In the complex ecosystem of the financial world, few transactions are as significant—or as paperwork-intensive—as the residential mortgage. For the average borrower, the face of the transaction is often the Loan Officer or the Real Estate Agent. However, behind the scenes, a critical engine drives the entire process toward the finish line: the Mortgage Loan Processor.

As a cornerstone of the business finance and personal lending sector, the loan processor is the bridge between a borrower’s aspirations and a lender’s risk management. This role requires a meticulous eye for detail, a deep understanding of financial documentation, and the ability to navigate a highly regulated environment. Whether you are a homebuyer curious about who is handling your sensitive data or a professional looking for a stable career in the money sector, understanding the intricacies of mortgage loan processing is essential.

The Core Responsibilities of a Mortgage Loan Processor

At its most basic level, a mortgage loan processor is responsible for preparing a borrower’s loan file and ensuring it is “underwriting-ready.” While the Loan Officer (LO) focuses on sales and initial consultation, the processor focuses on the logistics and the “proof.”

Document Verification and Collection

The primary task of a processor is to gather the “Big Three” of mortgage documentation: income, assets, and credit. This is not as simple as checking a box. A processor must examine W-2s, pay stubs, and tax returns to ensure the income reported matches the figures used in the initial application. In the world of personal finance, discrepancies are common, and it is the processor’s job to resolve them before the file reaches the underwriter.

Ensuring Regulatory Compliance

Mortgage lending is one of the most heavily regulated industries in the world. Processors must ensure that every file adheres to federal regulations such as the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA). They ensure that disclosures are sent within legal timeframes and that the file contains all necessary consumer protections. This layer of the job protects both the financial institution and the borrower from legal and financial repercussions.

Liaising Between Borrowers and Underwriters

The processor acts as a diplomatic envoy. Underwriters are the “judges” of the mortgage world, deciding whether to approve or deny a loan based on risk. The processor anticipates the underwriter’s questions and works with the borrower to provide the necessary explanations or “Letters of Explanation” (LOEs). This proactive approach prevents the file from being stuck in a loop of endless “conditions.”

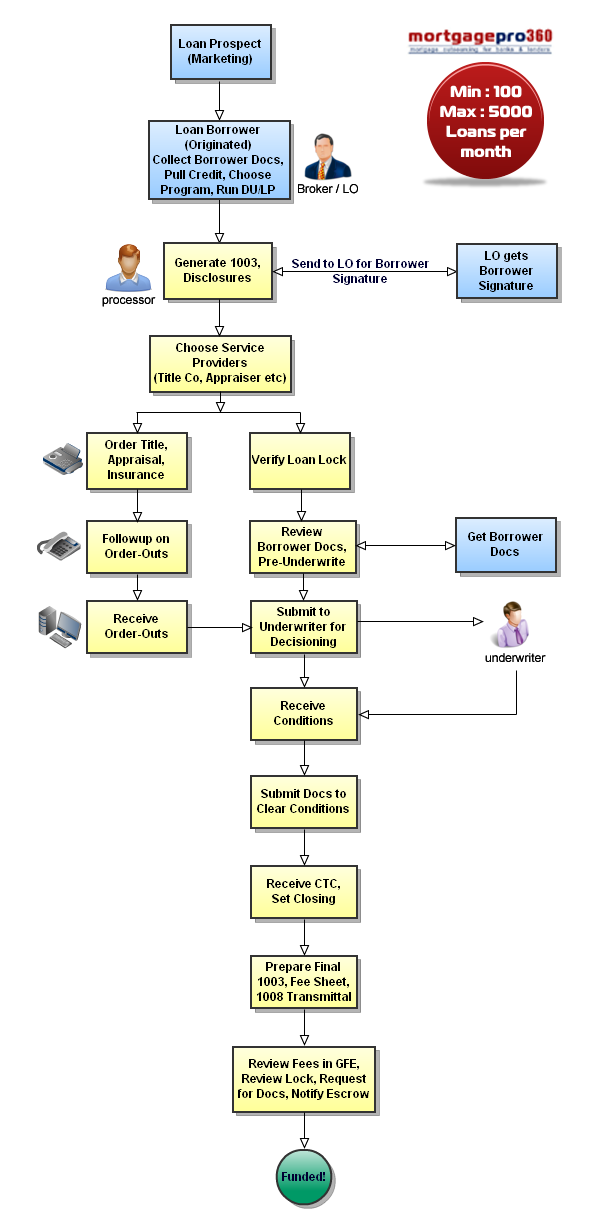

The Mortgage Workflow: From Application to Closing

To understand what a processor does, one must look at the timeline of a real estate transaction. The processor typically takes over the file once a borrower has found a home and signed a purchase contract, though they may also work on pre-approvals.

Initial File Review and Setup

Once the Loan Officer hands over the file, the processor performs a “scrub.” They verify that the application (the 1003 form) is complete and that the borrower’s Social Security number, employment history, and address history are accurate. During this phase, they will pull a fresh credit report if necessary and verify that the loan program (FHA, VA, Conventional) aligns with the borrower’s financial profile.

Third-Party Service Coordination

A mortgage involves more than just the lender and the borrower. It requires a village of third-party vendors. The processor is responsible for ordering:

- The Appraisal: Ensuring a licensed professional evaluates the property’s value.

- Title Insurance: Verifying that the property is free of liens or legal disputes.

- Verifications of Employment (VOE): Contacting employers to confirm the borrower is still employed.

- Homeowners Insurance: Ensuring the asset is protected before the loan is funded.

The Transition to Underwriting and “Clearing Conditions”

After the initial paperwork is assembled, the processor submits the file to the underwriter. The underwriter will issue a “Conditional Approval.” This is a list of items still needed to finalize the loan—perhaps a more recent bank statement or a clarification on a large deposit. The processor spends the bulk of their time “clearing conditions,” working tirelessly to move the file from “Approved with Conditions” to “Clear to Close” (CTC).

Essential Skills and Qualifications for Success in Loan Processing

The role of a mortgage loan processor is not just about data entry; it is a high-stakes position that requires a specific financial and interpersonal toolkit.

Attention to Detail and Organizational Mastery

In mortgage finance, a single digit can be the difference between an approval and a denial. A processor must be able to spot an expired insurance policy or a missing signature on page 14 of a 30-page tax return. Because they often manage 20 to 40 files simultaneously, their organizational systems must be impeccable. Each file has a strict deadline (the closing date), and missing that date can result in financial penalties for the borrower or even the loss of the home.

Understanding Financial Statements and Tax Returns

A successful processor must have a firm grasp of business finance principles, especially when dealing with self-employed borrowers. Analyzing a Schedule C or a K-1 to determine “qualifying income” requires a level of financial literacy that goes beyond basic math. They must understand how depreciation, business expenses, and capital gains affect a borrower’s debt-to-income (DTI) ratio.

Communication and Soft Skills

While the role is highly technical, it is also deeply human. Borrowers are often stressed, as buying a home is frequently the largest financial decision of their lives. A processor must be able to explain complex financial requirements in plain English, providing reassurance while maintaining the professional boundaries required by the bank or lending institution.

Career Outlook: Salary, Education, and Path to Advancement

For those looking to enter the “Money” sector, mortgage loan processing offers a robust career path with significant earning potential and stability.

Entry Requirements and Certifications

Most entry-level processing positions require a high school diploma, but an associate or bachelor’s degree in finance, business, or accounting is highly preferred in today’s market. While not always mandatory, many processors seek certification through the National Association of Mortgage Processors (NAMP). In some states, if a processor is an independent contractor rather than an employee of a bank, they may be required to obtain an NMLS (Nationwide Multistate Licensing System) license.

Potential Earnings and Remote Work Opportunities

The financial compensation for processors is often a mix of a base salary and “per-file” bonuses. This structure incentivizes efficiency and volume. According to industry data, experienced processors can earn anywhere from $50,000 to $90,000 annually, with top-tier professionals in high-volume markets exceeding six figures. Furthermore, the digital transformation of the finance industry has made loan processing one of the most common remote-friendly roles in banking.

Moving Up: From Processor to Underwriter or Loan Officer

Loan processing is often seen as the “proving ground” for higher-level finance roles. Many processors eventually transition into underwriting, where they take on the final decision-making authority for loan approvals. Others, who prefer the sales and networking side of the business, move into the Loan Officer role. The deep technical knowledge gained as a processor makes these individuals highly effective in any area of the mortgage industry.

Why the Mortgage Processor is the Hero of the Real Estate Transaction

In the grand narrative of personal finance, we often celebrate the moment the keys are handed over. We credit the agent who found the house or the bank that provided the funds. However, the mortgage loan processor is the silent architect who ensured the foundation of the deal was solid.

By meticulously verifying data, navigating the labyrinth of federal regulations, and managing the expectations of multiple parties, the processor protects the integrity of the financial system. They ensure that lenders are making sound investments and that borrowers are not taking on debt they cannot afford. In a world where financial transparency is paramount, the mortgage loan processor stands as a guardian of accuracy and a facilitator of the American dream of homeownership.

For anyone interested in the intersection of business finance, personal stability, and organizational excellence, the role of a mortgage loan processor is not just a job—it is a vital, high-impact career in the ever-evolving world of money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.