipt (electronically or in a “shoebox”), and leave $2,000 in your HSA to grow. Twenty years from now, you can “reimburse” yourself for that $2,000 expense. By then, that $2,000 might have grown to $8,000 through market investments. You take your $2,000 tax-free, and the remaining $6,000 stays in the account to continue growing.

Transitions After Age 65

What happens if you reach retirement age and you are remarkably healthy, leaving you with a massive surplus of unused HSA funds? Once you reach age 65, the HSA becomes even more flexible. While you can always continue to use the funds tax-free for medical expenses (including Medicare premiums), you also gain the ability to withdraw funds for non-medical purposes without the 20% penalty. In this scenario, the funds are simply taxed as ordinary income—identical to how a traditional IRA or 401(k) works. This effectively removes the “risk” of over-contributing to an HSA.

Protecting Your Unused Funds: Compliance and Common Pitfalls

While the HSA is an incredible tool, managing unused funds requires a disciplined approach to IRS regulations. Failing to follow the rules can lead to hefty penalties that erode your financial gains.

Maintaining Documentation for Future Audits

As mentioned with the “shoebox strategy,” the burden of proof lies with the taxpayer. If you plan to leave funds unused for years and then reimburse yourself later, you must maintain impeccable records. This includes EOBs (Explanation of Benefits), invoices, and proof of payment. If the IRS audits you ten years from now, you must be able to prove that the withdrawal you took was for a qualified expense incurred after the HSA was established.

Understanding the 20% Penalty

Before age 65, if you use your “unused” funds for a non-qualified expense—such as a vacation or a new car—you will be hit with a double blow: the withdrawal will be taxed as ordinary income, and you will be assessed a 20% penalty. This is significantly higher than the 10% penalty associated with early withdrawals from an IRA. Therefore, it is vital to treat the HSA as a restricted asset until either a medical need arises or you reach the age of 65.

Beneficiary Designations and Estate Planning

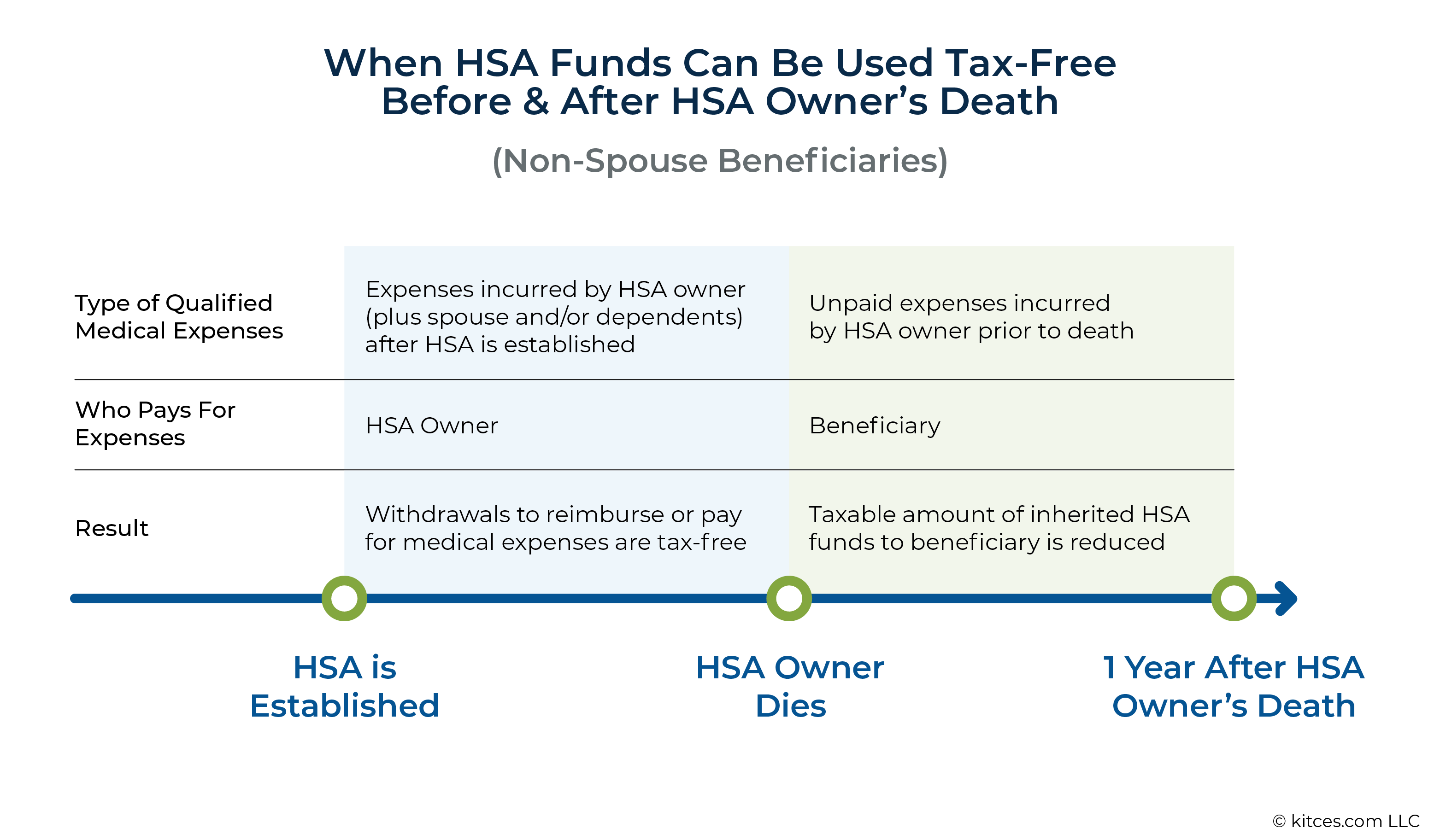

What happens to unused HSA funds if the account holder passes away? This is a critical “Money” topic for estate planning. If your spouse is the named beneficiary, the account becomes their HSA, and the tax advantages continue seamlessly. However, if the beneficiary is anyone other than a spouse (like a child or a sibling), the account ceases to be an HSA. The fair market value of the account becomes taxable to the beneficiary in the year of death. Strategic planning is required to ensure that your unused wealth is transferred as efficiently as possible.

Conclusion: The Financial Power of Doing Nothing

In many areas of personal finance, “unused” capital is seen as a sign of inefficiency. However, in the context of a Health Savings Account, unused funds are a signal of strategic wealth building. By allowing these funds to roll over, you aren’t just saving for a rainy day at the doctor’s office; you are participating in one of the most tax-efficient investment strategies allowed by law.

Whether you view your HSA as a high-yield emergency fund for healthcare or as a primary pillar of your retirement strategy, the message is clear: do not fear the rollover. Every dollar left unused today is a dollar that can be invested, grown, and utilized to provide financial security in the future. By mastering the mechanics of the HSA, you transform a simple healthcare account into a sophisticated engine for long-term financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.