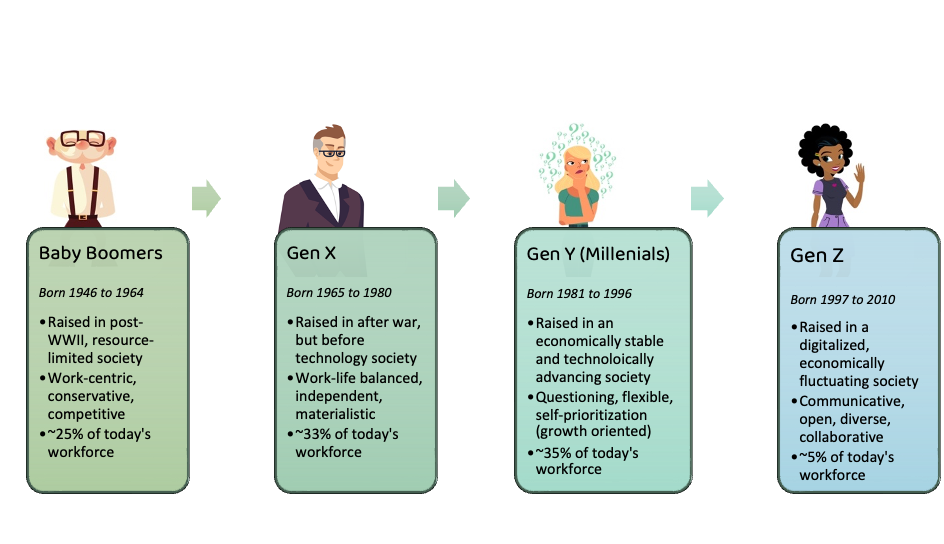

For decades, the cultural and economic conversation was dominated by the Baby Boomer generation. Born between 1946 and 1964, Boomers redefined the American Dream, fueled the post-war housing boom, and built the foundation of the modern consumer economy. However, as the sun began to set on the Boomer era, a new, leaner, and more pragmatic cohort emerged: Generation X.

Born approximately between 1965 and 1980, Generation X arrived during a period of significant social and economic flux. Often referred to as the “Latchkey Generation,” they grew up in an era of rising divorce rates and dual-income households, which fostered an early sense of independence and skepticism. In the realm of finance, Gen X serves as the critical bridge between the traditional pension-heavy world of their parents and the digital, gig-economy landscape of the Millennials who followed them. Today, Gen X finds itself in its peak earning years, grappling with a unique set of financial pressures and opportunities that will define the global economy for the next two decades.

The Economic Identity of the “Sandwich Generation”

Generation X occupies a unique space in the financial timeline. Unlike the Boomers, who often benefited from defined-benefit pension plans, Gen X was the first generation to be tasked with the responsibility of self-funding their retirement through defined-contribution plans like the 401(k). This shift fundamentally altered their relationship with money, moving it from institutional security to individual risk management.

Bridging the Gap Between Boomers and Millennials

Economically, Gen X is much smaller in size than the generations that bookend it. This “middle child” status has often led to them being overlooked by marketers and policy makers. However, their financial footprint is massive. They are currently the primary drivers of the workforce, occupying the majority of C-suite positions and senior management roles. While Boomers are transitioning into wealth decumulation (spending their savings), Gen X is in the high-stakes phase of wealth accumulation. They have witnessed multiple market cycles—from the “Black Monday” of 1987 to the Dot-com bubble and the 2008 Great Recession—giving them a seasoned, albeit cautious, perspective on investing.

The Peak Earning Years and Career Stability

Most members of Gen X are now between their mid-40s and late 50s. Historically, these are the peak earning years. This generation has traded the job-for-life loyalty of the Boomers for a more tactical approach to career progression. This adaptability has allowed them to command higher salaries in a tech-driven economy, but it also necessitates a more rigorous approach to personal branding and professional development to avoid being “aged out” by younger, cheaper talent. Their financial stability is the bedrock of the current economy, as they possess the highest disposable income of any age group, though much of it is currently earmarked for heavy familial obligations.

Personal Finance Challenges Unique to Gen X

While Gen X currently earns more than any other generation, they also face a “perfect storm” of financial demands. They are often called the “Sandwich Generation” because they are simultaneously providing financial support for their aging Boomer parents and their burgeoning Millennial or Gen Z children. This dual pressure creates a significant drag on their ability to save for their own fast-approaching retirement.

Managing the “Sandwich” Financial Pressure

The financial burden of being the “Sandwich Generation” cannot be overstated. On one side, the rising costs of elder care and the complexities of Medicare/Medicaid mean that Gen X is often subsidizing the living expenses or healthcare of their parents. On the other side, the skyrocketing cost of higher education has forced many Gen X parents to dip into their home equity or retirement savings to fund their children’s tuition. Balancing these “outward” cash flows while trying to maintain “inward” retirement savings requires a high level of financial literacy and disciplined budgeting.

Catch-up Contributions and Retirement Readiness

With retirement looming—some Gen Xers are less than a decade away—the focus has shifted aggressively toward “catch-up.” The IRS allows individuals over age 50 to contribute extra funds to their 401(k) and IRA accounts, a provision many Gen Xers are now utilizing to make up for lost time. However, the anxiety is real. Many in this cohort entered the workforce just as the safety nets of the past were being dismantled. Consequently, they are more likely to utilize sophisticated financial tools, such as Health Savings Accounts (HSAs) and diverse brokerage accounts, to maximize every dollar before they exit the workforce.

Investment Strategies for the Forgotten Generation

Because Gen X has lived through several major market crashes, their investment philosophy tends to be more balanced and risk-aware than the speculative nature often seen in younger cohorts. They aren’t just looking for growth; they are looking for resilience.

Risk Management in a Volatile Market

For Gen X, the goal is no longer just “getting rich”; it’s “staying solvent.” As they approach the “Red Zone” (the five to ten years before and after retirement), their asset allocation is shifting. We are seeing a move away from 100% equity portfolios toward a more classic 60/40 or 70/30 split, incorporating bonds, real estate, and inflation-protected securities (TIPS). They are the primary users of target-date funds, which automatically de-risk as they approach a specific retirement year. This pragmatic approach to risk management is a direct result of having seen “paper wealth” evaporate during the housing crisis of 2008.

Diversification and the Shift Toward Passive Income

Beyond traditional stocks and bonds, Gen X has shown a keen interest in diversifying into tangible assets. This generation holds a significant portion of the nation’s residential real estate wealth. Many have leveraged low interest rates in previous years to acquire rental properties, providing a stream of passive income that serves as a modern-day pension. Furthermore, they are increasingly exploring private equity and small business ownership as a “second act” career move, seeking to build equity in ventures they control rather than relying solely on the whims of the public markets.

Wealth Transfer and the Great Inheritance

One of the most significant financial events for Generation X is currently underway: The Great Wealth Transfer. As the Baby Boomer generation passes on, an estimated $68 trillion is expected to be transferred to their heirs, the majority of whom are Gen X. This influx of capital will fundamentally change the financial landscape.

Preparing for the Boomer Wealth Transfer

Receiving an inheritance is a complex financial event that requires careful planning to avoid massive tax liabilities. Gen X is currently working closely with estate planners and tax professionals to structure these transfers. Whether it is through step-up in basis on inherited property or managing the distributions from inherited IRAs, the way Gen X handles this windfall will determine their ultimate financial legacy. For many, this inheritance will be the “bailout” that allows them to finally secure their own retirement after years of supporting others.

Estate Planning and Legacy Building

Having seen the complexities of their parents’ estates, Gen X is being more proactive about their own legacy. There is a marked increase in the use of living trusts, power of attorney documents, and clear-cut wills among this group. They are focused on ensuring that their wealth—accumulated through decades of hard work and bolstered by inheritance—is passed down to Gen Z and Alpha with as little friction as possible. This generation understands that financial security is not just about the numbers in a bank account, but about the legal structures that protect those numbers.

Future Outlook: Gen X’s Impact on Global Markets

As Generation X moves toward the final stages of their careers, their influence on the economy remains potent. They are the “decision-makers” in the boardroom and the “spenders” in the household. Their transition into retirement will likely trigger another shift in the markets, moving focus from growth-oriented tech stocks toward value stocks, healthcare, and income-generating assets.

While they may have been the generation that came “after” the boomers, they are by no means an afterthought. Their financial journey—defined by the loss of the pension, the rise of the 401(k), the “sandwich” squeeze, and the impending Great Wealth Transfer—offers a masterclass in economic resilience. As they begin to hand over the reins of the economy to Millennials, the financial strategies and stability of Gen X will remain the benchmark for how to navigate a complex, modern financial world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.