Recessions are periods of significant economic contraction, marked by declines in GDP, rising unemployment, and reduced consumer spending. Their impact ripples through nearly every sector of the economy, and the housing market is no exception. However, the relationship between a recession and housing prices is not always straightforward or uniform. While a downturn generally implies downward pressure, the extent and nature of that pressure can vary dramatically based on the recession’s root causes, market fundamentals, and policy responses. Understanding this dynamic is crucial for homeowners, prospective buyers, and real estate investors alike, as it directly impacts personal wealth and investment strategies.

The Interplay of Recessions and Real Estate Dynamics

The health of the housing market is deeply intertwined with broader economic conditions. When the economy falters, several key mechanisms come into play that can influence home values.

Economic Downturns and Consumer Behavior

A recession typically leads to job losses or reduced income security for many households. This immediate financial pressure directly impacts the demand side of the housing market. Potential buyers, facing uncertain job prospects or diminished savings, become more cautious. They may postpone major financial commitments like purchasing a home, leading to a decrease in buyer activity. For current homeowners, reduced income can make mortgage payments more challenging, potentially increasing the risk of default and forced sales, which add to housing supply. Consumer confidence, a critical driver of big-ticket purchases, also plummets during a recession, further dampening demand. People tend to save more and spend less when the economic future is cloudy, shifting priorities away from homeownership or upgrading existing homes.

Interest Rates and Mortgage Affordability

Central banks often respond to recessions by cutting interest rates to stimulate economic activity. Lower interest rates typically translate into lower mortgage rates, which can, in theory, make housing more affordable and boost demand. However, this effect is often mitigated during a recession by other factors. Even with lower rates, stricter lending standards – a common reaction from banks during times of economic uncertainty – can make it harder for potential buyers to qualify for loans. Furthermore, the psychological impact of a recession, coupled with job insecurity, can override the incentive of lower mortgage payments. While lower rates might support a floor for prices or prevent a steeper decline, they rarely act as a silver bullet to ignite a housing boom during a recessionary period. The net effect on housing prices depends on whether the increased affordability outweighs the diminished willingness and ability to borrow.

Employment, Income, and Foreclosures

The most direct link between a recession and housing prices often stems from employment and income. Mass layoffs and stagnant wages reduce the pool of qualified buyers and weaken the financial standing of current homeowners. As unemployment rises, so does the risk of mortgage delinquencies and foreclosures. An increase in foreclosed properties can flood the market with distressed sales, which often go for lower prices. These lower-priced sales then drag down the comparable sales (comps) for other homes in the area, putting downward pressure on overall housing values. The severity of job losses and the duration of unemployment are critical determinants of how deeply and broadly housing prices might fall. Government programs, such as unemployment benefits or mortgage forbearance initiatives, can help buffer some of these impacts, but their effectiveness can vary.

A Look Back: Historical Housing Market Responses to Recessions

History provides valuable context, but it also reveals that not all recessions are created equal, particularly concerning their impact on real estate.

The Subprime Crisis of 2008: A Unique Case

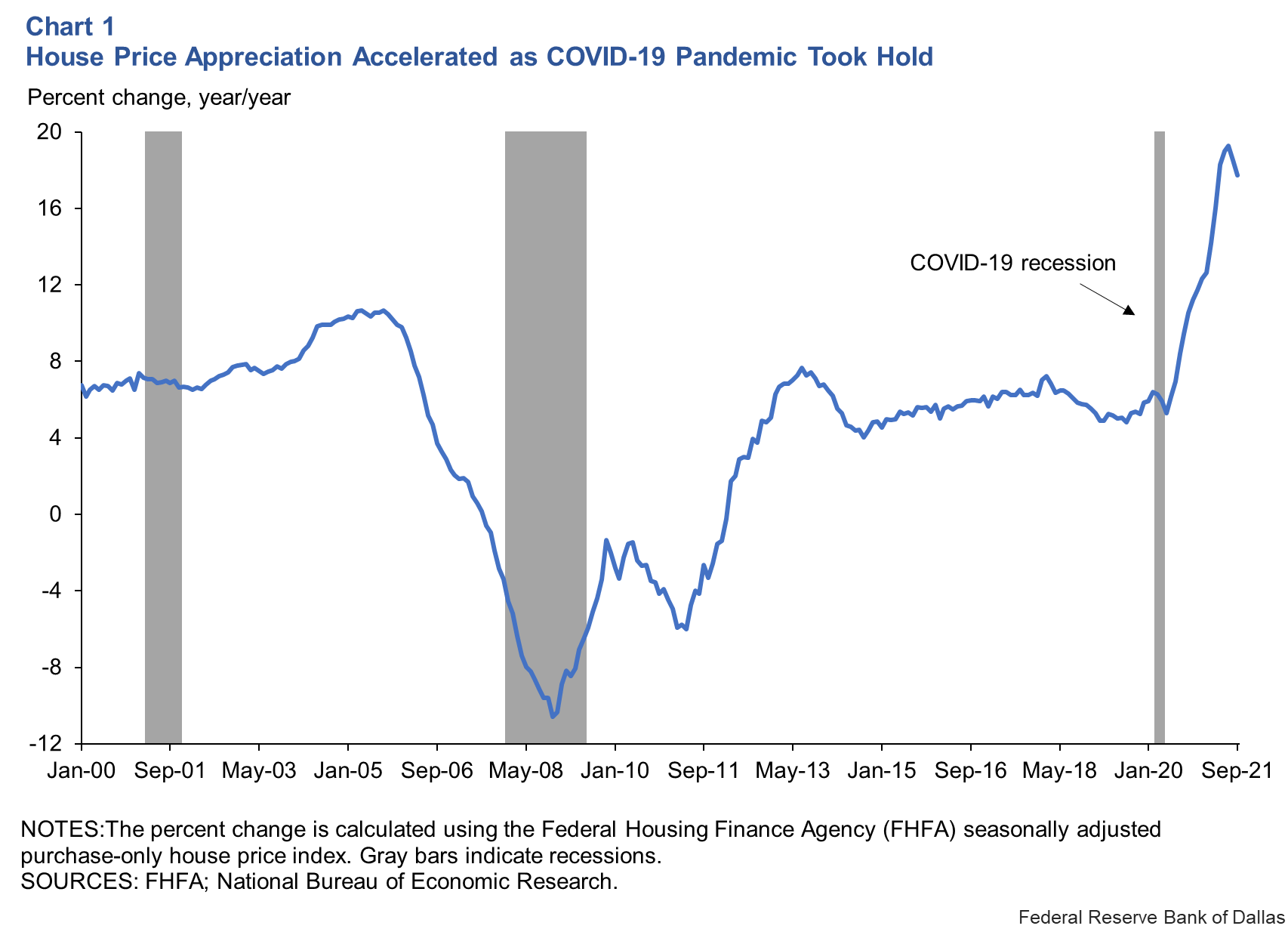

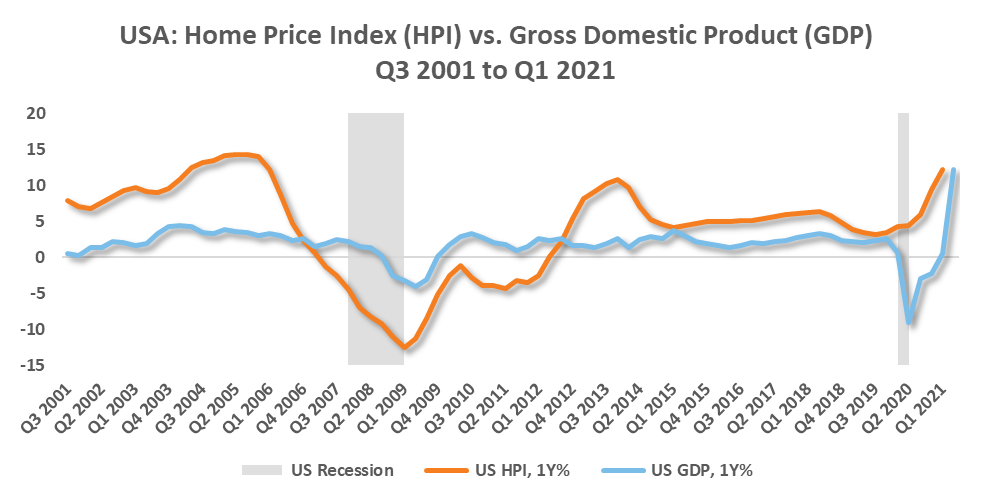

The Great Recession of 2008-2009 stands out as a housing-led crisis. It was unique because it originated from systemic failures within the mortgage and financial markets, specifically the proliferation of subprime loans and speculative lending practices. During this period, housing prices saw steep, widespread declines across the United States, with some areas experiencing drops of 30-50%. Foreclosures skyrocketed, and the housing market became a primary driver of the broader economic meltdown. This experience solidified a popular perception that recessions automatically lead to significant housing price crashes. However, this particular recession was an anomaly in terms of its origin and the magnitude of its impact on housing.

Other Recessions: Varied Outcomes

Looking at other recessions reveals a more nuanced picture. For instance:

- Early 1990s Recession (1990-1991): Triggered by a credit crunch and the Gulf War, this recession saw housing prices flatten or decline modestly in some regions, but certainly not a national crash comparable to 2008. The average national home price saw a mild dip and recovered relatively quickly.

- Dot-Com Bust (2001): This tech-bubble recession had a minimal impact on housing prices. In fact, many areas saw continued appreciation, partly due to falling interest rates that spurred housing demand even as the stock market corrected. The national housing market actually grew stronger through the early 2000s, setting the stage for the later boom.

- COVID-19 Recession (2020): This extremely short, sharp recession, caused by a global pandemic and subsequent lockdowns, was initially expected to crush housing. However, massive fiscal stimulus, historically low interest rates, and a shift in housing preferences (desire for more space, remote work) led to an unprecedented housing boom shortly after the initial shock. This defied many predictions, highlighting the complex interplay of factors beyond just economic contraction.

These examples underscore that a recession’s cause, duration, and the policy responses to it are critical in determining how housing prices react. Not every recession sees housing prices plummet; sometimes, they merely flatten, experience a modest correction, or even continue to rise if other supportive factors are present.

Regional Disparities and Local Market Nuances

It’s also vital to remember that “the housing market” is not a single, monolithic entity. Real estate is inherently local. During a national recession, some regions may experience significant price declines, while others remain relatively stable or even continue to see modest growth. Factors influencing these regional disparities include:

- Local Economic Drivers: Regions heavily reliant on industries particularly vulnerable to recession (e.g., manufacturing during certain downturns) may see greater job losses and thus more significant housing market impacts. Diversified economies tend to be more resilient.

- Supply and Demand Imbalances: Markets with chronic housing shortages tend to be more resistant to price drops, as demand continues to outstrip supply even in a downturn. Conversely, areas with an oversupply of homes are more vulnerable.

- Affordability: Markets that were already unaffordable prior to a recession may be more susceptible to corrections, as even minor economic shifts can push homeownership out of reach for a larger segment of the population.

- Migration Patterns: Population shifts, often influenced by economic opportunity, can strengthen or weaken local housing demand regardless of national trends.

Factors Determining Housing Market Resilience (or Vulnerability)

Beyond the immediate mechanics of a recession, several structural and policy factors can influence how resilient a housing market proves to be.

Supply and Demand Fundamentals

The core economic principle of supply and demand remains paramount. Markets with a severe and persistent undersupply of housing units—a common issue in many major metropolitan areas over the past decade—tend to be more resistant to price declines, even during a recession. The fundamental need for housing persists, and if there aren’t enough homes to go around, prices may hold steady or experience only minor adjustments. Conversely, markets with an oversupply, or those where new construction outpaced demand leading up to the recession, are more vulnerable to price corrections as supply quickly overwhelms reduced demand.

Mortgage Lending Standards and Buyer Qualifications

The rigor of mortgage lending standards plays a critical role. Leading up to the 2008 crisis, lax lending standards allowed many unqualified borrowers to obtain mortgages, creating an artificial demand bubble that burst when these loans inevitably failed. In contrast, post-2008 regulations generally led to much stricter underwriting criteria, ensuring that borrowers are more financially stable and less likely to default en masse during a downturn. When current homeowners have significant equity and responsible loans, the likelihood of widespread foreclosures that depress prices is significantly reduced.

Government Intervention and Stimulus Measures

Government responses to recessions can significantly alter the housing market’s trajectory. Fiscal stimulus packages, such as direct payments to citizens or enhanced unemployment benefits, can help maintain household incomes, supporting mortgage payments and overall housing demand. Monetary policy, including interest rate cuts and quantitative easing, aims to lower borrowing costs and inject liquidity into the financial system. Additionally, specific housing-related policies, such as mortgage forbearance programs (as seen during COVID-19), can temporarily prevent foreclosures, stabilizing the market during acute crises. The scale and timing of these interventions are crucial.

Demographic Shifts and Migration Patterns

Long-term demographic trends can act as powerful undercurrents. For example, a large cohort of millennials reaching peak homebuying age can provide consistent demand, even in the face of economic headwinds. Similarly, population growth in certain regions due to job creation or quality of life factors can maintain housing demand. Conversely, regions experiencing population decline or significant outward migration may see their housing markets weaken regardless of the national economic picture. The remote work phenomenon, accelerated by the pandemic, has also shifted some demand from expensive urban cores to more affordable suburban and rural areas, influencing localized housing trends.

Navigating the Housing Market During a Downturn

Understanding how recessions affect housing prices is not just academic; it empowers individuals to make more informed financial decisions.

For Prospective Homebuyers: Opportunities and Cautions

A recession can present opportunities for homebuyers, especially if prices soften or inventory increases, leading to less competition. Lower interest rates, if available and coupled with accessible lending, can improve affordability. However, caution is paramount. Buyers should prioritize financial stability, ensure job security, and build a substantial emergency fund. Avoiding overleveraging is critical, as future economic uncertainty could make high mortgage payments untenable. It’s often wise to focus on buying a home that meets needs rather than trying to perfectly time the bottom of the market, which is notoriously difficult. A long-term perspective is key, recognizing that real estate cycles inevitably turn.

For Current Homeowners: Protecting Equity and Managing Risk

For those who already own a home, a recession primarily concerns protecting equity and managing financial risk. Maintaining a strong emergency fund to cover mortgage payments during potential job loss is crucial. If facing financial hardship, exploring options like mortgage forbearance or refinancing to a lower rate (if available) can provide relief. Investing in essential home maintenance can preserve value, but major, non-essential renovations might be best postponed if equity is tight or future economic prospects are uncertain. Homeowners with significant equity are generally in a more secure position, as they have a buffer against potential price declines.

For Real Estate Investors: Strategic Planning and Value Identification

Real estate investors often view recessions as potential buying opportunities. Distressed properties, motivated sellers, and less competition can lead to acquiring assets at a discount. However, this requires significant capital, a tolerance for risk, and a keen understanding of local market fundamentals. Identifying undervalued properties, understanding potential rental demand shifts, and having a clear exit strategy are critical. Investors should also focus on properties that are less sensitive to economic cycles, such as essential housing in stable job markets, rather than speculative or luxury properties. Due diligence on potential economic recovery scenarios and interest rate trajectories is more important than ever. Diversification within a real estate portfolio can also help mitigate risks associated with specific market segments or geographies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.