In the world of business finance, intuition is a valuable asset, but data is the ultimate arbiter of success. For a business planner, whether they are launching a high-growth startup or managing an established enterprise, the “Break-Even Analysis” serves as the most critical reality check in their financial toolkit. At its core, a break-even analysis determines the exact point at which total costs and total revenues are equal, resulting in a net profit of zero. While that might sound like a modest goal, the insights derived from this calculation go far beyond a simple zero-sum game.

For a business planner, the break-even analysis is a navigational instrument. It transforms abstract goals into concrete operational targets. It answers the fundamental question of viability: “Is this business model sustainable?” By stripping away the complexities of market sentiment and focusing on unit economics, the break-even analysis provides a roadmap for pricing, cost management, and long-term financial health.

Defining the Break-Even Point: The Foundation of Financial Planning

Before a planner can use a break-even analysis to make strategic decisions, they must understand the components that feed the formula. In business finance, not all expenses are created equal. The distinction between fixed and variable costs is the bedrock upon which the entire analysis is built.

Understanding Fixed vs. Variable Costs

A business planner must categorize every cent leaving the company. Fixed costs, often referred to as “overhead,” are expenses that do not change regardless of how much a company produces or sells. These include rent, insurance, administrative salaries, and equipment leases. They represent the “barrier to entry” that must be overcome every single month.

Variable costs, on the other hand, fluctuate in direct proportion to production volume. This includes raw materials, direct labor, shipping costs, and sales commissions. A business planner looks at these costs to determine the “marginal cost” of selling one additional unit. If the variable costs are too high relative to the selling price, the business may find itself in a position where it loses money on every sale—a recipe for immediate insolvency.

The Mathematical Formula and the Unit Perspective

The break-even point is typically calculated using the formula:

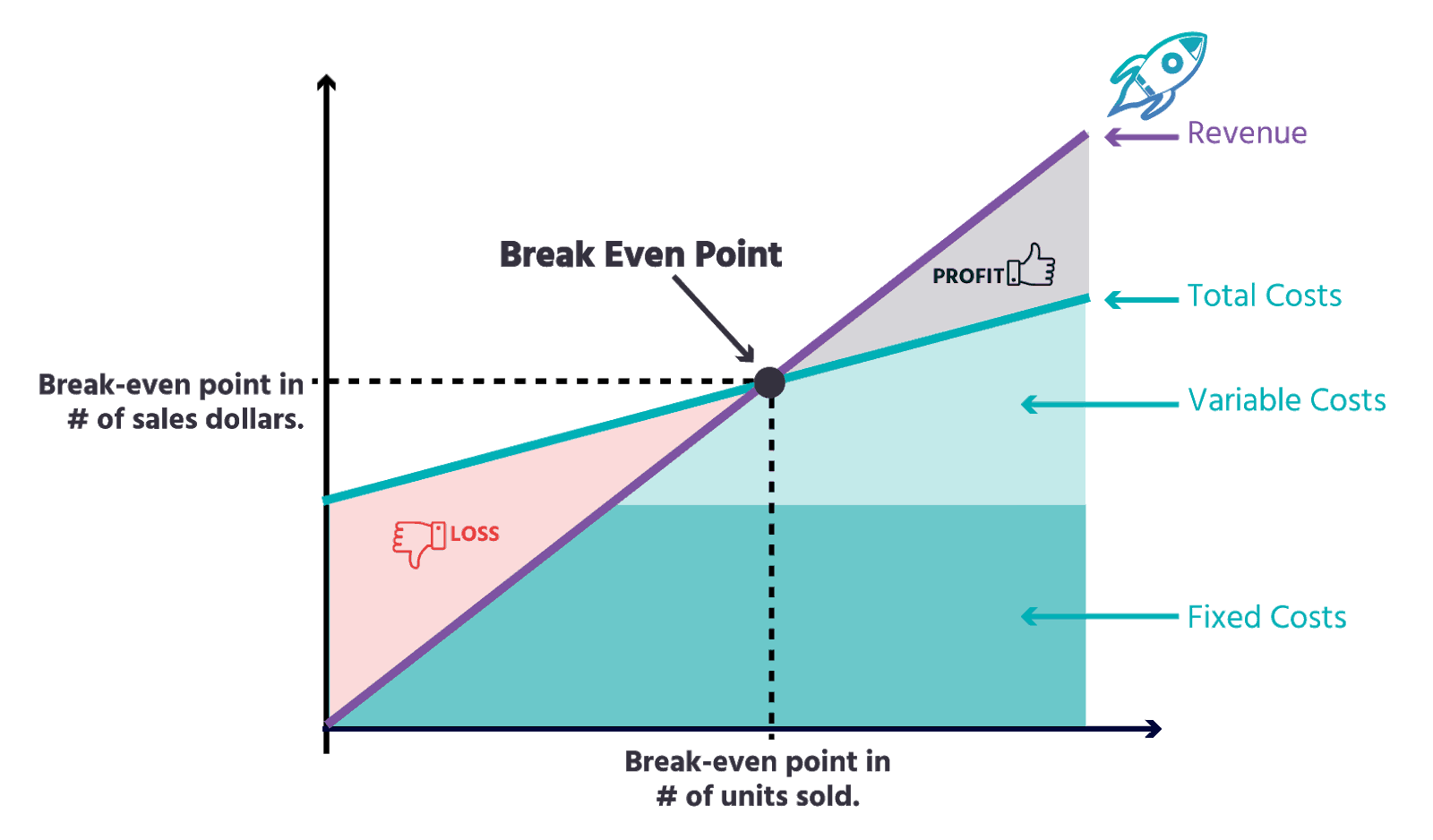

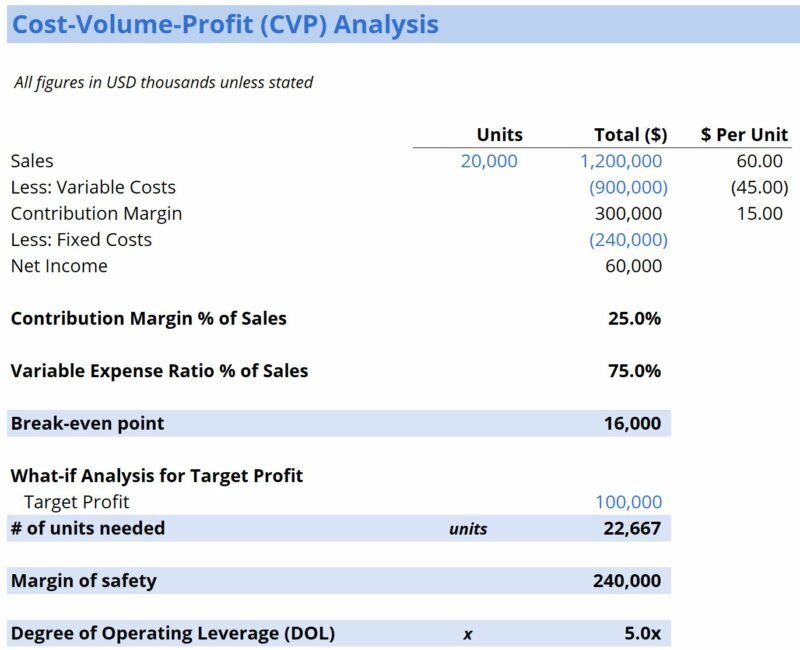

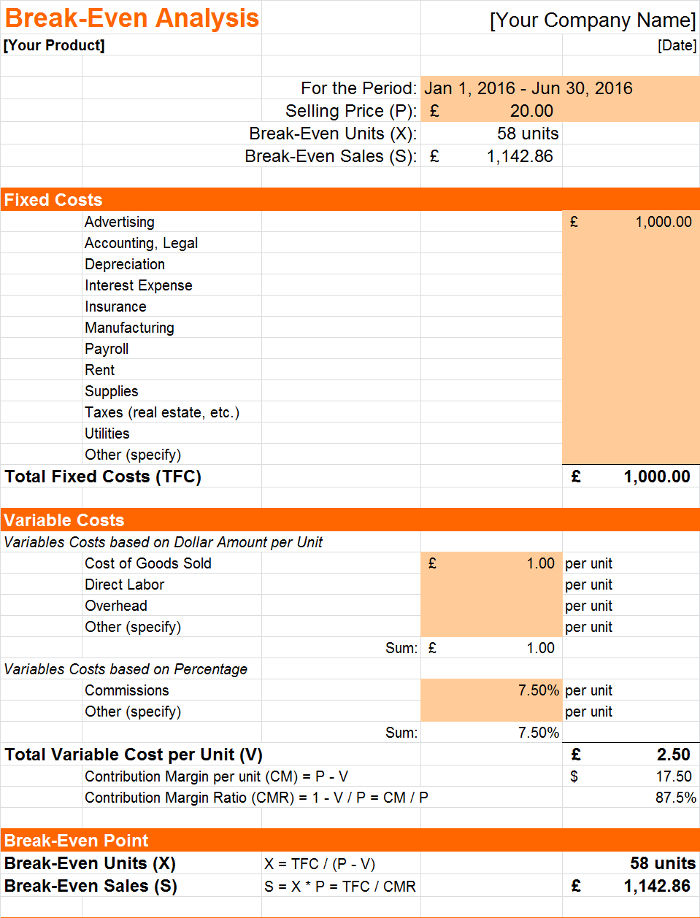

Break-Even Point (Units) = Fixed Costs / (Sales Price per Unit – Variable Cost per Unit).

The denominator—Sales Price minus Variable Cost—is known as the Contribution Margin. This is arguably the most important figure a business planner monitors. It represents the portion of each sale that “contributes” to covering fixed costs. Once those fixed costs are fully covered, every subsequent dollar of contribution margin flows directly into the net profit column. By looking at this formula, a planner can immediately see how a slight reduction in material costs or a small increase in price can exponentially accelerate the timeline to profitability.

Assessing Viability and Risk Management

The most immediate value of a break-even analysis to a business planner is its ability to quantify risk. Every new project or business venture carries an inherent level of uncertainty. A break-even analysis provides a “Margin of Safety,” which is a financial cushion that tells the planner how much sales can drop before the company begins to lose money.

Determining the Margin of Safety

For a financial planner, the Margin of Safety is the difference between the projected sales volume and the break-even volume. If a company projects sales of 10,000 units but the break-even point is 9,500 units, the margin is dangerously thin. A minor market downturn, a supply chain disruption, or an aggressive move by a competitor could push the business into the red.

Conversely, a wide Margin of Safety indicates a robust business model that can withstand economic volatility. Business planners use this metric to decide whether to proceed with a project or to go back to the drawing board to find ways to lower fixed overhead or improve the contribution margin.

Evaluating Potential Profitability Before Launch

A break-even analysis serves as a “litmus test” for feasibility. If the analysis reveals that a business must capture 80% of the total available market just to break even, the business planner will likely deem the venture too risky. By comparing the break-even volume to historical market data and competitor performance, the planner can determine if the sales targets are realistic. This prevents the common financial pitfall of “optimism bias,” where planners overestimate demand while underestimating the costs required to meet that demand.

Optimizing Pricing Strategies and Profit Margins

Pricing is often the most difficult lever for a business to pull. Set prices too high, and you lose volume; set them too low, and you may never cover your costs. A break-even analysis provides the data-driven framework needed to find the “sweet spot” in pricing strategy.

The Impact of Price Changes on Volume Requirements

A business planner uses break-even analysis to conduct “What-If” scenarios. For instance, if the marketing team suggests a 10% price cut to gain market share, the planner can quickly calculate how much volume must increase to maintain the same financial position.

If a 10% price cut requires a 40% increase in sales volume just to reach the same break-even point, the planner might conclude that the strategy is inefficient. On the other hand, if a premium pricing strategy allows the company to break even at only 30% capacity, the planner may advocate for a “low volume, high margin” model, which often carries less operational stress and higher long-term brand value.

Understanding the Contribution Margin Ratio

Beyond unit sales, the break-even analysis helps planners understand the Contribution Margin Ratio (Contribution Margin / Sales). This ratio tells the planner how much of every dollar in revenue is available to pay for fixed expenses. In multi-product businesses, this is vital. A planner might find that “Product A” has a high sales volume but a low contribution margin, while “Product B” has a lower volume but a much higher margin. This insight allows the planner to reallocate resources toward the most profitable products, optimizing the company’s overall financial health rather than just chasing top-line revenue.

Strategic Decision-Making and Resource Allocation

Strategic planning is essentially the art of allocating scarce resources to their most productive uses. A break-even analysis provides the financial justification for capital expenditures and operational changes.

Scaling and Growth Projections

When a business decides to scale—perhaps by opening a new location or investing in a new production line—its fixed costs will inevitably rise. A business planner uses a break-even analysis to project how this “step-up” in fixed costs will affect the company’s risk profile.

They must ask: “How many more units must we sell to justify this $500,000 investment in automation?” If the new technology reduces variable costs (like labor) significantly, the break-even point might actually drop in the long run, even though fixed costs increased. This type of deep financial modeling is what separates successful growth from reckless over-expansion.

Cost Control and Operational Efficiency

The break-even analysis also acts as a diagnostic tool for internal efficiency. If the break-even point is rising over time, it indicates that either fixed costs are “creeping” upward or variable costs are eroding the margin. A business planner can use this information to trigger a cost audit.

By analyzing the components of the break-even point, the planner can identify specific areas for improvement. Is the rent too high for the current revenue level? Are raw material prices increasing faster than the company can raise prices? By focusing on the “break-even” as a Key Performance Indicator (KPI), the planner ensures that the organization remains lean and focused on bottom-line results.

Navigating Future Uncertainties: Why Every Business Planner Needs a Break-Even Review

In an era of economic flux, the break-even analysis is not a “one-and-done” exercise. It is a living document that must be revisited quarterly, if not monthly. It tells the business planner exactly where the “floor” is, allowing the executive team to make bold moves with the confidence that they understand their downside risk.

Ultimately, a break-even analysis tells a business planner how much room they have to play with. It identifies the point where a “hobby” or a “project” becomes a “business.” By mastering the relationship between costs, volume, and price, the planner moves from guesswork to precision. They can provide the board of directors, investors, or stakeholders with a clear, mathematically sound justification for the company’s strategic direction.

In the final assessment, the break-even analysis is about more than just surviving; it is about creating a springboard for sustainable profit. It provides the clarity needed to navigate the complexities of business finance, ensuring that every dollar spent is a deliberate step toward long-term fiscal stability and success. For any business planner, ignoring the break-even point is like flying a plane without an altimeter—you might feel like you’re soaring, but you won’t know how close you are to the ground until it’s too late. Master the break-even, and you master the financial destiny of the enterprise.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.