In the sophisticated world of global finance, efficiency and security are the two pillars upon which trillions of dollars in transactions rest every day. While the modern consumer is increasingly focused on blockchain, digital wallets, and real-time bank transfers, there is a legacy technology that remains the silent engine of the global banking system. This technology is MICR.

MICR stands for Magnetic Ink Character Recognition. It is a specialized technology used primarily by the banking industry to facilitate the processing and clearance of checks and other sensitive financial documents. Despite the rise of digital-first banking, MICR remains a fundamental component of business finance, ensuring that the physical movement of money remains accurate, secure, and resistant to fraud.

This guide explores the depths of MICR technology, its strategic importance in financial tools, and why it remains indispensable for businesses and financial institutions worldwide.

Understanding the Foundation of MICR in Business Finance

To appreciate the value of MICR, one must first understand its technical composition and why it was developed. Before the mid-1950s, check processing was a manual, labor-intensive task. As the volume of checks grew post-World War II, the banking industry faced a crisis of scalability. The American Bankers Association (ABA) sought a solution that would allow machines to read check information accurately even if the document was smudged, wrinkled, or written over.

The Definition and Origin of Magnetic Ink Character Recognition

MICR technology utilizes a special type of ink or toner that contains iron oxide. This magnetic material allows the characters printed on a document to be magnetized and read by a machine, even if they are obscured by stamps, signatures, or dirt. Unlike standard optical character recognition (OCR), which relies on visual clarity, MICR relies on the magnetic signal emitted by the ink.

The development of MICR in the late 1950s by the Stanford Research Institute and General Electric revolutionized the banking world. It allowed for the automation of check sorting, reducing human error and increasing the speed of the clearing cycle from weeks to days. Today, MICR is the international standard for check processing, governed by strict ISO (International Organization for Standardization) guidelines.

How MICR Differs from Standard Printing

In the context of business finance, it is a common misconception that any high-quality printer can produce valid financial documents. Standard inkjet and laser printers use carbon-based or dye-based inks. While these look identical to the naked eye, they lack the magnetic properties required by bank reader-sorters.

When a check is processed, it passes through a MICR reader which magnetizes the ink and translates the magnetic “shape” of each character into digital data. If a business attempts to print checks with standard toner, the bank’s equipment will fail to pick up a signal, leading to manual processing fees, delayed transactions, or the outright rejection of the check. Understanding this distinction is crucial for any business owner looking to optimize their internal financial workflows.

The Role of MICR in Modern Banking Operations

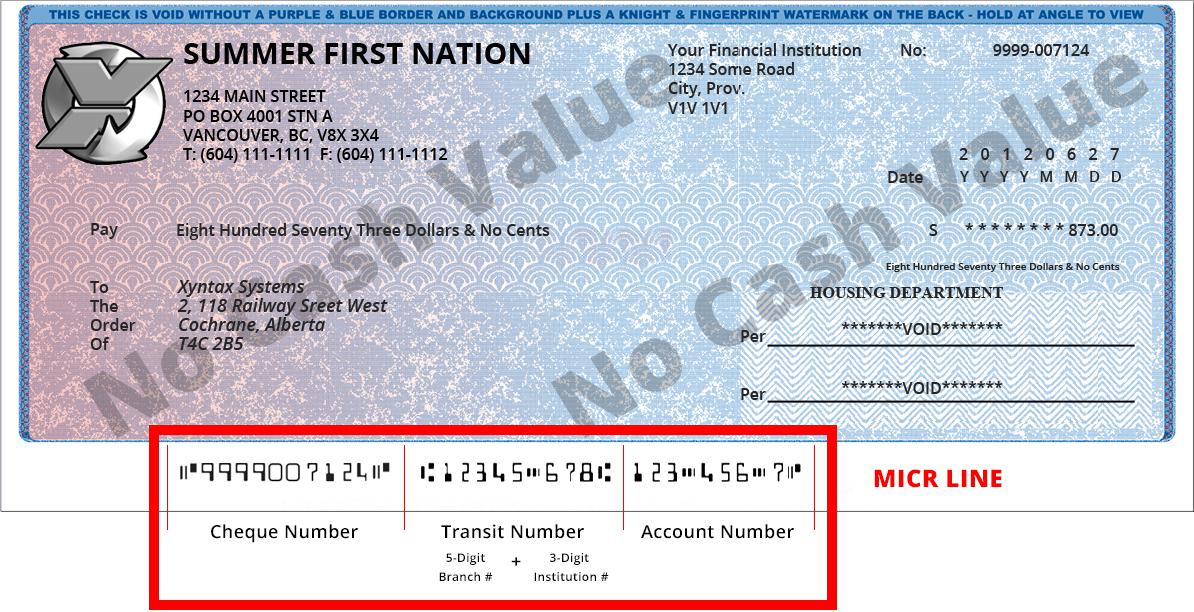

The strings of numbers you see at the bottom of a check are not just random digits; they are a highly structured data set formatted in a specific MICR font. These numbers typically include the routing transit number, the account number, and the specific check number.

The Check Clearing Process (Check 21 Act)

While the world has moved toward “Check 21” (The Check Clearing for the 21st Century Act), which allows banks to process electronic images of checks, MICR technology remains the source of truth. Even when a check is scanned via a mobile app or a teller’s desktop scanner, the MICR line provides the most reliable data.

In a high-speed banking environment, reader-sorters can process up to 2,400 checks per minute. The MICR line allows these machines to instantly categorize checks by their bank of origin, ensuring the funds are routed from the correct institution to the correct recipient. This automation is what keeps the liquidity of the business world flowing without the bottlenecks of manual data entry.

Global Standards: E-13B vs. CMC-7 Fonts

There are two primary MICR fonts used globally, and understanding which one applies to your region is vital for international business finance compliance.

- E-13B: This is the standard used in the United States, Canada, the United Kingdom, and Australia. It consists of only 14 characters: the numbers 0–9 and four special symbols (transit, amount, on-us, and dash). It is designed to be easily readable by both machines and humans.

- CMC-7: Used extensively across Europe, South America, and parts of Asia, this font is more complex. Each character is composed of five thin bars with varying spaces, which creates a unique magnetic signature.

For multinational corporations, ensuring that payroll and vendor checks are printed using the correct regional MICR font is a baseline requirement for financial operational excellence.

Why MICR Remains a Critical Tool for Financial Security

In an era of sophisticated cybercrime, one might wonder why a physical, magnetic technology is still prioritized. The answer lies in its inherent security features. MICR is significantly harder to forged or alter than standard digital or printed text.

Combating Forgery and Alteration

Financial fraud costs businesses billions of dollars annually. MICR technology serves as a primary line of defense. Because the MICR characters are printed with magnetic ink, any attempt to alter the routing or account numbers using standard pens or printers will be immediately detected by the bank’s magnetic sensors.

Furthermore, because the MICR line must be printed with extreme precision—often within 1/16th of an inch of a specific location—counterfeit checks produced on consumer-grade equipment rarely pass the rigorous mechanical checks of a professional financial institution. This physical barrier to entry makes “check washing” and other forms of document fraud significantly more difficult to execute successfully.

Reliability in High-Volume Environments

For businesses dealing with high volumes of outgoing payments—such as insurance companies, government agencies, or large retail corporations—reliability is a financial metric. Optical Character Recognition (OCR) systems have an error rate that can be affected by the background design of the check or the presence of a signature that overlaps the numbers.

MICR, however, has an incredibly low error rate. Because it “ignores” anything that isn’t magnetic, it can read through signatures, coffee stains, or cancellation stamps. For a CFO, this translates to fewer administrative headaches and lower “exception processing” costs from banks.

Implementing MICR Technology in Your Business

For many small to medium enterprises (SMEs), the question is not just “what does MICR stand for,” but “how do I use it to save money?” Many businesses are moving away from pre-printed checks provided by banks toward in-house check printing solutions.

Cost Efficiency and In-House Check Printing

Purchasing pre-printed checks from a bank is often expensive and poses a security risk, as a stack of blank checks with your account info already on them is a liability. By utilizing MICR-capable printers and specialized MICR toner, businesses can print their own checks on blank security paper.

This approach offers several financial advantages:

- Reduced Inventory Costs: No need to store different check stocks for different bank accounts.

- Enhanced Security: Information is only printed at the moment of the transaction.

- Operational Agility: Changes to bank account details or company addresses can be updated in the software instantly, without wasting pre-printed stock.

Compliance Requirements for Commercial Accounts

If your business decides to print its own checks, compliance is non-negotiable. Banks have strict “Signal Strength” requirements. If the magnetic signal of your MICR ink is too weak or too strong, the check will fail. Investing in high-quality, MICR-compliant financial tools—specifically the right software and toner—is an essential investment in the professionalism and reliability of your business’s financial operations.

The Future of MICR in an Increasingly Digital Economy

As we look toward the future of money, the role of MICR is evolving rather than disappearing. While the “death of the check” has been predicted for decades, the reality is that many B2B transactions still rely on paper for record-keeping and auditing purposes.

MICR in the Age of Mobile Deposits

The rise of Mobile Imaging and Remote Deposit Capture (RDC) has changed how the MICR line is consumed. Even when a check is “read” by a smartphone camera using OCR, the MICR line remains the anchor. The specific font shapes of E-13B are optimized for high-contrast recognition, making them the most reliable part of the document for a mobile app to interpret.

Sustainability and Transitioning Financial Workflows

As businesses move toward ESG (Environmental, Social, and Governance) goals, there is a push to reduce paper. However, for those instances where paper is required, MICR technology ensures that the paper is processed as efficiently as possible, minimizing the carbon footprint associated with repeated shipping and manual handling of rejected documents.

In conclusion, MICR stands for Magnetic Ink Character Recognition, but for the modern business professional, it stands for something much more: reliability, security, and the bridge between traditional banking and the digital future. By understanding and leveraging this technology, businesses can protect their assets, streamline their accounts payable, and ensure they remain in compliance with the global financial standards that keep the economy moving.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.