Small claims court is often described as the “people’s court,” a judicial venue designed to resolve disputes involving relatively small amounts of money without the need for expensive legal representation. From a personal finance and business perspective, understanding the mechanics of small claims court is an essential skill. Whether you are an individual trying to recover a security deposit or a small business owner chasing an unpaid invoice, the ability to navigate this system can mean the difference between a total financial loss and a successful recovery.

This guide explores the financial landscape of small claims court, detailing what happens from the moment you file a claim to the eventual collection of a judgment.

Understanding the Financial Thresholds and Purpose of Small Claims

The primary objective of small claims court is to provide an accessible, low-cost method for resolving monetary disputes. Unlike superior or district courts, which can involve years of discovery and high attorney fees, small claims are streamlined to focus on the bottom line.

Defining the Jurisdictional Limits

Every jurisdiction has a specific “dollar limit” for small claims. This is the maximum amount of money you can sue for in this specific court. In some states or regions, this limit might be as low as $2,500, while in others, it can go up to $15,000 or $25,000. Before proceeding, it is vital to calculate your total damages. If your claim significantly exceeds the limit, you may have to waive the excess amount to stay in small claims court, or move to a higher court where the legal costs may outweigh the potential recovery.

When Does Filing Make Financial Sense?

Just because you are owed money does not always mean you should sue. A savvy financial actor conducts a cost-benefit analysis before filing. You must consider the filing fees (usually ranging from $15 to $150), the cost of serving the defendant with papers, and the value of your time. Furthermore, you must assess the “collectability” of the defendant. If the person or business you are suing is insolvent or has no seizable assets, a court judgment is merely a piece of paper with no immediate monetary value.

The Pre-Court Phase: Preparation and Documentation

Success in small claims court is rarely determined by rhetorical flair; it is determined by the paper trail. Because these proceedings are brief, the person with the most organized financial evidence usually wins.

Gathering Financial Evidence and Receipts

To prove your case, you need to substantiate the exact amount of money in dispute. This requires a meticulous assembly of records, including:

- Invoices and Contracts: Any written agreement that outlines payment terms.

- Proof of Payment: Bank statements, canceled checks, or electronic transfer receipts showing what was paid or what was withheld.

- Estimates and Quotes: If you are suing for damages (e.g., a contractor’s poor work), you need written estimates from third-party professionals to prove the cost of repair.

- Communication Logs: Printouts of emails or text messages where the debt was acknowledged or disputed.

The Demand Letter: A Last Chance for Settlement

In many jurisdictions, you are legally required to demand payment before filing a lawsuit. Even if not required, it is a sound financial strategy. A formal demand letter—sent via certified mail—outlines the debt, the deadline for payment, and your intent to sue. This often prompts a settlement or a payment plan, saving you the time and expense of a court appearance. From a business finance perspective, a settlement at 80% of the debt today is often more valuable than a 100% judgment six months from now.

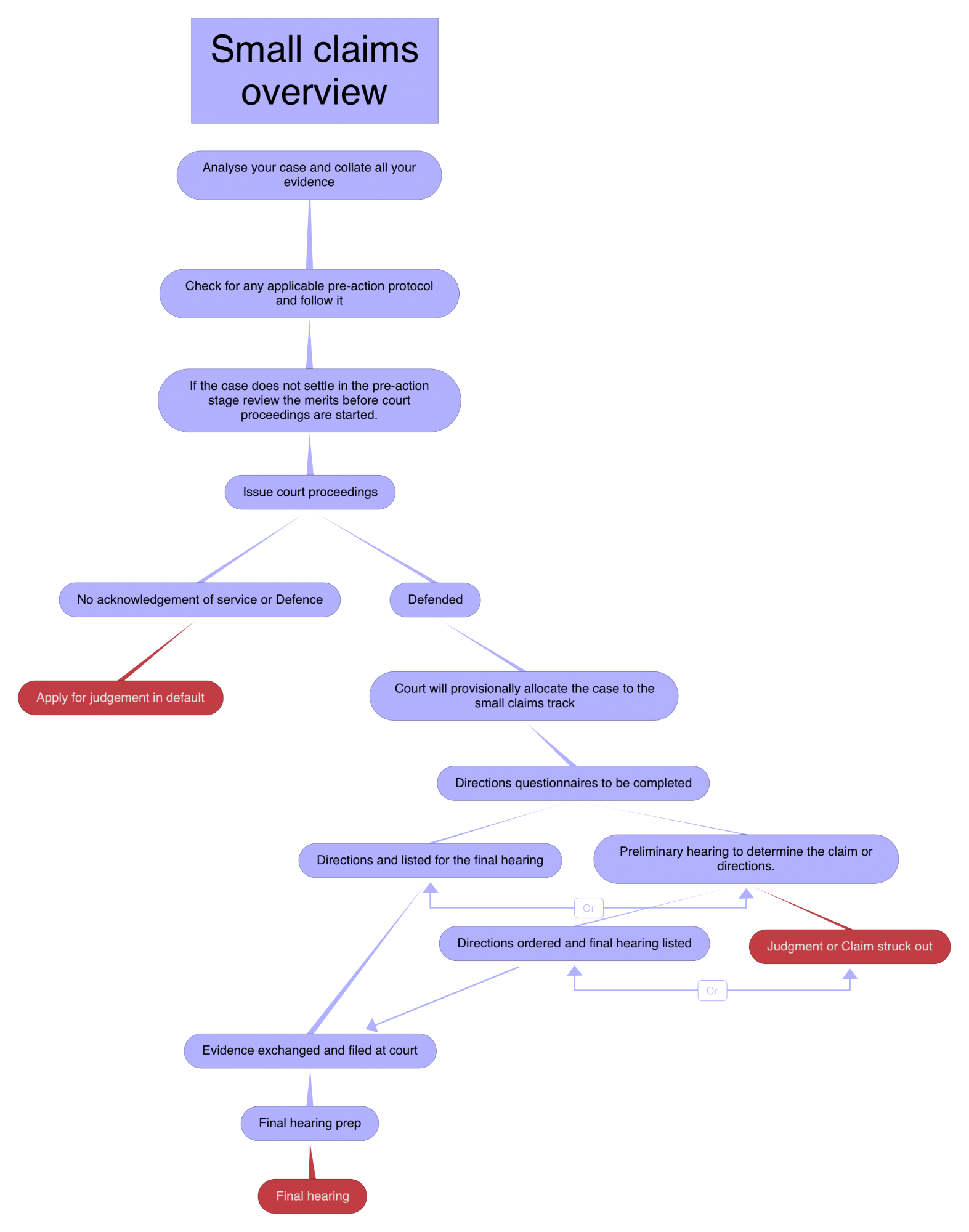

Navigating the Courtroom: The Step-by-Step Procedure

On the day of the hearing, the atmosphere is usually professional yet less formal than a high-stakes corporate trial. Most people represent themselves, though some jurisdictions allow attorneys.

Presenting Your Case to the Judge

When your case is called, the plaintiff (the person suing) speaks first. You must present a concise narrative focused on the financial facts. The judge is interested in three things: Was there an agreement? Was that agreement breached? What is the specific financial harm?

It is crucial to have your evidence organized in folders so you can quickly hand documents to the judge or the clerk. Avoid emotional arguments; instead, focus on the ledger. For example, rather than saying “the defendant was mean,” say “the defendant failed to deliver the goods as per the invoice dated October 12th, resulting in a loss of $1,200.”

Defending Against Counterclaims

In the realm of small claims, a “counterclaim” occurs when the person you are suing decides to sue you back within the same case. This is a common tactic used to offset the money they owe. You must be prepared to defend your finances against these claims. If a tenant sues for a $1,000 security deposit, a landlord might counterclaim for $1,200 in damages. The court will look at both sets of evidence and determine the “net” amount owed to one party or the other.

Post-Judgment Realities: Collecting Your Money

The most common misconception about small claims court is that the judge will hand you a check at the end of the hearing. This does not happen. The court issues a “judgment,” which is a legal recognition of the debt, but it is up to you to enforce it.

The Difference Between Winning and Collecting

A judgment is essentially a license to use the state’s power to collect money. If the defendant is honest, they may pay you voluntarily within 30 days. However, if they refuse, you must transition into the role of a debt collector. This involves additional costs, though these can often be added to the total judgment amount.

Tools for Asset Discovery and Wage Garnishment

If the debtor refuses to pay, you have several financial tools at your disposal:

- Wage Garnishment: You can obtain an order that requires the debtor’s employer to withhold a portion of their paycheck and send it directly to you.

- Bank Levy: With a court order, you can authorize the sheriff to freeze and seize funds directly from the debtor’s bank account.

- Property Liens: You can place a lien on the debtor’s real estate. While this doesn’t result in immediate cash, the debtor cannot sell or refinance the property without paying you first.

- Debtor’s Exam: You can haul the debtor back into court to testify under oath about their assets, bank accounts, and employment.

Strategic Financial Considerations for Small Business Owners

For entrepreneurs and small business owners, small claims court is a tool for maintaining healthy cash flow. However, it must be used strategically to ensure it doesn’t become a drain on resources.

Weighing Legal Fees vs. Potential Recovery

While small claims court is designed for self-representation, some business owners choose to consult with an attorney to prepare their filings or strategy. You must calculate the “opportunity cost” of your time. If you spend 20 hours preparing for a $500 claim, and your time is valued at $100 an hour, you are effectively losing money even if you win. Small businesses should reserve small claims for debts that are significant enough to justify the administrative overhead but too small for full-scale litigation.

Impact on Business Credit and Cash Flow

Consistently having to use small claims court to recover funds may indicate a problem with your business’s credit policy. If a high percentage of your accounts receivable ends up in court, it may be time to implement stricter upfront payment terms or more rigorous credit checks. Conversely, being sued in small claims court can damage your business’s credit rating and reputation with vendors. Managing these disputes efficiently—or avoiding them through better financial contracts—is a hallmark of a well-run business.

In conclusion, small claims court is a powerful financial instrument for those who know how to use it. By maintaining impeccable records, understanding the local jurisdictional rules, and being prepared for the realities of the collection process, you can effectively protect your assets and ensure that your personal or business finances remain secure. Success in this arena is less about legal “theatrics” and more about the cold, hard logic of the balance sheet.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.