At its core, a budget is far more than just a restrictive financial straitjacket; it’s a meticulously crafted plan for your money, a roadmap that guides your income to its designated destinations. Far from being a tool of deprivation, budgeting is an act of empowerment, giving you conscious control over your financial destiny. It’s the essential framework that allows individuals, families, and businesses alike to understand where their money comes from, where it goes, and crucially, how to direct it towards their most important goals. In essence, a budget answers the fundamental question: “How can I make my money work for me?”

Without a budget, financial decisions often become reactive, driven by immediate desires or necessities rather than a cohesive strategy. This can lead to debt, missed opportunities for saving and investing, and a pervasive sense of financial anxiety. By embracing the principles of budgeting, you transition from passively observing your money disappear to actively allocating every dollar with purpose, turning aspirations into achievable realities. This article will delve into the profound meaning of budgeting, its indispensable role in personal and business finance, and practical approaches to implementing this transformative financial discipline.

The Core Concept: A Financial Roadmap

Understanding what a budget means begins with grasping its fundamental purpose: to provide clarity and control over your financial resources. It’s a forward-looking document that forecasts income and expenses over a specific period, typically a month, allowing you to make informed decisions about your spending and saving.

More Than Just Restraint: Empowering Your Spending

Many people associate budgeting with austerity, seeing it as a tedious exercise in cutting back and saying “no” to things they enjoy. This perception couldn’t be further from the truth. While a budget does involve making conscious choices about where your money goes, its primary function is to empower your spending. By clearly outlining your income and your fixed and variable expenses, a budget helps you identify areas where you can comfortably spend, save, or invest, aligning your financial actions with your values and goals. It’s about intentionality, ensuring that every dollar serves a purpose, whether it’s covering rent, building an emergency fund, or enjoying a well-deserved night out. It shifts the mindset from feeling restricted to feeling liberated by financial clarity.

The Dual Purpose: Tracking and Planning

A budget serves two critical, interconnected functions: tracking and planning. Tracking involves retrospectively observing where your money has gone. This often entails reviewing bank statements, credit card bills, and receipts to get an accurate picture of your past spending habits. This historical data is invaluable, revealing unconscious patterns and potential areas of waste. Without understanding your past spending, it’s incredibly difficult to plan for the future.

Once you have a clear understanding of your income and typical expenses, the planning aspect takes over. This is where you allocate your future income proactively. You decide in advance how much to spend on groceries, how much to save for retirement, and how much to allocate to discretionary items like entertainment or hobbies. This forward-thinking approach minimizes impulsive spending, ensures bills are paid on time, and systematically moves you closer to your financial objectives. The synergy between tracking and planning transforms abstract financial concepts into actionable steps, making your money management systematic and predictable.

Why Budgeting is Indispensable for Everyone

The benefits of budgeting extend far beyond simply knowing your bank balance. It’s a foundational practice that underpins almost every aspect of financial well-being, providing stability, control, and a clear path toward prosperity.

Achieving Financial Goals

One of the most compelling reasons to budget is to achieve your financial goals. Whether you dream of buying a house, saving for your child’s education, paying off student loans, taking a dream vacation, or retiring comfortably, a budget is the engine that drives these aspirations. It allows you to break down large, seemingly insurmountable goals into manageable monthly savings targets. By earmarking specific amounts of money for each goal, you ensure that progress is consistent and measurable. Without a budget, these goals often remain distant fantasies, perpetually pushed aside by everyday expenses and unplanned spending.

Gaining Financial Control and Reducing Stress

Few things are as stressful as feeling out of control with your finances. The anxiety of not knowing if you can cover an unexpected expense, the dread of checking your bank balance, or the uncertainty of your financial future can be debilitating. Budgeting directly addresses this by providing a comprehensive overview of your financial landscape. When you know precisely how much income you have, where it needs to go, and how much is left for discretionary spending or savings, you gain immense clarity and confidence. This control translates directly into reduced stress, allowing you to make financial decisions from a place of knowledge and power, rather than fear or guesswork.

Identifying and Eliminating Wasteful Spending

A budget acts as a financial magnifying glass, highlighting exactly where your money is going. Often, we spend money unconsciously on subscriptions we don’t use, coffees we could make at home, or impulse purchases that offer fleeting satisfaction. By categorizing and tracking expenses, you can easily identify these “money leaks”—areas where funds are being spent without providing commensurate value. Once identified, you can make informed decisions to reduce or eliminate these wasteful expenditures, reallocating those funds to more meaningful categories like savings, debt repayment, or even purposeful discretionary spending that brings genuine joy. This process not only saves money but also fosters a more mindful approach to consumption.

Building an Emergency Fund

Life is unpredictable, and unexpected expenses are an inevitable part of it, whether it’s a car repair, a medical bill, or a sudden job loss. An emergency fund is a critical financial safety net, typically covering three to six months of living expenses. Building such a fund requires consistent, dedicated savings, and a budget is the indispensable tool for achieving this. By designating a specific amount in your budget each month for your emergency fund, you systematically build this vital buffer, transforming potential crises into manageable inconveniences. Without a budget, saving for an emergency often falls by the wayside, leaving you vulnerable when unforeseen circumstances arise.

Key Components of an Effective Budget

To construct a robust and actionable budget, it’s essential to understand its fundamental building blocks. These components represent the inflows and outflows of your money, along with the strategies for managing them effectively.

Income: The Foundation

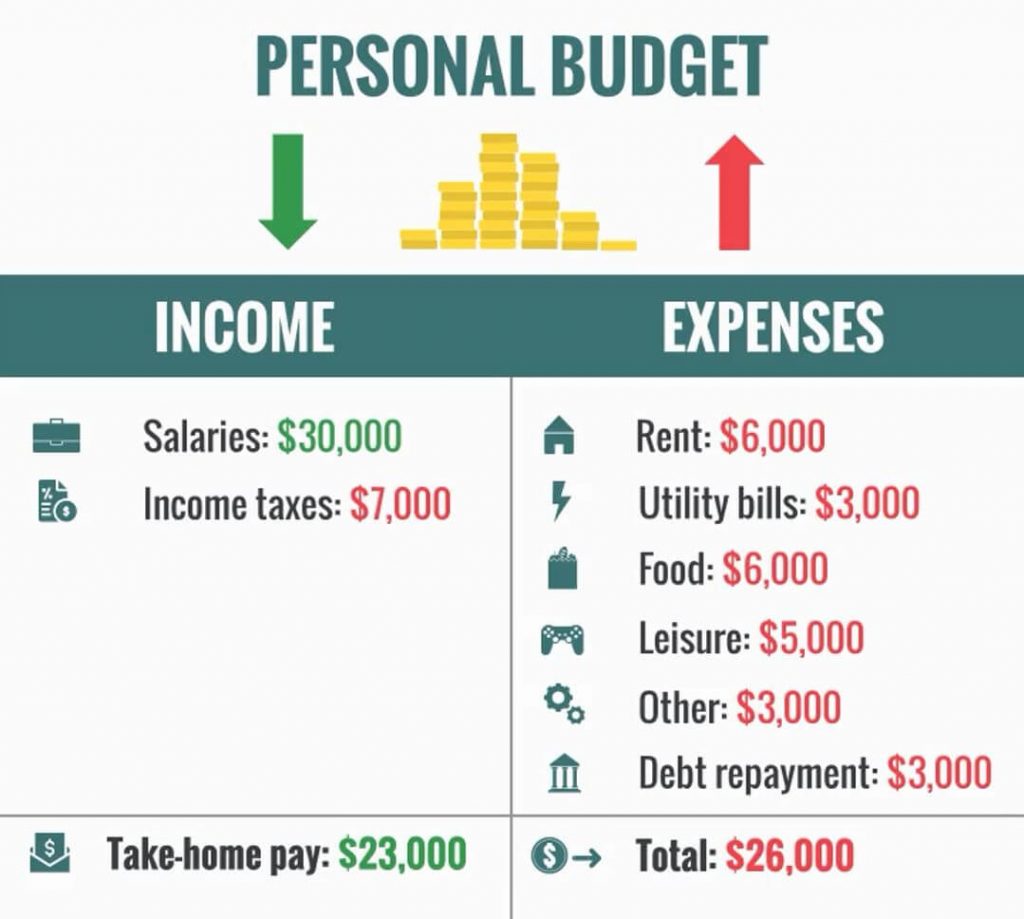

The starting point of any budget is a clear understanding of your income. This includes all money you receive, whether it’s your primary salary, wages from a side hustle, rental income, investment dividends, or benefits. It’s crucial to use your net income (the amount after taxes, deductions, and contributions like 401k are taken out), as this is the actual money you have available to spend and save. If your income varies (e.g., freelance work, commissions), it’s often wise to budget based on a conservative estimate or to average your income over several months to ensure you don’t over-allocate funds.

Expenses: Where Your Money Goes

Expenses are the outgoings—the money you spend. These are broadly categorized into two types:

- Fixed Expenses: These are expenses that typically remain the same amount each month and are relatively predictable. Examples include rent or mortgage payments, loan payments (car, student), insurance premiums, and many subscription services (Netflix, gym membership).

- Variable Expenses: These fluctuate from month to month and offer more flexibility for adjustment. Examples include groceries, utilities (electricity, water, gas, which can vary with usage), transportation costs (gas, public transit), entertainment, and dining out.

Understanding the distinction between fixed and variable expenses is vital because variable expenses are often the easiest to adjust when you need to cut costs or find extra money for savings. Furthermore, it’s helpful to distinguish between discretionary expenses (wants like entertainment, dining out, hobbies) and non-discretionary expenses (needs like housing, food, utilities, transportation to work).

Categories and Tracking

To effectively manage expenses, breaking them down into specific categories is essential. Instead of a lump sum for “spending,” categorize everything: housing, transportation, food, utilities, health, personal care, entertainment, savings, debt repayment, etc. This level of detail allows you to see precisely where your money is going within each area.

Consistent tracking is the backbone of budget maintenance. Whether you use a simple spreadsheet, a budgeting app, or even pen and paper, regularly recording and reviewing your expenses against your budgeted amounts is non-negotiable. This process reveals deviations, helps identify overspending in certain categories, and informs adjustments for future planning.

Savings and Debt Repayment: Prioritizing Your Future

A critical component of an effective budget is explicitly allocating funds for savings and debt repayment. These shouldn’t be treated as an afterthought or what’s left over at the end of the month. Instead, they should be treated as essential expenses, prioritized alongside your fixed bills. The “pay yourself first” principle advocates for setting aside money for savings (e.g., emergency fund, retirement, down payment) and debt reduction immediately after income is received. This ensures that your future financial well-being is consistently addressed, rather than hoping there’s money left over to save.

Popular Budgeting Methods and Approaches

There isn’t a one-size-fits-all approach to budgeting. What works for one person might not suit another. Understanding various methods allows you to choose the system that best aligns with your lifestyle, financial goals, and comfort level with tracking.

The 50/30/20 Rule

Popularized by Senator Elizabeth Warren, the 50/30/20 rule is a straightforward and highly adaptable budgeting framework. It suggests allocating your after-tax income as follows:

- 50% to Needs: This covers essential expenses like housing, utilities, groceries, transportation, and minimum loan payments.

- 30% to Wants: This category includes discretionary spending like dining out, entertainment, hobbies, vacations, and shopping for non-essentials.

- 20% to Savings & Debt Repayment: This portion is dedicated to building an emergency fund, saving for retirement or other long-term goals, and paying off any debt above the minimum payments.

The beauty of the 50/30/20 rule lies in its simplicity, making it an excellent starting point for those new to budgeting.

Zero-Based Budgeting

Zero-based budgeting (ZBB) is a more detailed and intensive method where every single dollar of your income is assigned a specific job. At the end of the month, your income minus your expenses, savings, and debt payments should equal zero. This doesn’t mean your bank account is empty; it means all your money has been purposefully allocated. For example, if you earn $4,000, you might assign $1,500 to rent, $500 to groceries, $300 to utilities, $400 to savings, $200 to debt repayment, $300 to entertainment, and so on, until all $4,000 is accounted for. ZBB provides maximum control and ensures that no money is left unaccounted for, often making it highly effective for quickly achieving financial goals like aggressive debt repayment.

Envelope System

The envelope system is a classic, tactile budgeting method that primarily uses cash. You designate physical envelopes for different variable spending categories (e.g., “Groceries,” “Dining Out,” “Entertainment”). At the beginning of the month (or paycheck), you withdraw cash and place the budgeted amount into each corresponding envelope. Once an envelope is empty, you stop spending in that category until the next budgeting period. This system is highly effective for visual and tactile learners and for those who struggle with overspending on credit cards, as it provides an immediate, tangible limit to spending.

Software and App-Based Budgeting

In the digital age, numerous financial tools and apps have revolutionized budgeting. Platforms like YNAB (You Need A Budget), Mint, Personal Capital, or Simplifi offer automated tracking by linking to your bank accounts and credit cards, categorizing transactions, and providing real-time insights into your spending. Many also offer goal tracking, bill reminders, and detailed reports. These tools are excellent for those who appreciate automation, visual data, and the convenience of managing their finances on the go, often integrating various accounts into a single dashboard for a holistic financial view.

Implementing and Maintaining Your Budget

A budget is not a static document; it’s a dynamic tool that requires consistent effort, review, and adjustment to remain effective. The true power of budgeting comes from its continuous application and adaptation.

Getting Started: Gathering Data and Setting Goals

The first step in implementing a budget is to gather all relevant financial data. This includes statements from all your income sources, bank accounts, credit cards, loan providers, and any recurring bills or subscriptions. Review at least 1-3 months of past spending to get an accurate picture of your actual expenses. Simultaneously, clearly define your financial goals. Are you saving for a down payment in two years? Do you want to pay off credit card debt by the end of next year? Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals will provide the motivation and direction for your budget.

Regular Review and Adjustment

A budget is a living document. It needs to be reviewed and adjusted regularly, ideally weekly or bi-weekly, and at least once a month. Life circumstances change: income can fluctuate, new expenses arise (e.g., a car repair, a new hobby), and old expenses may disappear. During your review, compare your actual spending against your budgeted amounts. Identify categories where you overspent or underspent and understand why. Then, make necessary adjustments for the upcoming period. This iterative process ensures your budget remains realistic, relevant, and an effective tool for achieving your goals. Don’t be afraid to tweak it; flexibility is key to long-term success.

Dealing with Unexpected Expenses

Even with the best planning, unexpected expenses will occur. This is precisely why building an emergency fund, as a core component of your budget, is so critical. When an unforeseen cost arises, draw from your emergency fund rather than derailing your entire budget or accumulating new debt. If your emergency fund is still growing, your budget allows you to quickly identify areas where you can temporarily cut back (e.g., reduce discretionary spending) to cover the unexpected cost without jeopardizing your essential needs or long-term goals. The budget provides the structure to pivot and adapt without financial panic.

Staying Consistent and Patient

Budgeting is a habit, and like all habits, it takes time, discipline, and patience to cultivate. You won’t master it overnight, and there will be months when you go off track. The key is not to get discouraged but to learn from each instance and recommit to the process. Consistency is more important than perfection. Stick with your chosen method, track diligently, review regularly, and celebrate small victories. Over time, budgeting will become second nature, transforming your relationship with money and paving the way for lasting financial health and freedom.

In conclusion, “what does budget mean” unpacks a concept that is foundational to financial well-being. It is a powerful, personalized financial roadmap that enables individuals and organizations to understand, control, and optimize their money. By providing clarity on income and expenses, facilitating goal achievement, reducing stress, and fostering financial discipline, budgeting transforms an often daunting aspect of life into an empowering journey towards financial freedom and peace of mind. Start your budget today, and take the first step towards a more secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.