Losing a loved one is an emotionally taxing experience, often compounded by the daunting task of settling their earthly affairs. Among the most common and confusing financial hurdles is the question of outstanding debt—specifically, credit card bills. Many survivors worry that they will inherit the debt of the deceased or that their family home might be seized to pay off a lingering Visa or Mastercard balance.

In the realm of personal finance, understanding the intersection of credit debt and estate law is crucial. Debt does not simply vanish into thin air upon a person’s passing, but the rules governing who is responsible for it are more nuanced than many realize. This guide explores the lifecycle of a credit card bill after death, the legal frameworks that protect heirs, and the strategic steps survivors should take to manage the estate’s liabilities.

The Legal Fate of Credit Card Debt: Understanding the Probate Process

When a person passes away, everything they owned—from bank accounts and real estate to vehicles and personal belongings—becomes part of their “estate.” Simultaneously, everything they owed becomes a liability of that estate. The process of totaling these assets and liabilities, paying off creditors, and distributing the remainder to heirs is known as probate.

The Role of the Executor or Administrator

The first step in the financial aftermath of a death is the appointment of a legal representative. If the deceased left a will, they likely named an “executor.” If there is no will, the court appoints an “administrator.” This individual is a fiduciary, meaning they are legally obligated to act in the best interests of the estate.

The executor’s primary responsibility regarding credit cards is to identify all open accounts and notify the issuers. They must use the assets within the estate to pay off valid debts. It is important to note that the executor is not using their own money to pay these bills; they are using the deceased person’s money.

How Assets are Used to Settle Liabilities

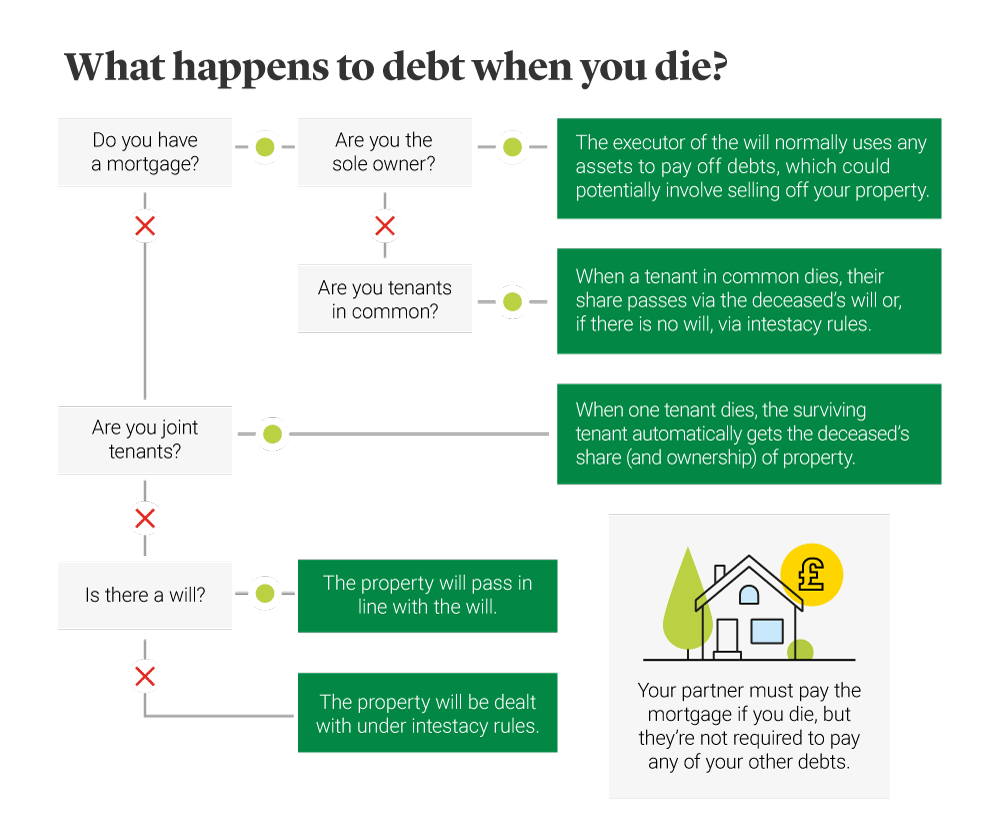

In the hierarchy of probate, creditors must be paid before any heirs receive an inheritance. Credit card debt is typically classified as “unsecured debt.” This means it is not backed by collateral like a house (mortgage) or a car (auto loan).

In the eyes of the law, unsecured creditors are often lower on the priority list than funeral expenses, taxes, and secured debts. If the estate has $50,000 in assets and $10,000 in credit card debt, the executor pays the $10,000, and the heirs split the remaining $40,000. However, if the estate is “insolvent”—meaning the debts exceed the assets—the credit card companies may simply be out of luck. In most cases, if there is no money left in the estate, the debt goes unpaid and is eventually written off by the lender.

Liability and Responsibility: Who is Actually on the Hook?

One of the biggest fears for grieving spouses and children is that they will be held personally liable for a loved one’s spending. Under federal law and standard contract law, children and other relatives are generally not responsible for the deceased’s credit card debt. However, there are three significant exceptions to this rule.

Individual Accounts vs. Joint Accounts

The distinction between an individual account and a joint account is the most critical factor in determining liability. If a credit card was in the deceased’s name alone, the estate is responsible. If the estate cannot pay, the debt dies with the individual.

However, if the account was a “joint account”—where two people applied together and both had equal access and responsibility—the surviving joint account holder is 100% responsible for the remaining balance. The lender does not care who made the purchases; the contract binds both parties to the total debt.

The Difference Between Co-signers and Authorized Users

It is common to confuse “co-signers” with “authorized users,” but the legal implications are worlds apart. A co-signer is someone who guaranteed the debt at the time of application, usually to help the primary borrower qualify. Like a joint account holder, a co-signer is fully liable for the balance after the primary borrower passes away.

An authorized user, conversely, is someone who was given permission to use the card but never signed a contract assuming financial responsibility. If you were an authorized user on your late parent’s card, you are not responsible for the bill. In fact, you should stop using the card immediately upon their death, as continued use could be flagged as fraud.

Community Property States and Shared Debt

In the United States, nine states follow “community property” laws: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. In these states, most debts incurred by one spouse during the marriage are considered the joint responsibility of both spouses, even if only one name was on the credit card.

If you live in a community property state, the surviving spouse might be required to pay off the deceased spouse’s credit card debt using community assets. This is a complex area of financial law, and consulting with an estate attorney in these specific states is highly recommended to protect your personal assets.

Practical Steps for Survivors and Heirs

Managing the administrative side of death is a race against interest rates and automated systems. Taking swift action can prevent the estate from being eroded by unnecessary fees and protect the credit scores of surviving joint holders.

Notifying Issuers and Credit Bureaus

As soon as possible, the executor should contact the customer service department of each credit card issuer to report the death. Most banks have a dedicated “deceased notification” or “estates” department. You will typically need to provide a certified copy of the death certificate.

Once notified, the bank will freeze the account to prevent further charges and stop the accrual of late fees. Simultaneously, it is wise to notify the three major credit bureaus (Equifax, Experian, and TransUnion). This places a “deceased” flag on the person’s credit report, which is a vital step in preventing posthumous identity theft.

Managing Automatic Payments and Subscriptions

In the digital age, many credit cards are linked to recurring subscriptions—Netflix, gym memberships, insurance premiums, and utility bills. When a cardholder dies, these charges continue to hit the account until it is closed.

The executor should review recent statements to identify these recurring charges. If a utility bill is linked to the card, it should be transitioned to a different payment method to ensure that electricity or water isn’t shut off at the deceased’s residence while the home is being prepared for sale or transfer.

Protecting the Estate from Collection Harassment

Unfortunately, some debt collectors can be aggressive, even when dealing with an estate. Under the Fair Debt Collection Practices Act (FDCPA), collectors are allowed to contact the surviving spouse or the executor to discuss the debt. However, they are not allowed to mislead you into thinking you are personally responsible for the debt if you are not.

If a collector pressures you to pay a deceased relative’s debt out of your own pocket, you have the right to request that they cease all communication. All further inquiries should be directed to the estate’s legal representative.

Strategic Financial Planning to Protect Your Legacy

While the immediate concern is often “what happens now,” the most effective way to handle credit card debt and death is through proactive financial planning. Understanding how debt impacts an estate can help individuals structure their finances to ensure their heirs are protected.

Life Insurance as a Debt Shield

Life insurance is one of the most effective tools for “debt-proofing” an estate. Unlike bank accounts or real estate, life insurance payouts usually go directly to named beneficiaries and do not pass through probate. This means the money is generally protected from the deceased’s creditors.

If you carry significant credit card debt, having a term life insurance policy ensures that your spouse or children have the cash flow to maintain their lifestyle or voluntarily settle debts without having to liquidate family heirlooms or the family home.

The Importance of a Clear Will and Trust

A well-drafted will provides clear instructions for the executor on how to handle liabilities. More importantly, using a Living Trust can allow assets to bypass probate entirely. Since creditors primarily target assets within the probate estate, assets held in a trust may be more difficult for credit card companies to reach.

Furthermore, transparency with family members about financial health is a gift. Keeping a “letter of instruction” that lists all open credit accounts, passwords, and the location of physical cards can save survivors hundreds of hours of frustration and legal fees.

Conclusion: Balancing Empathy and Financial Prudence

The intersection of grief and debt is never easy to navigate. While the law generally protects individuals from inheriting the credit card debt of their loved ones, the estate remains on the hook. By understanding the roles of executors, the nuances of joint accounts, and the specific laws of your state, you can ensure that the probate process is handled with integrity.

Navigating these financial waters requires a blend of prompt administrative action and legal awareness. By addressing credit card bills head-on, survivors can clear the path toward financial closure, ensuring that the legacy left behind is defined by memories and heritage rather than lingering balances and collection calls.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.