The intersection of mortality and finance is a subject many prefer to avoid, yet it is one of the most critical aspects of comprehensive financial planning. A common anxiety among those carrying a balance is the fear that their financial burdens will become a legacy of debt for their grieving loved ones. There is a persistent myth that credit card debt simply evaporates upon death, and an equally pervasive fear that children or spouses will be hounded by collectors to pay off balances they didn’t accrue.

The reality lies somewhere in the middle. While debt does not typically “inherit” in the way a house or a jewelry collection might, it does not disappear. Instead, it becomes a liability of the deceased person’s estate. Understanding the mechanics of how debt is handled after death is essential for protecting your heirs and ensuring your final wishes are executed without financial turmoil.

The Lifecycle of Debt After Death: Understanding the Estate Process

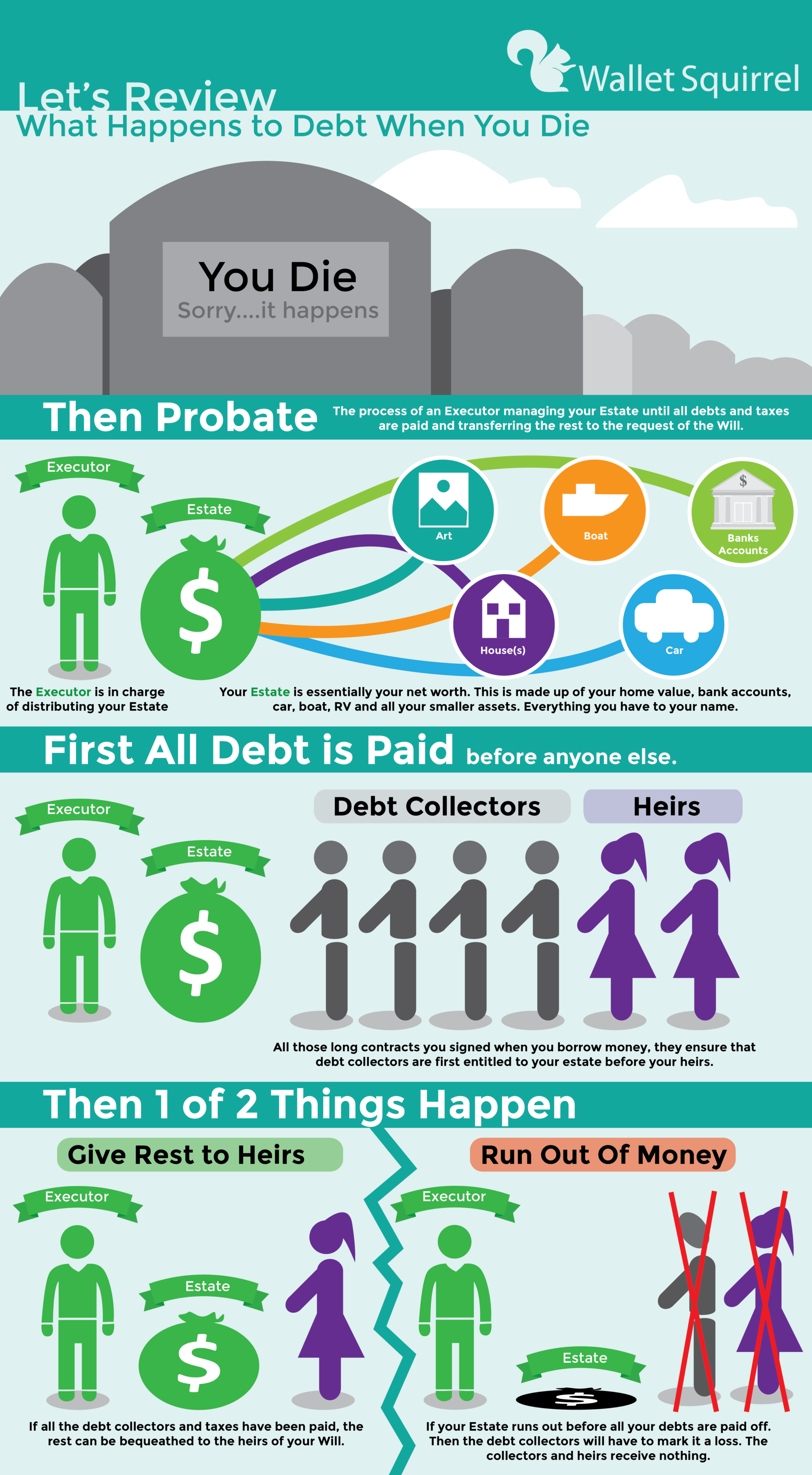

When a person passes away, everything they owned—from bank accounts and real estate to personal effects—collectively becomes known as their “estate.” Simultaneously, everything they owed becomes the responsibility of that estate. This transition is managed through a legal process known as probate, which is designed to ensure that creditors are paid before any assets are distributed to beneficiaries.

Defining the Estate and the Role of the Executor

The estate is a temporary legal entity created to bridge the gap between a person’s death and the final distribution of their assets. If the deceased left a will, they likely named an “executor” (or personal representative) to manage these affairs. If there is no will, a court appoints an administrator. The executor’s primary fiduciary duty is to settle the estate’s debts using the estate’s assets. This involves identifying all creditors, notifying them of the death, and determining the total value of the assets available to satisfy those claims.

The Probate Process: How Assets Meet Obligations

Probate is the court-supervised process of validating a will and overseeing the distribution of assets. During this time, the executor must take an inventory of all property. It is important to note that not all assets go through probate. Life insurance payouts, retirement accounts with named beneficiaries (like 401(k)s or IRAs), and “payable on death” (POD) bank accounts usually bypass probate and go directly to the beneficiaries. Because these assets aren’t part of the probate estate, they are often shielded from credit card companies looking for payment, unless the estate itself was named as the beneficiary.

The Hierarchy of Creditors: Where Credit Cards Rank

In the world of debt, not all liabilities are created equal. State laws dictate the order in which debts must be paid from the estate’s funds. Typically, the hierarchy begins with funeral expenses and the costs of administering the estate (including legal and executor fees). Next come taxes and secured debts, such as mortgages or auto loans, where the debt is tied to a specific piece of collateral.

Credit card debt is classified as “unsecured debt,” meaning it is not backed by an asset the bank can seize. Consequently, credit card companies usually sit at the bottom of the priority list. If an estate runs out of money after paying funeral costs and taxes, the credit card companies may simply be out of luck.

Are Heirs Responsible? Debunking Myths About Inherited Debt

The most pressing question for most families is whether survivors are personally responsible for paying off the deceased’s credit cards. In the vast majority of cases, the answer is a definitive “no.” You cannot inherit a debt simply by being related to the deceased. However, there are three significant exceptions to this rule that every family should understand.

General Rule: You Can’t Inherit Debt

Under federal law and the statutes of most states, heirs are not personally liable for the individual debts of the deceased. If your father dies with $20,000 in credit card debt and $5,000 in his bank account, the credit card company can take the $5,000, but they cannot legally demand the remaining $15,000 from you. Once the estate’s assets are exhausted, the remaining unsecured debt is typically written off by the creditor as uncollectible.

The Exception of Community Property States

The landscape changes significantly in “community property” states. In these jurisdictions—which include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin—most debts incurred by one spouse during the marriage are considered the joint responsibility of both spouses. If a person dies in one of these states with credit card debt, the surviving spouse may be held personally liable for that debt, even if their name was never on the account. This reflects the legal philosophy that assets and liabilities acquired during a marriage belong to the “community” of the couple.

Co-signers vs. Authorized Users: Knowing the Difference

It is vital to distinguish between a co-signer and an authorized user. An authorized user is someone who has permission to use a credit card but did not sign the original credit agreement. Authorized users are generally not responsible for the balance after the primary cardholder dies.

In contrast, a co-signer (or joint account holder) has signed a contract guaranteeing the debt. If you co-signed a credit card for a loved one, you are “jointly and severally” liable. This means that upon their death, the credit card company will look directly to you for the full balance, regardless of what is happening in the probate process.

When the Estate Is “Insolvent”: What Happens if There Isn’t Enough Money?

An “insolvent estate” occurs when the total value of the deceased’s assets is less than the total value of their debts. This is a common scenario, and it requires a specific legal protocol to ensure the executor does not inadvertently become liable for mishandling funds.

The Definition of an Insolvent Estate

When an estate is insolvent, the executor must follow state-mandated priority lists for payment. They cannot choose to pay a favorite credit card over a tax bill. If they distribute money to heirs before paying off legitimate creditors, the executor can be held personally liable for the “wrongful distribution.” In an insolvent estate, the heirs receive nothing, as every available dollar is funneled toward the creditors in their ranked order.

Protecting Exempt Assets: Life Insurance and Retirement Accounts

One of the most important aspects of financial planning is understanding “exempt assets.” In many states, certain assets are protected from creditors even if the estate is insolvent. Life insurance proceeds paid to a named beneficiary are almost always exempt from the deceased’s creditors. Similarly, retirement accounts like 401(k)s and IRAs usually pass directly to the beneficiary outside of the estate’s reach. This is why it is crucial to keep beneficiary designations up to date; if you name “my estate” as the beneficiary, those funds suddenly become available to satisfy credit card companies.

Dealing with Aggressive Debt Collectors

Unfortunately, some debt collection agencies may attempt to guilt or pressure survivors into paying debts they do not owe. They might suggest that “paying the balance is the right thing to do for your loved one’s legacy.” It is important to remember that unless you are a co-signer or live in a community property state, you have no legal obligation to pay. The Fair Debt Collection Practices Act (FDCPA) provides protections against harassment. If a collector contacts you, you have the right to refer them to the executor of the estate and request that they cease further personal contact.

Proactive Steps: Managing Your Legacy and Protecting Your Loved Ones

The best way to ensure that your credit card debt doesn’t create a headache for your family is to engage in proactive estate planning. While you cannot take your debt with you, you can take steps to ensure it is handled efficiently and that your heirs are protected.

The Importance of a Clear Will and Estate Plan

A well-drafted will does more than just distribute property; it provides a roadmap for the executor. By clearly outlining how debts should be paid and who should manage the process, you reduce the likelihood of legal disputes that can drain the estate’s value. Professional legal counsel can help you structure your affairs so that your most valuable assets bypass probate entirely, ensuring they reach your heirs without being intercepted by credit card companies.

Using Life Insurance to Cover Outstanding Balances

For those concerned about leaving behind debt, a term life insurance policy can serve as a “debt safety net.” By calculating your average outstanding debt and purchasing a policy for that amount, you ensure that your loved ones have the liquidity needed to settle accounts or maintain their lifestyle without the burden of your liabilities. Because life insurance payouts are generally tax-free and bypass probate, they are an incredibly efficient tool for legacy protection.

Communicating with Beneficiaries About Financial Reality

Perhaps the most overlooked step in financial planning is communication. It is a gift to your heirs to leave behind an “organized death.” This includes a folder containing a list of all credit card accounts, login credentials, and the contact information for your executor. When family members know the state of your finances, they are less likely to be blindsided by creditors or fall victim to the stress of the unknown.

In conclusion, credit card debt after death is a manageable legal hurdle, not a mandatory inheritance. By understanding the roles of the estate, the nuances of state law, and the power of beneficiary designations, you can ensure that your financial legacy is defined by what you leave behind for your loved ones, rather than what you owed to the bank.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.