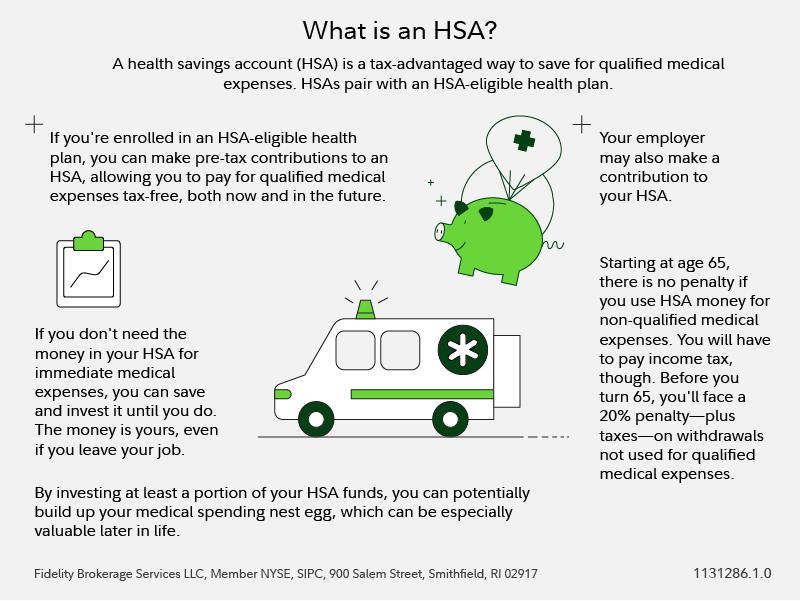

A Health Savings Account (HSA) is a powerful financial tool that allows individuals to save for qualified medical expenses on a tax-advantaged basis. More than just a savings vehicle, an HSA acts as a bridge between your healthcare needs and your financial well-being, offering significant benefits for those enrolled in high-deductible health plans (HDHPs). Understanding what an HSA covers is crucial to maximizing its potential and ensuring you are making the most of this valuable benefit.

Understanding the Fundamentals of HSA Eligibility and Contributions

Before delving into the specifics of what an HSA covers, it’s essential to grasp the foundational aspects of who can open an HSA and how funds are deposited. These core components dictate the very availability and growth of the money you can use for healthcare.

Who is Eligible for an HSA?

Eligibility for a Health Savings Account is tied directly to your health insurance coverage. To open and contribute to an HSA, you must meet the following criteria:

- Enrollment in a High-Deductible Health Plan (HDHP): This is the primary requirement. An HDHP is defined by the IRS with specific minimum deductible and maximum out-of-pocket limits that change annually. For 2023, an HDHP for self-only coverage must have a minimum deductible of $1,500 and a maximum out-of-pocket expense of $7,500. For family coverage, the minimum deductible is $3,000, and the maximum out-of-pocket expense is $15,000. These figures are adjusted for inflation each year.

- Not enrolled in Medicare: Individuals eligible for Medicare, including those receiving Social Security retirement benefits, cannot contribute to an HSA.

- Not covered by another health plan that is not an HDHP: You cannot have coverage under another health insurance plan, such as a traditional PPO or HMO, that is not considered an HDHP, even if it’s a secondary plan. However, you can have other specific types of coverage, like dental, vision, or disability insurance, and still be eligible.

- Not claimed as a dependent on someone else’s tax return: If someone else claims you as a dependent on their federal tax return, you are generally not eligible to contribute to an HSA.

The IRS meticulously reviews these eligibility requirements. Maintaining eligibility throughout the year is key to avoiding penalties and taxes on contributions.

How Contributions Work and Their Tax Advantages

HSAs offer a triple tax advantage, making them exceptionally attractive for long-term financial planning related to healthcare:

- Tax-Deductible Contributions: Contributions made to your HSA are typically tax-deductible. This means the money you deposit reduces your taxable income for the year, lowering your overall tax burden. This is true whether your employer contributes to your HSA or if you contribute directly from your paycheck or personal bank account.

- Tax-Free Growth: Any interest or investment earnings your HSA generates grow tax-free. As your balance increases through prudent investments, you won’t owe taxes on those gains until you withdraw the funds.

- Tax-Free Withdrawals for Qualified Medical Expenses: The most significant benefit is that withdrawals made for qualified medical expenses are completely tax-free. This means you get to use your money for healthcare costs without it being subject to federal income tax.

Contribution limits are set annually by the IRS and depend on whether you have self-only or family HDHP coverage. There’s also a “catch-up” contribution provision for individuals aged 55 and older, allowing them to contribute an additional amount each year.

What Qualified Medical Expenses Can Your HSA Cover?

The core purpose of an HSA is to cover healthcare costs. The IRS defines a broad range of “qualified medical expenses” that can be paid for using HSA funds without incurring taxes or penalties. This list is extensive and designed to encompass most healthcare needs.

Prescription Medications and Over-the-Counter (OTC) Drugs

Prescription medications are a primary and expected use of HSA funds. This includes any medication prescribed by a doctor to treat, diagnose, cure, mitigate, or prevent disease, or to affect the structure or function of the body.

Beyond prescription drugs, the Tax Cuts and Jobs Act of 2017 expanded the list of qualified OTC medicines and drugs that can be purchased using HSA funds without a prescription. This now includes items such as:

- Pain relievers (e.g., ibuprofen, acetaminophen)

- Allergy medications

- Cold and cough remedies

- Digestive aids

- Topical creams and ointments

It’s important to note that while many OTC items are now covered, certain products, like dietary supplements or cosmetic items, are generally not considered qualified medical expenses unless prescribed by a doctor for a specific medical condition. Always check the IRS guidelines or your HSA administrator’s list for clarity.

Medical, Dental, and Vision Care Services

A significant portion of what an HSA covers includes direct medical services. This encompasses a wide array of treatments and procedures:

- Doctor’s Visits: Co-pays and deductibles for visits to your primary care physician, specialists, and any other healthcare provider.

- Hospital Services: Costs associated with inpatient or outpatient hospital care, including surgery, room and board, and other related fees.

- Diagnostic Tests and Screenings: Services such as X-rays, MRIs, blood tests, and cancer screenings.

- Therapies: Physical therapy, occupational therapy, speech therapy, and mental health counseling.

- Medical Equipment: Items like crutches, walkers, wheelchairs, prosthetic devices, and durable medical equipment prescribed by a doctor.

- Dental Care: Most dental services, including check-ups, cleanings, fillings, braces, dentures, and surgical procedures like tooth extractions or root canals.

- Vision Care: Eye exams, prescription eyeglasses, contact lenses, and corrective vision surgery like LASIK.

The breadth of coverage for these services means your HSA can be a vital resource for managing both routine and unexpected healthcare needs.

Preventive Care and Wellness

Many HDHPs are designed to encourage preventive care, and HSAs align with this philosophy. Many preventive services are covered by insurance plans without requiring you to meet your deductible, and any costs associated with these services can be paid for by your HSA. This includes:

- Annual physical examinations

- Screenings for conditions like high blood pressure, diabetes, and certain cancers

- Vaccinations and immunizations

- Counseling on healthy lifestyle choices

- Certain prenatal and postnatal care services

By covering these services, HSAs support a proactive approach to health, which can lead to better long-term health outcomes and potentially lower healthcare costs over time.

Other Qualified Medical Expenses

The IRS guidelines for qualified medical expenses are quite comprehensive. Beyond the common categories, your HSA can also cover:

- Premiums for COBRA continuation coverage: If you lose your job and opt for COBRA coverage, you can use HSA funds to pay for those premiums.

- Premiums for qualified Long-Term Care Insurance: A portion of the premiums paid for qualified long-term care insurance can be reimbursed from your HSA, up to certain limits.

- Health insurance premiums while receiving unemployment benefits: If you are receiving federal or state unemployment compensation, you can use HSA funds to pay for your health insurance premiums.

- Costs incurred due to a disability: This can include expenses for specialized equipment or services needed due to a disability.

- Costs for certain medical aids and devices: This can extend to items like hearing aids, glucose monitors, and other health-related devices.

- Transportation and lodging for medical care: The cost of transportation (mileage, tolls, parking) and lodging when traveling to receive medical care is also considered a qualified expense, provided it’s primarily for and essential to receiving medical care.

It’s crucial to consult your HSA administrator or the IRS Publication 502, Medical and Dental Expenses, for the most accurate and up-to-date information on qualified expenses.

Beyond Medical Needs: Using Your HSA for Retirement and Long-Term Goals

While the primary function of an HSA is to cover current medical expenses, its value extends far beyond immediate healthcare needs, particularly concerning long-term financial planning and retirement. The tax-free growth and withdrawal benefits make it an attractive investment vehicle for future use.

Investing Your HSA Funds for Growth

One of the most significant advantages of an HSA is its potential to grow as an investment account. Most HSA providers offer investment options similar to those found in 401(k)s or IRAs, such as mutual funds and exchange-traded funds (ETFs).

- Tax-Free Investment Growth: As mentioned, any earnings generated from your HSA investments grow tax-free. This compound growth can significantly bolster your savings over the years, especially if you have a long time horizon.

- Strategic Investment Choices: You have the flexibility to choose investments that align with your risk tolerance and financial goals. Conservative investors might opt for bonds or stable value funds, while those with a higher risk appetite might choose stock-based funds.

- Long-Term Accumulation: The longer your HSA funds are invested, the greater the potential for growth. Many individuals use their HSA as a supplemental retirement savings account, contributing consistently and allowing their investments to mature.

It’s important to note that accessing investment funds may have its own set of rules and potential transaction fees, depending on your HSA administrator.

Using HSA Funds in Retirement

The flexibility of HSA withdrawals extends into retirement. Once you reach Medicare eligibility age (typically 65), you can use your HSA funds for any purpose, not just qualified medical expenses, and the withdrawals will be taxed as ordinary income, similar to withdrawals from a traditional IRA or 401(k).

- Supplementing Retirement Income: This allows your HSA to act as a secondary source of retirement income, providing funds for living expenses, travel, or any other needs.

- Continuing to Cover Healthcare Costs: Even in retirement, healthcare costs can be substantial. Your HSA remains a tax-free resource for these ongoing medical expenses, which often increase with age. This can be particularly beneficial if you anticipate significant long-term care needs.

- Estate Planning: If you pass away with funds remaining in your HSA, the account can be passed on to your beneficiaries. If the beneficiary is your spouse, they can continue to use the HSA as their own, maintaining its tax-advantaged status. If the beneficiary is not your spouse, they will receive the assets tax-free from an income tax perspective, but they will be required to pay estate taxes on the value of the account.

This dual purpose – a robust savings vehicle for current healthcare and a powerful investment tool for long-term financial security – underscores the multifaceted value of a Health Savings Account. By understanding its coverage and strategically utilizing its investment features, individuals can harness the full potential of their HSA to achieve both their immediate and future financial and health goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.