The term “current balance” on a credit card statement can sometimes feel like a moving target, a number that fluctuates based on your spending habits and payment cycles. Understanding its precise meaning is fundamental to effectively managing your credit and maintaining your financial well-being. It’s not just a static figure; it’s a dynamic representation of your financial obligations at a specific point in time. This article will delve into the intricacies of the current balance, its implications, and how it interacts with other key credit card metrics.

Understanding the Core Concept: Current Balance vs. Statement Balance

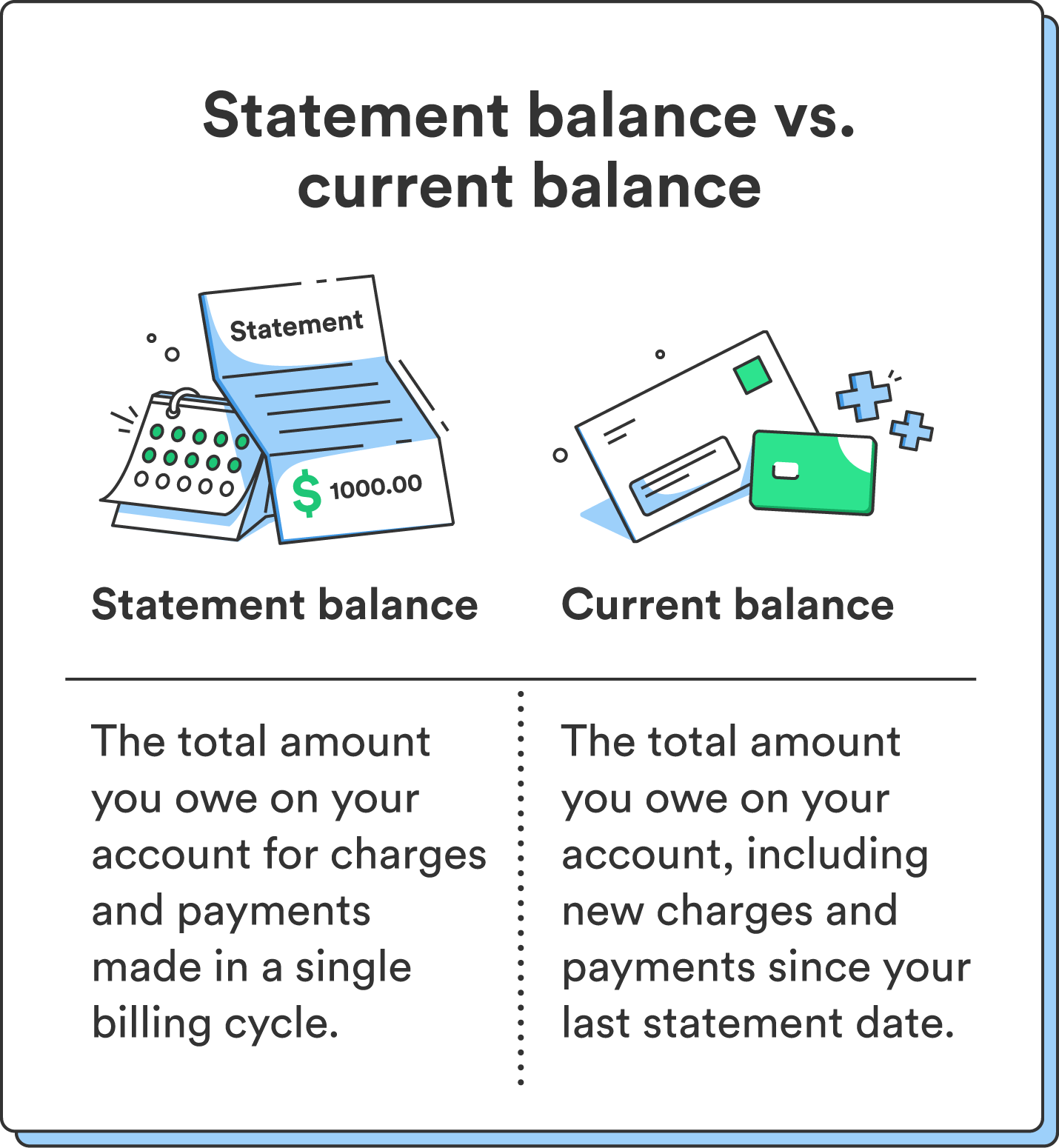

At its heart, the current balance represents the total amount of money you owe to your credit card issuer at any given moment. However, to truly grasp its significance, we must differentiate it from another crucial figure: the statement balance.

The Statement Balance: A Snapshot in Time

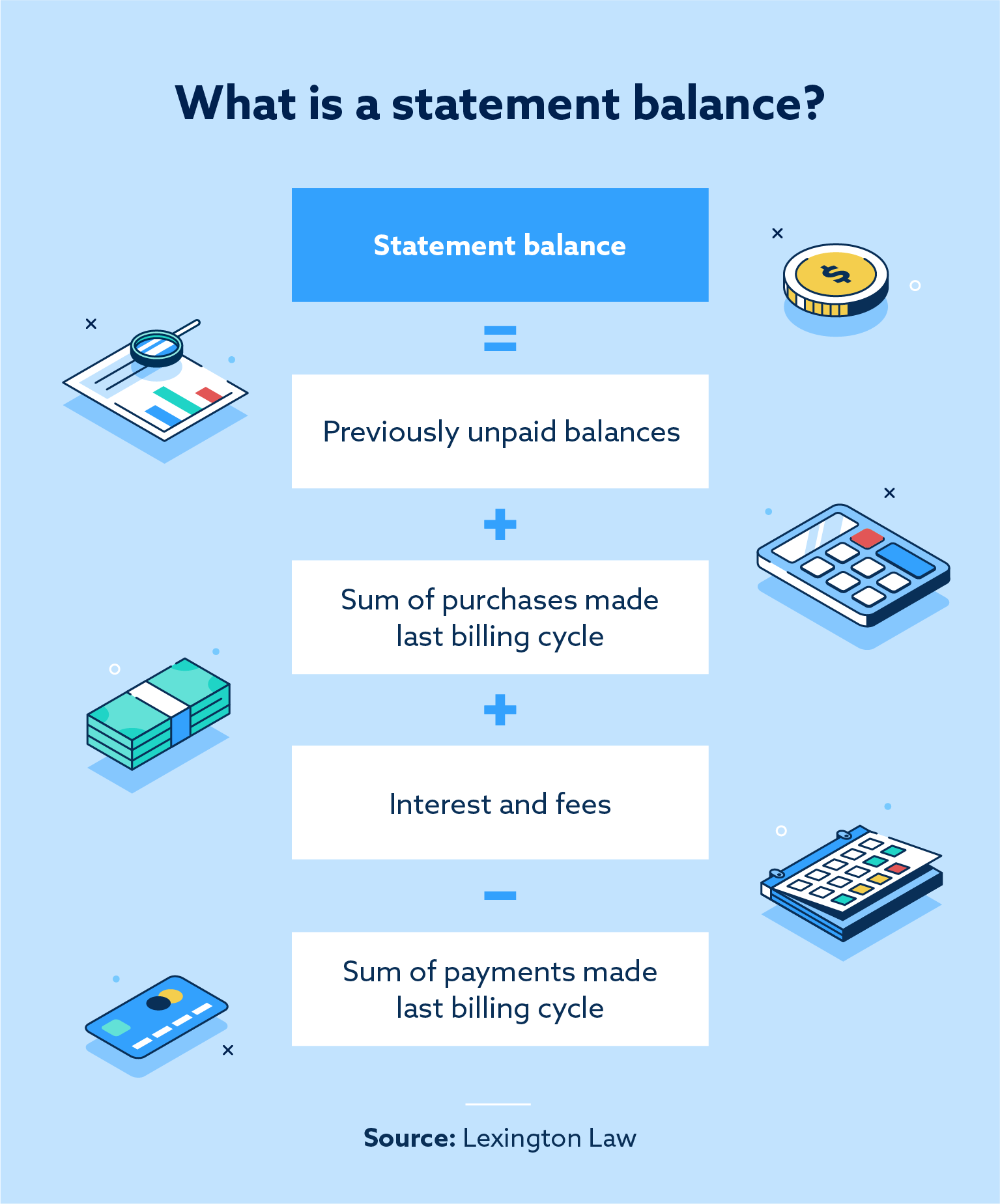

The statement balance is the total amount you owed on your credit card at the end of your last billing cycle. This is the figure that typically appears on your monthly credit card statement and is the amount you are generally expected to pay by the due date to avoid interest charges. It is a historical record, reflecting all transactions that posted to your account during that specific billing period.

For instance, if your billing cycle ends on the 15th of the month, your statement balance would reflect all purchases, payments, and credits that were processed and finalized between the 16th of the previous month and the 15th of the current month. This balance is crucial because it determines the minimum payment due and the full balance due to maintain a grace period.

The Current Balance: A Real-Time Picture

The current balance, on the other hand, is a dynamic figure that updates more frequently. It reflects all transactions that have posted to your account up to the present moment. This includes the statement balance from your last billing cycle, plus any new purchases or other charges that have occurred since then, minus any payments or credits that have been applied.

Imagine you made a purchase on your credit card after your last statement was generated. That purchase will not appear on your statement balance, but it will be reflected in your current balance. Similarly, if you’ve made a payment that has already been processed by the issuer, it will reduce your current balance. This real-time nature makes the current balance a more immediate indicator of your immediate financial commitment.

The Impact of Transactions on Your Current Balance

Every activity on your credit card account directly influences your current balance. Understanding how different types of transactions affect this figure is key to proactive financial management.

Purchases and New Charges

When you make a purchase using your credit card, the amount of that transaction is added to your current balance. This applies to everything from a small coffee to a significant appliance. The speed at which these charges appear in your current balance can vary. Some transactions, especially those made with major retailers, may post within a few hours, while others, particularly international transactions or those from smaller businesses, might take a day or two to appear.

It’s important to note that pending transactions might not always be immediately visible in your current balance. However, once a transaction has “posted” – meaning it has been officially recorded by the credit card issuer – it will be incorporated into your current balance. This distinction is crucial because while a pending transaction is an authorized charge, it hasn’t yet fully impacted your outstanding debt.

Payments and Credits

Conversely, when you make a payment to your credit card account, the amount of that payment reduces your current balance. The timing of when a payment affects your current balance depends on the payment method and the issuer’s processing times. Electronic payments, such as online bill pay or direct debit, are often the quickest to reflect, sometimes appearing within the same business day or the next.

Similarly, any credits applied to your account – for example, from a returned item or a promotional rebate – will also decrease your current balance. These credits function similarly to payments in reducing the amount you owe.

Fees and Interest Charges

Your current balance can also increase due to fees (such as late payment fees, annual fees, or foreign transaction fees) and interest charges. Interest charges are calculated based on your Average Daily Balance and your Annual Percentage Rate (APR). These charges are typically added to your account at the end of each billing cycle, but they contribute to the running total of your current balance from the moment they are incurred. Understanding how and when interest is applied is a vital aspect of managing your credit card debt effectively.

Why Tracking Your Current Balance Matters

The current balance is more than just a number; it’s a crucial metric that influences several aspects of your credit card usage and financial health.

Avoiding Overspending and Staying Within Limits

Monitoring your current balance helps you stay aware of your total debt. This awareness is critical for preventing overspending and ensuring you remain within your credit limit. Exceeding your credit limit can result in hefty fees and negatively impact your credit score. By regularly checking your current balance, you can make informed spending decisions and adjust your purchasing habits accordingly. For example, if your current balance is nearing your limit, you might decide to postpone a non-essential purchase until you can pay down some of the existing debt.

Strategic Payment Planning

Understanding your current balance is essential for planning your payments strategically. While the statement balance is what you generally need to pay by the due date to avoid interest, paying more than the statement balance and aiming to reduce your current balance can save you a significant amount in interest over time. If your current balance is substantially higher than your statement balance due to recent spending, you might consider making a payment that covers both the statement balance and a portion of the new charges to minimize future interest accrual.

Understanding Your Available Credit

Your current balance also directly impacts your available credit. Available credit is calculated by subtracting your current balance from your total credit limit. A lower current balance means higher available credit, which can be important for emergencies or unexpected expenses. Conversely, a high current balance reduces your available credit, potentially limiting your ability to make necessary purchases. Keeping a healthy gap between your current balance and your credit limit is a sign of responsible credit management.

Credit Utilization Ratio

The current balance plays a pivotal role in determining your credit utilization ratio, which is the amount of credit you are using compared to your total available credit. A lower credit utilization ratio (ideally below 30%) is beneficial for your credit score. Since your current balance is the numerator in this calculation, keeping it as low as possible directly improves your credit utilization ratio. This, in turn, can lead to a better credit score, making it easier to qualify for loans, mortgages, and other forms of credit in the future with more favorable terms.

Navigating Your Credit Card Statement and Online Tools

Credit card companies provide several tools to help you track your current balance. Familiarizing yourself with these resources will empower you to stay on top of your financial obligations.

The Credit Card Statement

As mentioned, your monthly credit card statement is a primary source of information. While it primarily features the statement balance, it will also usually provide a summary of recent activity that has affected your current balance since the statement was generated. Look for sections detailing new purchases, payments received, and any fees or interest accrued. Some statements may even provide an estimate of your current balance if you were to make a payment today.

Online Account Portals and Mobile Apps

Most credit card issuers offer online account portals and mobile applications that provide real-time access to your account information. These platforms are invaluable for tracking your current balance as it updates throughout the day. You can typically see a clear display of your current balance, available credit, recent transactions, and payment history. Many apps also offer features like spending trackers, budget tools, and payment reminders, further aiding in your financial management efforts. Utilizing these digital tools is often the most convenient and up-to-date way to monitor your credit card activity.

Customer Service

If you ever have questions or are unsure about any aspect of your current balance or other account details, don’t hesitate to contact your credit card issuer’s customer service. They can provide clear explanations, clarify transaction details, and offer assistance with managing your account.

In conclusion, understanding the current balance on your credit card is a cornerstone of responsible financial management. It’s a dynamic figure that reflects your real-time financial obligations, influencing your spending decisions, payment strategies, and overall credit health. By diligently tracking your current balance, utilizing the tools provided by your issuer, and making informed choices about your spending and payments, you can effectively navigate the world of credit and build a strong financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.