For most individuals, the purchase of a home is the most significant financial transaction of their lifetime. Central to this transaction is a stack of legal documents that can often feel overwhelming and impenetrable. Among these, the mortgage deed stands as one of the most critical. While many people use the terms “mortgage” and “deed” interchangeably, they represent distinct financial and legal concepts. Understanding what a mortgage deed looks like, what it contains, and how it functions is a vital component of financial literacy for any homeowner or real estate investor.

In its simplest form, a mortgage deed is a formal document that creates a lien on a property as security for a loan. It is the “security instrument” that gives the lender the right to seize the property if the borrower fails to meet the repayment terms. Below, we break down the anatomy of this document, the essential clauses it contains, and how it differs from other real estate paperwork.

The Anatomy of a Mortgage Deed: Physical and Structural Layout

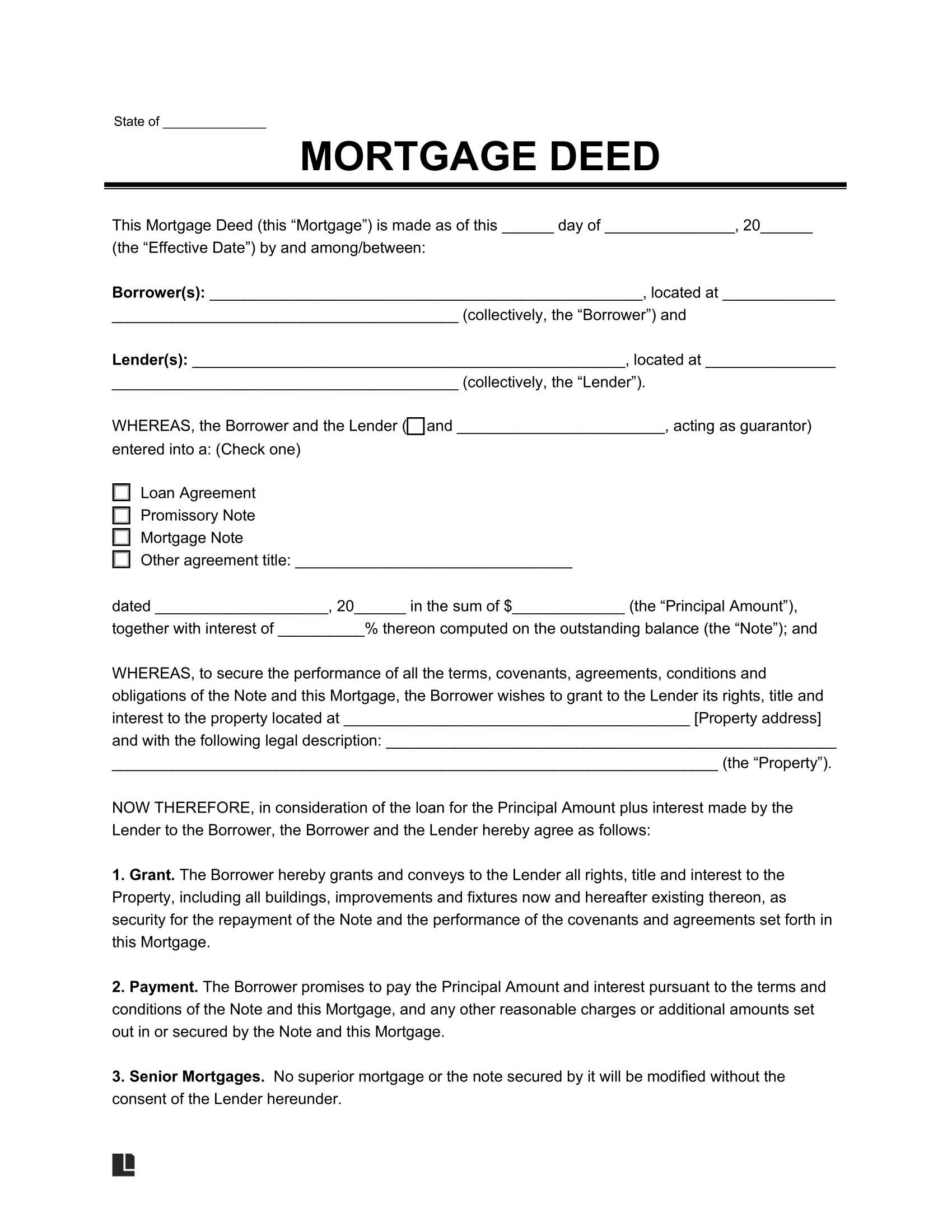

When you first view a mortgage deed, you will notice it is a formal, multi-page document—typically ranging from 15 to 40 pages depending on the state and the complexity of the loan. In the modern era, most mortgage deeds follow standardized formats set by government-sponsored entities like Fannie Mae and Freddie Mac. This standardization ensures consistency across the financial markets.

Identifying the Parties Involved

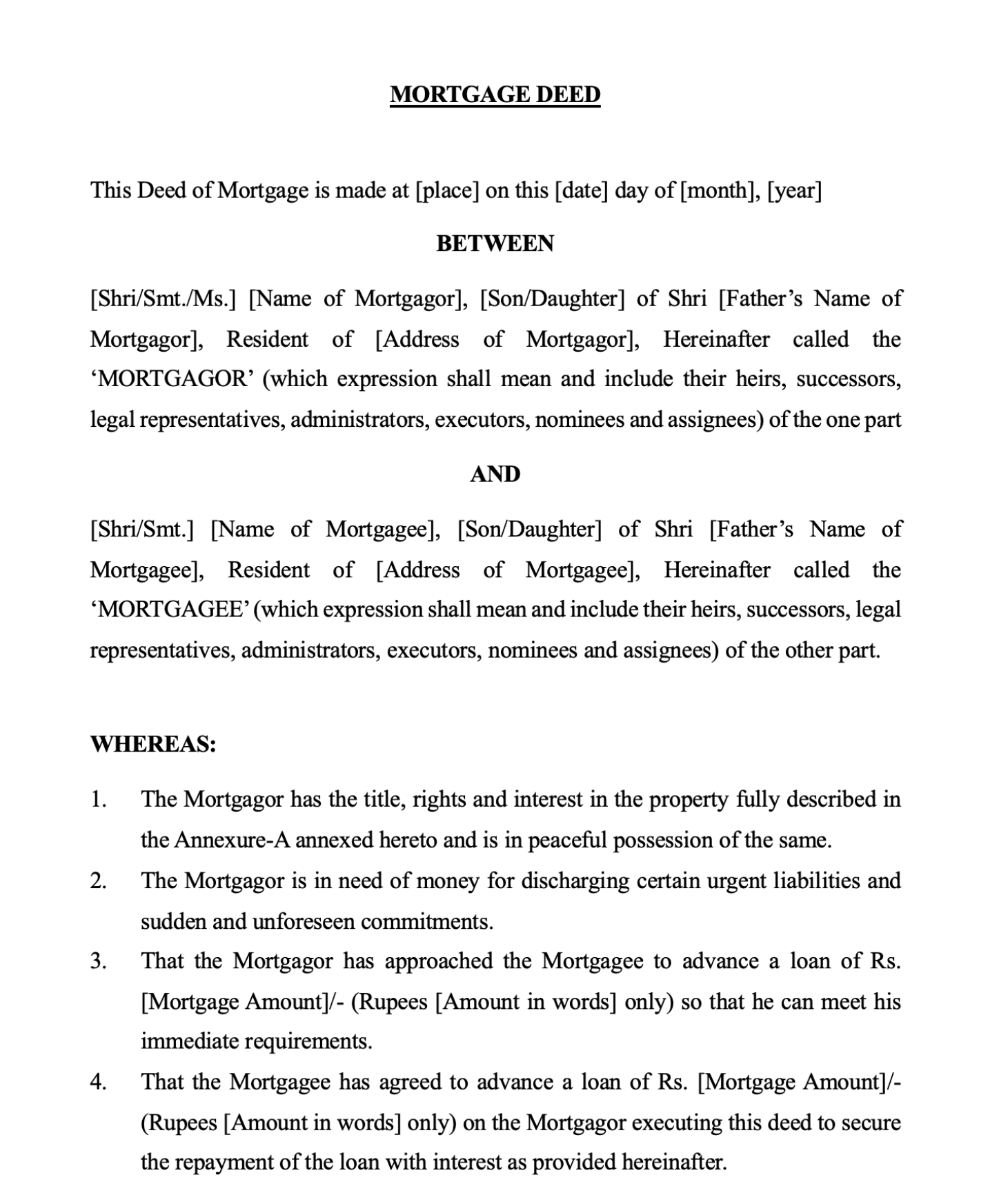

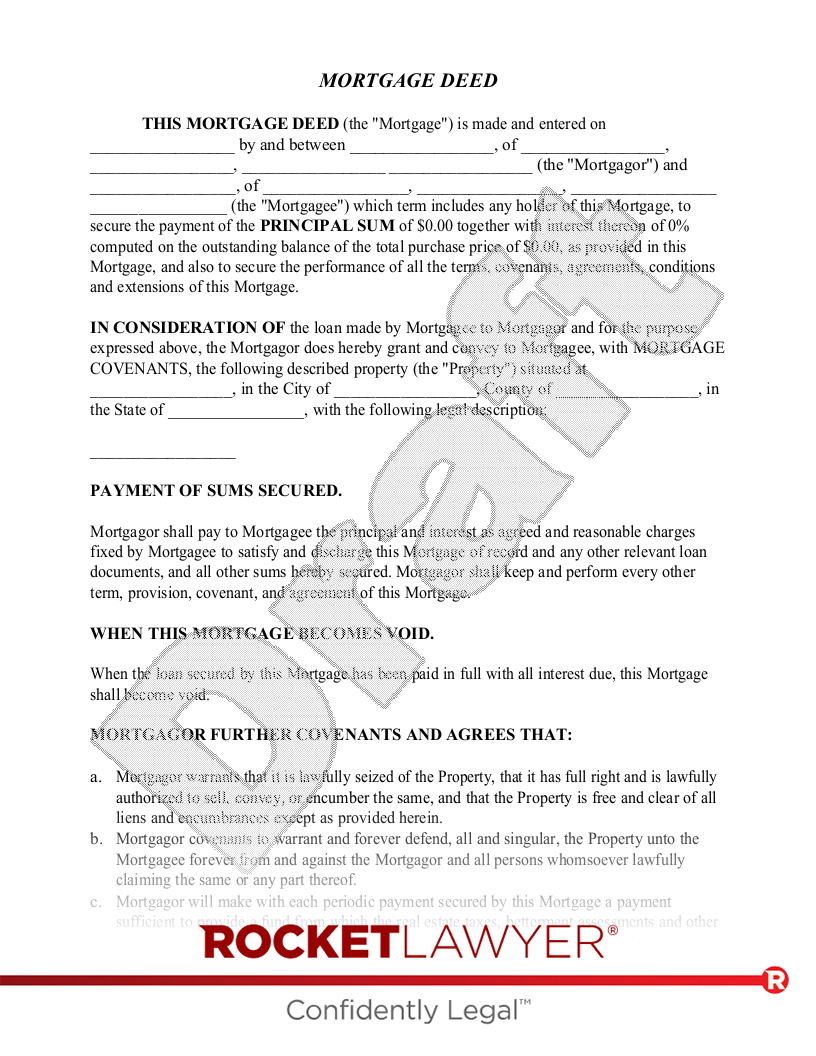

The first page of a mortgage deed clearly identifies the legal entities entering the agreement. You will see the “Mortgagor” and the “Mortgagee.” In the world of personal finance, it is a common point of confusion: the Mortgagor is the borrower (the homeowner), and the Mortgagee is the lender (the bank or financial institution). The document will list the full legal names and addresses of both parties.

The Legal Property Description

Unlike a standard mailing address, a mortgage deed requires a “legal description” of the property. This is a precise geographical identifier that might include lot numbers, block numbers, and metes and bounds. This section ensures there is no ambiguity regarding exactly which asset is being used as collateral for the financial obligation. You will usually find this in the early pages or attached as an “Exhibit A.”

The Granting Clause

This is the “meat” of the document from a financial perspective. The granting clause states that the borrower is “granting, bargaining, selling, and conveying” the property to the lender (or a trustee) specifically for the purpose of securing the debt. It establishes the lender’s security interest in the home, which is the foundational element of real estate lending.

Essential Clauses Every Homeowner Should Recognize

Beyond the basic identification of the property and the parties, the mortgage deed contains several “covenants” or promises. These are the rules of the financial engagement. If you are managing your personal finances, these are the sections that dictate your risks and responsibilities.

The Acceleration Clause

Perhaps the most significant clause in the entire document is the acceleration clause. This provision states that if the borrower breaches the contract—most commonly by missing payments—the lender has the right to “accelerate” the loan. This means the entire remaining balance of the mortgage becomes due immediately. Understanding this clause is essential for risk management, as it is the precursor to the foreclosure process.

Covenants of Maintenance and Insurance

From a lender’s perspective, the house is their collateral. Therefore, the mortgage deed will look like a set of instructions on how to care for that collateral. You will find clauses requiring the borrower to maintain “hazard insurance” and to keep the property in good repair. If the borrower fails to pay property taxes or insurance, the deed typically allows the lender to pay these costs themselves and add them to the loan balance—a process known as “force-placed insurance” or “advances.”

The Due-on-Sale Clause

In the context of personal finance and investing, the due-on-sale clause is critical. It specifies that if the property is sold or transferred to a new owner, the lender can demand full payment of the remaining loan balance. This prevents a buyer from “assuming” a low-interest rate mortgage from a seller without the lender’s explicit approval.

Mortgage Deed vs. Title Deed: Understanding the Financial Nuance

One of the most common misconceptions in personal finance is the difference between a mortgage deed and a title deed. While they are often signed at the same closing table, they serve diametrically opposed purposes.

Ownership vs. Debt

A Title Deed (or Grant Deed/Warranty Deed) is the document that proves ownership. It transfers the “title” of the property from the seller to the buyer. If you hold the title deed, you are the legal owner of the property.

A Mortgage Deed, on the other hand, is a document representing a debt. It does not prove you own the home; rather, it proves that you owe money on the home and have pledged the home as collateral. While the title deed says “This house belongs to you,” the mortgage deed says “If you don’t pay the bank back, the bank can take the house.”

The Concept of a Lien

In the eyes of a financial auditor or a title searcher, the mortgage deed acts as a “lien.” It is a public notice that there is a financial “cloud” or encumbrance on the property. As long as the mortgage deed is active, the owner cannot sell the property and walk away with the full proceeds without first satisfying the debt to the mortgagee.

The Recording Process and Legal Validity

A mortgage deed is not just a private contract between two parties; it is a public record. For the lender’s financial interest to be protected against other creditors, the deed must be “perfected.”

The Role of the County Recorder

After the closing documents are signed and notarized, the mortgage deed is sent to the local County Recorder’s Office or Register of Deeds. The clerk stamps the document with a book and page number (or a digital instrument number) and enters it into the public land records. This “recording” provides constructive notice to the world that the lender has a primary financial interest in the property.

Priority of Liens

In the world of investing and business finance, the date of recording is paramount. Generally, the first mortgage deed recorded has “seniority.” If the borrower goes bankrupt or the property is foreclosed upon, the “first” mortgage holder is paid before any subsequent “second” mortgages or home equity lines of credit (HELOCs). This hierarchy of debt is established entirely by the chronological order in which the mortgage deeds were filed.

The Digital Evolution: The Shift to E-Deeds in Modern Finance

As technology reshapes the financial sector, the physical “look” of a mortgage deed is changing. Historically, these were heavy, parchment-style documents with embossed seals. Today, we are seeing the rise of the “e-Note” and the electronic mortgage deed.

Electronic Signatures and Notarization

Many jurisdictions now allow for Remote Online Notarization (RON). In these cases, the mortgage deed exists as a secure PDF or a blockchain-verified file. While the language and legal clauses remain the same as their paper counterparts, the “look” is now a digital interface with encrypted digital signatures. For the modern homeowner, this means their “original” mortgage deed might never exist in physical form, but rather as a secure entry in a digital vault (such as the MERS—Mortgage Electronic Registration System).

Transparency and Accessibility

Digital deeds make it significantly easier for homeowners to monitor their financial standing. Through online banking portals, borrowers can often view a scanned copy of their recorded deed, allowing them to verify the terms of their interest rate, their escrow obligations, and their legal descriptions without having to visit a county courthouse.

Conclusion: Why the Mortgage Deed Matters to Your Financial Future

Understanding what a mortgage deed looks like—and more importantly, what it signifies—is a cornerstone of sound personal financial management. It is more than just a 30-page document signed in a blur of excitement on closing day. It is the legal framework that governs your largest debt and protects your largest asset.

By recognizing the specific clauses regarding acceleration, maintenance, and the due-on-sale provision, you can navigate your homeownership journey with greater confidence. Whether you are a first-time buyer or a seasoned real estate investor, treating the mortgage deed as a vital financial tool rather than just “paperwork” ensures that you remain in control of your property and your financial destiny. Always remember: the title deed gives you the keys, but the mortgage deed sets the rules for how you keep them.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.