Tax season, for many, can feel like a daunting annual pilgrimage through a labyrinth of forms, receipts, and financial jargon. Far from being just an obligation, it’s an annual opportunity to review your financial health, ensure compliance, and potentially reclaim funds through deductions and credits. The key to transforming this often-stressful period into a manageable, even empowering, experience lies in proactive preparation. Understanding precisely what you need, and why, can significantly streamline the process, reduce errors, and ensure you make the most of every allowable benefit. This comprehensive guide will walk you through the essential documents, information, and strategies required to approach tax season with confidence, whether you’re a seasoned filer or embarking on your first tax journey. From foundational personal details to intricate financial statements, and from choosing your filing method to adopting robust record-keeping habits, we’ll uncover the building blocks of a successful tax filing experience, strictly within the realm of personal and business finance.

The Foundation: Gathering Your Personal and Prior Year Information

Before diving into the complexities of income and expenses, the groundwork for your tax return begins with basic personal identification and a look back at your previous filings. These initial steps are critical for accurate reporting and continuity.

Essential Personal Details

Your tax return is uniquely tied to your identity and household structure. The first items on your checklist should always include:

- Social Security Numbers (SSNs) or Individual Taxpayer Identification Numbers (ITINs): For yourself, your spouse (if filing jointly), and all dependents you plan to claim. Accuracy here is paramount, as discrepancies can lead to significant delays and complications with the IRS or your local tax authorities.

- Dates of Birth: For yourself, spouse, and dependents. This helps determine eligibility for certain credits, such as the Child Tax Credit or certain education benefits.

- Current Address: Ensure this is up-to-date. This is where any physical correspondence from tax authorities will be sent.

- Bank Account Information: Specifically, your routing and account numbers if you wish to receive your refund via direct deposit. This is the fastest and most secure way to get your money back.

- Employer Identification Number (EIN): If you are self-employed with employees, or operate certain types of businesses, your EIN will be required.

Maintaining a secure, accessible record of these details ensures you can quickly populate the introductory sections of any tax software or provide them efficiently to a tax preparer.

Leveraging Your Previous Year’s Returns

Your prior year’s tax return is a goldmine of information, acting as a historical ledger of your financial life. It often contains data crucial for the current year’s filing and helps to establish continuity. Key elements to revisit include:

- Adjusted Gross Income (AGI): This figure is often referenced for eligibility for various credits, deductions, and even certain healthcare subsidies.

- Carryovers: Information like capital loss carryovers, passive activity loss carryovers, or charitable contribution carryovers from previous years directly impact your current tax situation. Without this historical context, you might miss out on valuable deductions.

- Depreciation Schedules: If you own rental properties or have a business with depreciable assets, the depreciation schedule from the previous year is essential to continue accurately calculating depreciation for the current year.

- Filing Status: While your status can change, last year’s return provides a baseline. Reviewing it can remind you of your default position and prompt you to consider if your circumstances (e.g., marriage, divorce, birth of a child) necessitate a change.

- Tax Preparer Information: If you used a professional last year, their details will be on the return, making it easy to reconnect or provide context to a new preparer.

Having a digital or physical copy of your previous year’s tax return readily available saves time and reduces the risk of overlooking important financial details. It serves as a benchmark and a checklist for consistency.

Decoding Your Income: A Guide to Financial Reporting Documents

The core of any tax return is your income. Various entities are legally obligated to report your earnings to the tax authorities and, crucially, to you. Collecting these documents is paramount to accurately declare all taxable income.

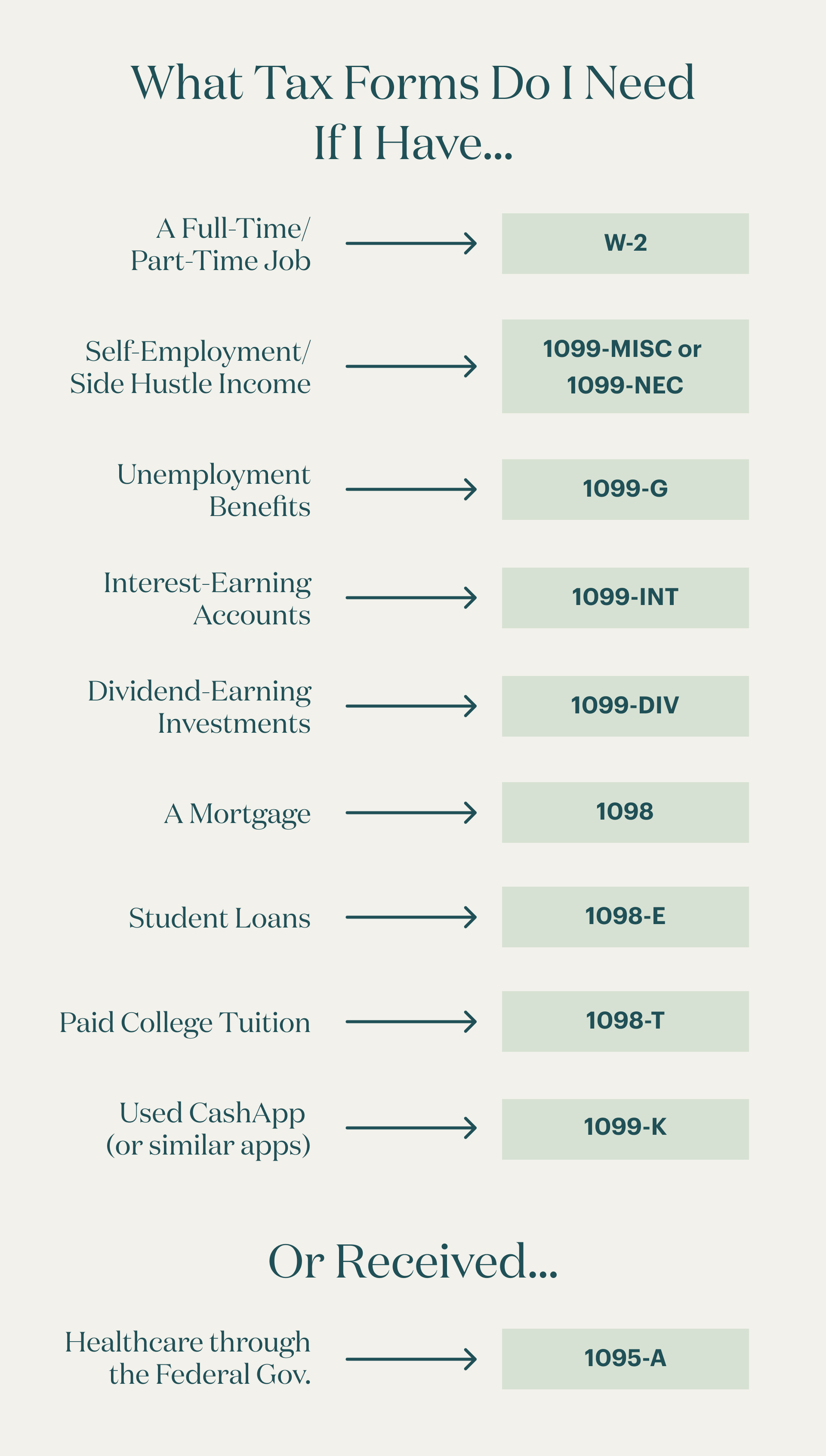

Employment Income: W-2s and Beyond

For most employed individuals, the W-2 Form is the cornerstone of income reporting. It summarizes your wages, tips, and other compensation, along with federal, state, and local taxes withheld. Ensure you receive a W-2 from every employer you had during the tax year. However, employment income can also encompass:

- Form W-2G: For certain gambling winnings.

- Tip Income Records: Even if not fully reported on a W-2, you are responsible for reporting all tip income.

- Stock Option Information: If you exercised stock options as part of your compensation package, documentation from your employer or broker is necessary to calculate the taxable benefit.

- Reimbursements: Certain non-taxable reimbursements might be listed on your W-2 for informational purposes, or you might need to track taxable reimbursements not included.

Carefully review each W-2 for accuracy. Any discrepancies should be addressed with your employer immediately to ensure corrections are made before filing.

Self-Employment and Gig Economy Earnings: The 1099 Series

The rise of the gig economy means an increasing number of individuals receive various 1099 forms instead of, or in addition to, W-2s. These forms report different types of non-employment income:

- Form 1099-NEC (Nonemployee Compensation): This form has replaced 1099-MISC for reporting payments of $600 or more to non-employees, typically independent contractors or freelancers.

- Form 1099-MISC (Miscellaneous Income): Now primarily used for reporting rents, royalties, prize winnings, and other miscellaneous payments of $600 or more.

- Form 1099-K (Payment Card and Third Party Network Transactions): Issued by payment processors (e.g., PayPal, Stripe, Square) if you meet certain thresholds for gross payments from payment card transactions or third-party payment networks. This is crucial for businesses and gig workers.

- Form 1099-G (Certain Government Payments): Reports unemployment compensation, state or local income tax refunds, or agricultural payments.

- Personal Records for Cash Earnings: If you received cash payments for services or goods that weren’t reported on a 1099, you are still legally obligated to report this income. Maintaining meticulous records of these transactions is essential.

For the self-employed, tracking gross income is just one part of the equation; accurate expense tracking is equally vital for determining net profit and reducing your tax liability.

Investment and Retirement Income Documentation

Your investments and retirement accounts generate various forms of income that are subject to tax. Keep an eye out for these documents from your financial institutions:

- Form 1099-DIV (Dividends and Distributions): Reports ordinary dividends, qualified dividends, capital gain distributions, and other distributions from stocks and mutual funds.

- Form 1099-INT (Interest Income): Reports interest earned from bank accounts, bonds, and other investments.

- Form 1099-B (Proceeds From Broker and Barter Exchange Transactions): Reports capital gains or losses from the sale of stocks, bonds, and other securities. This form often includes cost basis information, which is critical for calculating accurate gains/losses.

- Form 1099-R (Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.): Reports distributions from retirement accounts, including withdrawals from 401(k)s, IRAs, and pension plans. This form distinguishes between taxable and non-taxable portions of distributions.

- Schedule K-1 (Form 1065 or 1120-S): If you are a partner in a partnership or a shareholder in an S corporation, you’ll receive a K-1 detailing your share of the entity’s income, deductions, credits, and other items.

It’s imperative to consolidate all these investment-related documents, as overlooking even small amounts can lead to discrepancies with tax authorities.

Other Income Streams: Rental Properties, Alimony, and More

Beyond standard employment and investment income, other sources can contribute to your taxable income:

- Rental Property Income and Expenses: If you own rental properties, you’ll need detailed records of rent received, and all associated expenses (mortgage interest, property taxes, repairs, utilities, insurance, depreciation) to accurately report net rental income or loss on Schedule E.

- Alimony Received: For divorce agreements executed before January 1, 2019, alimony received is generally taxable income. For agreements entered into on or after that date, it is no longer considered taxable income at the federal level.

- Gambling Winnings (Form W-2G): As mentioned, significant winnings typically come with this form. Keep personal logs for smaller winnings and losses to potentially offset gains.

- Foreign Earned Income: If you live or work abroad, you’ll need records related to foreign income, foreign taxes paid, and eligibility for exclusions or credits (e.g., Form 2555 for Foreign Earned Income Exclusion).

Accurate reporting of all income sources, regardless of size or origin, is a cornerstone of tax compliance and avoids potential penalties.

Maximizing Your Savings: Identifying Deductions and Credits

Once all income is accounted for, the next crucial step is to identify opportunities to reduce your taxable income through deductions and directly lower your tax bill with credits. This is where strategic preparation can significantly impact your financial outcome.

Itemized Deductions vs. Standard Deduction

One of the first decisions for many taxpayers is whether to take the standard deduction or itemize.

- Standard Deduction: A fixed dollar amount that varies based on your filing status, age, and blindness. It simplifies tax preparation significantly. For many taxpayers, especially since the Tax Cuts and Jobs Act of 2017 significantly increased standard deduction amounts, this is the most beneficial option.

- Itemized Deductions (Schedule A): If the sum of your specific deductible expenses exceeds your standard deduction, you can itemize. Common itemized deductions include:

- Medical and Dental Expenses: Amounts exceeding a certain percentage of your AGI.

- State and Local Taxes (SALT): A cap of $10,000 applies to combined state and local income or sales taxes and property taxes.

- Home Mortgage Interest: Interest paid on home mortgage loans, up to certain limits.

- Charitable Contributions: Donations to qualified organizations.

- Casualty and Theft Losses: Limited to federally declared disaster areas.

Keeping meticulous records of all potential itemized deductions throughout the year is vital to make an informed decision come tax time.

Education-Related Expenses and Credits

Education can be a significant expense, but tax law often provides relief through deductions and credits:

- Form 1098-T (Tuition Statement): Issued by eligible educational institutions, this form reports qualified tuition and related expenses. It’s crucial for claiming education credits.

- American Opportunity Tax Credit (AOTC): A partially refundable credit for qualified education expenses for eligible students pursuing a degree or other recognized educational credential for the first four years of higher education.

- Lifetime Learning Credit (LLC): A nonrefundable credit for qualified education expenses for courses taken toward a college degree or to acquire job skills.

- Student Loan Interest Deduction: You can deduct up to $2,500 of student loan interest paid during the year, subject to income limitations. You’ll receive Form 1098-E from your loan servicer for this.

Thorough documentation of tuition payments, fees, and student loan interest is essential to claim these valuable benefits.

Dependent Care and Child-Related Credits

Families with children or dependents can often benefit from substantial tax credits:

- Child Tax Credit (CTC): A significant credit for each qualifying child. The maximum amount and refundability can vary based on income and specific tax years (e.g., changes introduced in the American Rescue Plan Act for 2021 filings). You’ll need SSNs for all claimed children.

- Credit for Other Dependents: A nonrefundable credit for dependents who do not qualify for the Child Tax Credit.

- Child and Dependent Care Credit: For expenses paid for the care of a qualifying child or dependent to allow you to work or look for work. You’ll need the provider’s name, address, and EIN or SSN.

These credits are often among the most impactful for families, making accurate dependent information and expense tracking critical.

Healthcare and Medical Expense Considerations

While the Affordable Care Act (ACA) introduced changes, some healthcare-related deductions and forms remain relevant:

- Form 1095-A, B, or C: These forms report your health coverage status. Form 1095-A (Health Insurance Marketplace Statement) is particularly important if you received subsidies (Premium Tax Credit) through the marketplace, as you’ll need to reconcile these on your tax return.

- Medical Expense Deduction: As noted under itemized deductions, you can deduct unreimbursed medical expenses exceeding a certain percentage of your AGI. Keep detailed records of all medical, dental, and vision expenses, including prescription costs, insurance premiums not paid pre-tax, and transportation to medical care.

- Health Savings Account (HSA) Contributions and Distributions (Form 5498-SA and 1099-SA): Contributions to an HSA are deductible, and qualified distributions are tax-free. These forms summarize your activity.

Understanding your health insurance situation and diligently tracking medical expenses can lead to significant savings.

Homeownership and Interest Deductions

Homeownership comes with several potential tax benefits:

- Form 1098 (Mortgage Interest Statement): Your mortgage lender will provide this form, reporting the mortgage interest you paid during the year, which is deductible on Schedule A. It also often includes real estate taxes and mortgage insurance premiums paid, which may also be deductible.

- Property Tax Records: In addition to what might be on Form 1098, keep records of all real estate taxes paid to local authorities.

- Points Paid on a Mortgage: If you paid “points” to obtain your mortgage, these can often be deducted over the life of the loan or, in some cases, in the year they were paid.

- Home Equity Loan Interest: Interest on home equity loans used to buy, build, or substantially improve your home can be deductible, subject to limits.

These deductions can substantially reduce the taxable income for homeowners.

Business Expenses for the Self-Employed

For freelancers, sole proprietors, and small business owners, tracking business expenses is paramount for accurate income calculation and tax reduction:

- Receipts and Invoices: For all business purchases, including office supplies, equipment, software, professional services, and travel.

- Mileage Logs: Detailed records of business-related mileage are essential for deducting vehicle expenses.

- Home Office Expenses: If you use a portion of your home exclusively and regularly for business, you may be able to deduct a portion of your rent, utilities, insurance, and depreciation.

- Advertising and Marketing Costs: Records of expenditures on promoting your business.

- Professional Development: Costs associated with courses, seminars, and certifications relevant to your business.

- Business Insurance Premiums: For liability, property, or professional insurance policies.

The distinction between personal and business expenses is crucial. Maintaining separate bank accounts and credit cards for your business can greatly simplify this process.

Beyond the Documents: Choosing Your Tax Preparation Method

Once you’ve meticulously gathered all your documents, the next decision is how you will actually prepare and file your return. The “what you need” extends to the tools and assistance that best fit your situation.

DIY Tax Software: Empowerment and Efficiency

For many individuals, especially those with straightforward tax situations, do-it-yourself tax software offers a cost-effective and efficient solution. These platforms guide you through the process step-by-step, flagging potential errors and suggesting deductions.

- Leading Software Options: Programs like TurboTax, H&R Block Tax Software, and TaxAct provide varying levels of support and features, from basic free versions for simple returns to advanced options for self-employed individuals and investors.

- Benefits: Convenience, control over your data, and instant feedback on your refund or tax due. Many offer audit support and guarantee accuracy.

- Considerations: Requires a basic understanding of your financial situation and comfort with technology. While user-friendly, complex scenarios might still be challenging without professional guidance.

Choosing the right software involves assessing your tax complexity, budget, and desired level of hands-on involvement.

The Professional Touch: When to Hire a Tax Preparer

For those with complex financial situations, significant life changes, or simply a desire for expert reassurance, hiring a tax professional is often the wisest choice.

- Who Benefits: Individuals with multiple income streams, complex investments, business ownership (especially corporations or partnerships), those who’ve experienced major life events (marriage, divorce, home purchase/sale), or anyone facing an audit.

- Types of Professionals: Enrolled Agents (EAs), Certified Public Accountants (CPAs), and tax attorneys. Each has different qualifications and specializations.

- Benefits: Expertise in tax law, strategic advice to optimize your return, representation during an audit, and peace of mind. A good preparer can identify deductions and credits you might miss.

- Considerations: Cost is generally higher than DIY software. It’s crucial to choose a reputable professional with appropriate credentials and experience.

When seeking a professional, inquire about their fees, experience with your specific tax situation, and their process for handling client information and communication.

Free Tax Filing Options: Eligibility and Access

Various initiatives aim to make tax filing accessible to everyone, particularly those with lower incomes or specific circumstances.

- IRS Free File Program: A partnership between the IRS and leading tax software companies, offering free federal tax preparation and e-filing for taxpayers whose Adjusted Gross Income (AGI) is below a certain threshold (which changes annually). Some partners also offer free state filing.

- Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE): These IRS-sponsored programs offer free tax preparation help from certified volunteers. VITA generally assists people who make $60,000 or less, persons with disabilities, and limited English-speaking taxpayers. TCE provides free tax help to all taxpayers, particularly those who are 60 years of age and older, specializing in pension and retirement-related issues.

- Free Fillable Forms: Provided directly by the IRS, these are electronic versions of paper IRS forms. They offer no guidance, calculations, or state tax preparation, making them suitable only for those extremely confident in their ability to prepare their own taxes.

These free resources can be invaluable for eligible taxpayers, ensuring they can fulfill their tax obligations without incurring preparation costs.

The Importance of Diligent Record-Keeping and Future Planning

Ultimately, the ease and accuracy of your tax filing heavily rely on how well you’ve managed your financial records throughout the year. Effective record-keeping isn’t just for tax season; it’s a fundamental aspect of sound financial management.

Organizing Your Financial Life Year-Round

Instead of a frantic scramble in January or February, adopt a proactive approach to document management:

- Dedicated Tax Folder: Whether physical or digital, create a specific location for all tax-related documents as they arrive. This could be a physical accordion file or a cloud-based folder.

- Categorize and Label: As you receive income statements, expense receipts, or investment documents, categorize them immediately. Use clear labels like “W-2,” “1099-NEC,” “Medical Receipts,” “Charitable Donations,” etc.

- Digital Copies: Scan physical receipts and documents to create digital backups. Cloud storage services offer secure and accessible options. This protects against loss and provides easy retrieval.

- Separate Business Finances: If self-employed, maintaining distinct bank accounts and credit cards for business transactions simplifies tracking income and expenses.

- Monthly/Quarterly Review: Take time throughout the year, perhaps monthly or quarterly, to review your financial statements and reconcile your records. This prevents last-minute surprises and ensures completeness.

This year-round diligence transforms tax preparation from a burdensome task into a straightforward data compilation exercise.

Understanding Retention Periods for Tax Records

Knowing how long to keep your tax documents is crucial for both compliance and future reference. The IRS generally recommends keeping records for three years from the date you filed your original return or two years from the date you paid the tax, whichever is later, if you owe additional tax. However, specific situations warrant longer retention:

- Seven Years: If you filed a claim for a loss from worthless securities or bad debt deduction.

- Six Years: If you do not report income that you should report, and it is more than 25% of the gross income shown on your return.

- Indefinitely: Records relating to property (e.g., purchase and improvement records for your home, rental properties, or business assets) should be kept indefinitely, or at least until a few years after you sell or dispose of the property. This is vital for calculating gain or loss.

- Indefinitely: Copies of your actual filed tax returns should ideally be kept permanently.

These guidelines protect you in case of an audit and provide the necessary history for future financial decisions.

Proactive Strategies for Future Tax Seasons

Leverage your current tax filing experience to inform and improve future preparation:

- Post-Filing Review: Once your return is complete, take a moment to understand your financial picture. Did you pay too much tax? Did you receive a surprisingly large refund (suggesting too much withholding)?

- Adjust Withholding/Estimated Payments: Based on your current tax situation, adjust your W-4 with your employer or modify your estimated tax payments if you are self-employed. The goal is to avoid significant underpayment penalties or tying up too much of your money in an interest-free loan to the government.

- Consult a Financial Advisor: If your situation is complex or you have specific financial goals, a professional can provide tailored advice on tax-efficient strategies for investments, retirement planning, and business operations.

- Stay Informed: Tax laws change. Subscribing to financial news, reputable tax blogs, or using a tax professional can keep you abreast of relevant updates.

By embracing diligent record-keeping and proactive planning, you can transform tax season from an annual dread into a well-managed component of your overall financial strategy, ensuring compliance and optimizing your financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.