In the modern financial landscape, the boundary between traditional banking and digital wallets has become increasingly porous. Cash App, developed by Block, Inc., has emerged as a titan in the peer-to-peer (P2P) payment sector, effectively functioning as a bridge between digital convenience and personal finance management. However, for many users transitioning from physical cash or legacy banking, the terminology within the app can occasionally cause confusion. Specifically, the question “what does withdraw mean on Cash App?” touches upon the fundamental concept of liquidity—the ease with which an individual can convert digital credits into accessible, external capital.

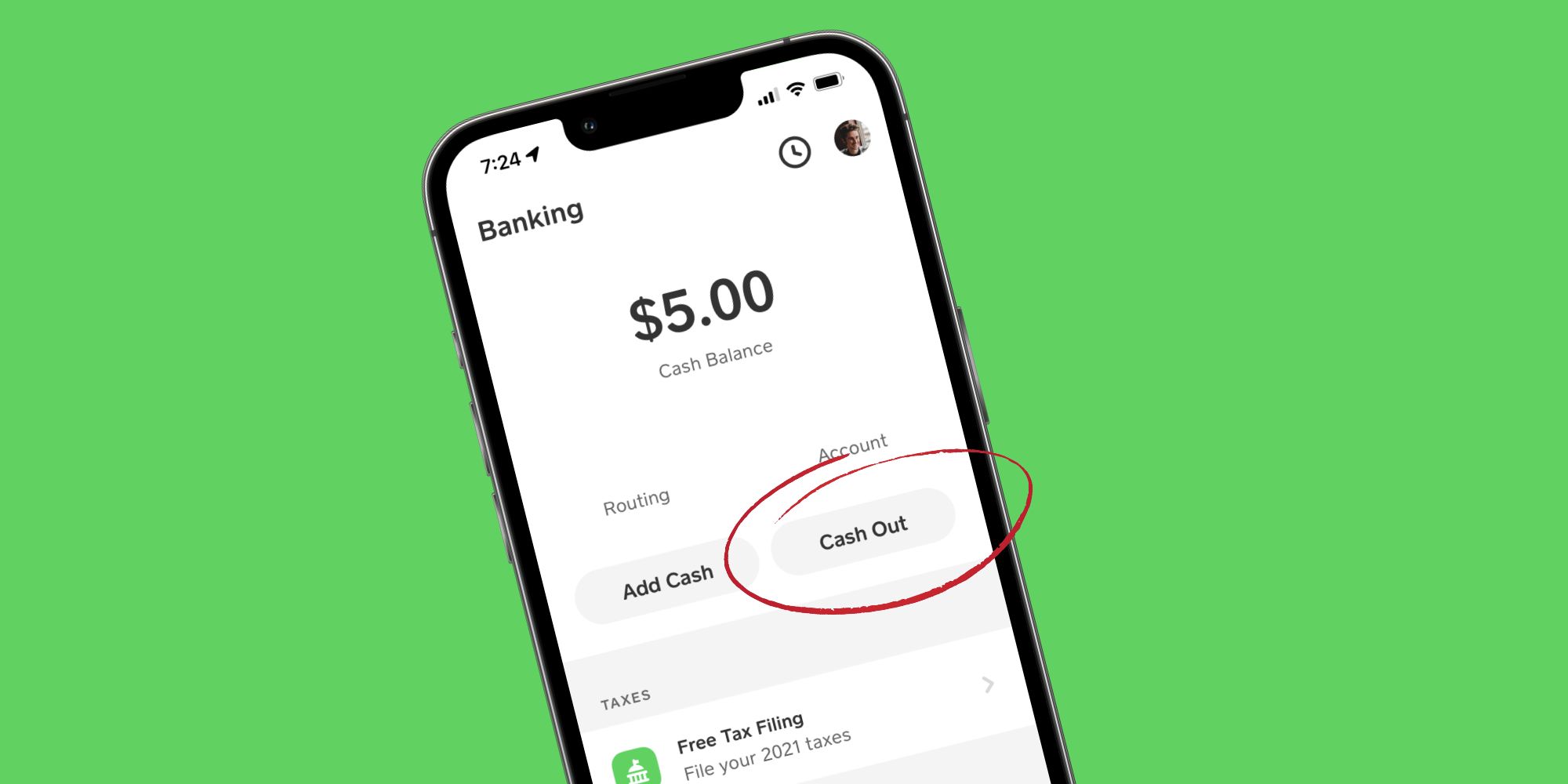

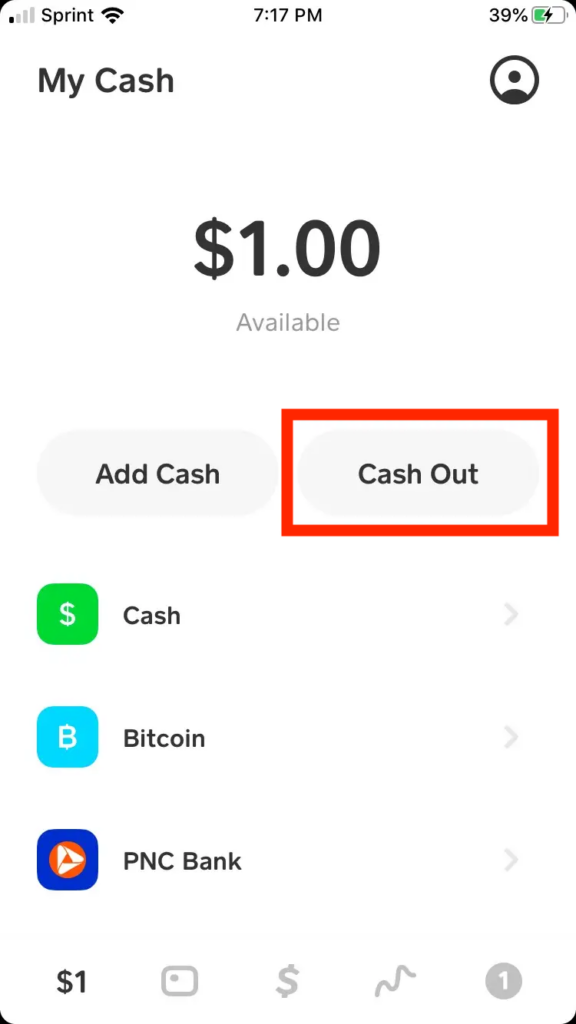

In the context of Cash App, a “withdrawal” refers to the process of transferring funds out of your protected digital wallet and into a linked external bank account or onto a physical debit card. This action is the final stage of the digital payment lifecycle, ensuring that the money you receive from friends, side hustles, or investment gains is usable in the broader economy.

The Definition of Withdrawal in the Digital Banking Ecosystem

At its core, “withdrawing” on Cash App is an act of reclaiming liquidity. When you hold a balance in Cash App, that money exists within a closed-loop system managed by the app’s financial partners. While you can spend this money directly using a Cash Card, a withdrawal is necessary if you intend to move those funds to a primary checking account, use them to pay mortgage or rent via traditional banking methods, or simply consolidate your assets.

Moving Funds from Digital Wallets to Traditional Accounts

For the modern consumer, the “digital wallet” acts as a temporary holding cell. Whether you have received a payment for a freelance gig or a reimbursement for a dinner bill, the funds initially sit in your Cash App balance. To “withdraw” means to initiate an Outbound Automated Clearing House (ACH) transfer or a real-time debit push. This transition is vital for personal finance management, as it allows users to move money from a high-velocity spending app into a more stable, long-term savings environment.

The Role of Cash App as a Financial Intermediate

Understanding withdrawal requires understanding Cash App’s role as an intermediary. It is not a bank itself; rather, it provides financial services through banking partners like Lincoln Savings Bank or Community Federal Savings Bank. Therefore, a withdrawal is technically a request for these partner banks to release your funds to your primary financial institution. This distinction is important for those managing business finance or significant personal assets, as it highlights the layers of digital architecture involved in a single “cash out” click.

Strategic Options for Accessing Your Capital

One of the most critical aspects of withdrawing on Cash App is choosing the method of transfer. In personal finance, time is often equated with money, and Cash App’s withdrawal structure reflects this principle. Users are presented with two primary paths: Standard Deposits and Instant Deposits.

Standard Deposits: Maximizing Interest and Avoiding Fees

The Standard Deposit is the preferred method for the fiscally conservative user who is not in an immediate rush. This method utilizes the ACH network, the same system used for direct deposits and utility payments.

- Timeframe: Usually takes 1 to 3 business days.

- Cost: Free.

By opting for a Standard Deposit, you ensure that 100% of your capital reaches its destination. In the realm of personal finance, avoiding unnecessary fees is a cornerstone of wealth preservation. If you are withdrawing a significant sum—perhaps a few thousand dollars—saving the percentage fee associated with instant transfers is a prudent financial decision.

Instant Deposits: The Cost of Immediate Liquidity

For those facing an immediate expense or a cash flow gap, Cash App offers the “Instant” withdrawal option. This utilizes the “Original Credit Transaction” (OCT) process through the Visa or Mastercard networks.

- Timeframe: Near-instantaneous (usually within minutes).

- Cost: A fee typically ranging from 0.5% to 1.75% (with a minimum fee).

While the convenience is undeniable, the “money” perspective suggests using this sparingly. For a side hustler relying on quick turnover, this fee is a cost of doing business. However, for everyday personal use, frequent instant withdrawals can erode one’s savings over time. Calculating the “opportunity cost” of this fee is an essential skill for any savvy app user.

Managing Your Personal Finance through Investment Withdrawals

Cash App has evolved beyond simple transfers; it is now a robust platform for micro-investing in stocks and Bitcoin. Consequently, “withdraw” takes on a multi-layered meaning when dealing with these asset classes. You cannot withdraw “shares” or “Satoshis” directly to a standard bank account; you must first liquidate the asset.

Divesting from Stocks and Reclaiming Principal

If you have invested in fractional shares of a company, the “withdrawal” process begins with selling those shares. Once the sale is executed, the proceeds move into your Cash App balance. From there, the standard withdrawal rules apply. For an investor, understanding the “settlement period” is crucial. After selling a stock, it may take a day or two for the funds to be “settled” and available for a final withdrawal to your bank. This is a critical component of managing one’s liquidity ratio and ensuring that investment capital can be converted back to cash when needed.

Withdrawing from the Bitcoin Wallet

Bitcoin withdrawals on Cash App are unique because the platform allows for “On-Chain” transfers. This means “withdrawing” can also mean moving your Bitcoin from Cash App to a private hardware wallet or another exchange. This is a high-level financial move often recommended for digital security (“not your keys, not your coins”). Alternatively, if you want the fiat value, you sell the Bitcoin and withdraw the USD. Understanding the volatility and the transaction fees associated with the blockchain is paramount for anyone using Cash App as a gateway to cryptocurrency.

Security Protocols and Financial Guardrails

When dealing with the movement of capital, security and regulatory compliance are non-negotiable. “Withdrawing” is not just a technical process; it is a regulated one. To protect against money laundering and fraud, Cash App imposes certain limits and verification requirements.

Verification Limits and Transaction Thresholds

For a basic, unverified account, withdrawal limits are quite restrictive. To increase these limits—essential for those using the app for business finance or significant side income—users must undergo a “Know Your Customer” (KYC) verification. This involves providing a full name, date of birth, and the last four digits of a Social Security Number. Once verified, the withdrawal capacity increases significantly, allowing for the movement of larger tranches of capital. Understanding these thresholds is vital for financial planning, especially if you are expecting a large transfer that you intend to move to your bank immediately.

Protecting Your Assets During the Withdrawal Process

A “withdrawal” is a point of vulnerability in the digital finance chain. Professional financial management dictates that you ensure your linked bank account is secure and that your Cash App is protected by two-factor authentication (2FA) or biometric locks. Because withdrawals are often permanent and difficult to reverse once they hit the ACH or debit networks, confirming the destination of the funds is a critical step in maintaining financial integrity.

Conclusion: The Strategic Importance of the Withdrawal Process

In summary, to “withdraw” on Cash App is to execute a strategic move of capital from a digital-first environment to a traditional financial institution. Whether you are a casual user splitting a bill, a freelancer receiving payment, or an investor managing a portfolio of Bitcoin and stocks, the withdrawal function is your primary tool for realizing the value of your digital assets.

By understanding the difference between Standard and Instant deposits, the nuances of asset liquidation, and the necessity of account verification, you can manage your personal finances with greater precision. In the world of modern money, it is not just about how much you earn or receive; it is about how effectively you can move, protect, and access that wealth. Withdrawing is the final, essential link in that chain of financial empowerment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.