When you apply for a mortgage, your bank statements serve as the ultimate narrative of your financial life. While credit scores provide a snapshot of your debt repayment history, your bank statements offer a high-definition video of your spending habits, cash flow, and financial discipline. To a mortgage broker, these documents are not just bureaucratic requirements; they are critical risk-assessment tools used to determine whether you can comfortably handle the long-term commitment of a home loan. Understanding what brokers scrutinize will help you prepare your finances and prevent last-minute hurdles in your property purchase.

The Pillars of Financial Stability: Income and Deposits

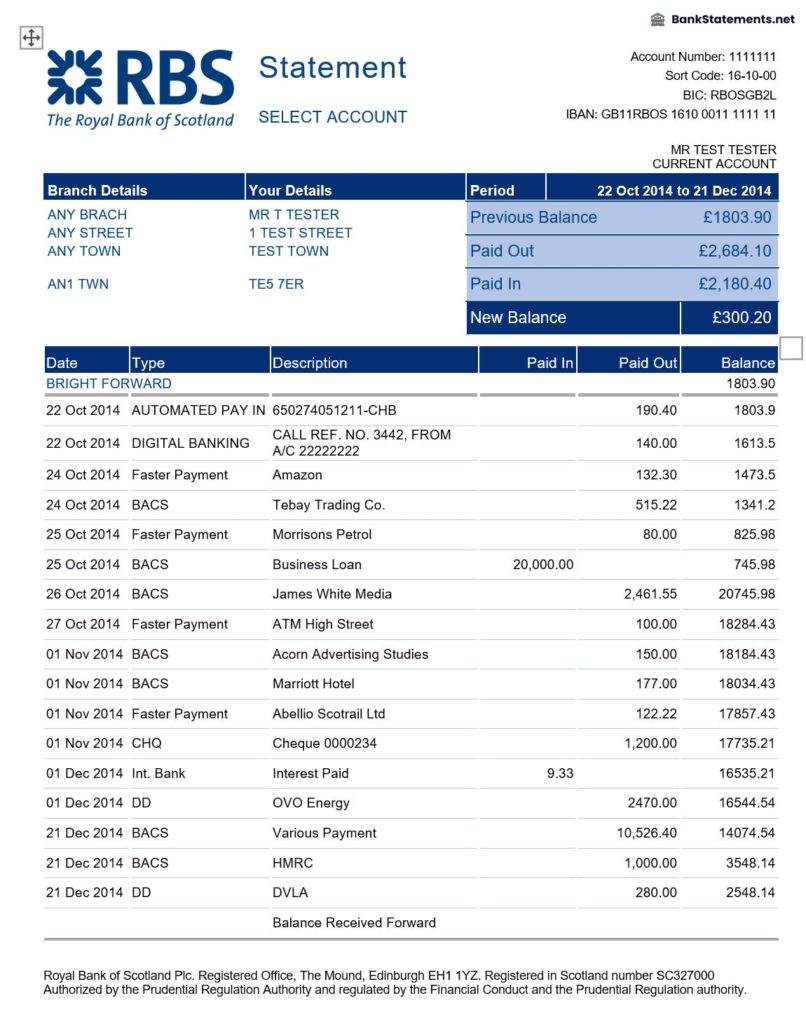

The primary reason a broker requests 3 to 6 months of bank statements is to verify the legitimacy and consistency of your income. They want to see that your lifestyle is supported by verifiable earnings rather than a web of complex, unexplained transfers.

Verifying Regular Income

Brokers cross-reference your bank statements with your pay stubs and tax returns. They are looking for recurring deposits that match your employer’s payroll schedule. If your income fluctuates, such as for commission-based employees or freelancers, brokers look for a consistent average over time. Any large, unexplained deposit can trigger an inquiry; if you deposit a significant amount of cash that isn’t tied to your salary, you will likely be required to provide a paper trail, such as a gift letter or evidence of the sale of a personal asset.

Scrutinizing “Large Deposits”

In the mortgage industry, a “large deposit” is typically defined as anything exceeding 25% of your total monthly qualifying income. Brokers are mandated by anti-money laundering (AML) regulations to source these funds. If you move money between your own accounts—such as transferring savings from a high-yield account to a checking account to prepare for a down payment—ensure you keep records of both sides of the transaction. Avoid depositing cash under your mattress or from undocumented side jobs into your account in the weeks leading up to your application, as these “unverifiable” funds may be excluded from your down payment calculation entirely.

Evaluating Spending Habits and Liability Management

While income shows what you make, your spending habits reveal what you keep. Brokers analyze your outflow to ensure you have enough residual income to cover the new mortgage payment on top of your existing financial obligations.

Identifying Recurring Debts

Bank statements are the most effective way for a lender to catch “hidden” debts that might not appear on your formal credit report. If your statement shows recurring monthly payments to a private lender, a car lease, or a recurring subscription service that functions as a loan, the broker must account for these as liabilities. If you are paying off a debt that isn’t on your credit report, the broker may recalculate your Debt-to-Income (DTI) ratio, which can inadvertently lower the maximum loan amount you qualify for.

Monitoring Lifestyle Expenses

Brokers aren’t typically judging your taste in coffee or your shopping habits, but they are looking for signs of financial distress. Excessive overdraft fees, non-sufficient funds (NSF) charges, or a pattern of living beyond your means are major red flags. An NSF fee suggests that you are managing your cash flow poorly, which translates to a higher risk of default in the eyes of an underwriter. If your statements consistently show that you are spending every dollar you earn, the lender may question your ability to absorb the unexpected costs of homeownership, such as property repairs or tax fluctuations.

The “Paper Trail” Requirement for Transfers and Assets

The golden rule of mortgage applications is that every dollar must be accounted for. When you move money around, you create a complex map that the broker must decode.

Internal Transfers

It is standard practice to move money into a central account for the closing costs. However, moving money between five different accounts creates five different sets of statements that must be reconciled. If possible, consolidate your funds into one primary account at least 60 days before applying for a mortgage. This minimizes the amount of documentation required and reduces the chances of an underwriter flagging a “missing link” in your funding chain.

Gift Funds and Secondary Support

If your down payment includes gifts from family members, there is a specific protocol for documenting these. A gift letter alone is often insufficient. A broker will look for the deposit of the gift funds into your account and must be able to trace those funds back to the donor. They will want to see the donor’s transfer receipt or a copy of the cleared check. If you receive a large gift, refrain from depositing it as cash. Always ensure the transfer is electronic or via check to create a clean, traceable audit trail.

Optimizing Your Statements Before You Apply

If you know you are planning to apply for a mortgage in the coming months, your preparation should begin long before you submit the application. Strategic account management can make your file significantly more attractive to lenders.

The 60-Day “Cooling Off” Period

Most underwriters request the most recent two or three months of statements. This means the activity occurring today will be scrutinized during the underwriting process. During the 60 days leading up to your application, avoid making any large, unusual purchases or moving large sums of money. If you need to make a major purchase—like buying new furniture or a vehicle—do it after the loan has closed. Financing a large purchase immediately before or during the application process can spike your DTI ratio and potentially disqualify you.

Clean Up Your “Optics”

While a broker is looking for hard data, the presentation of your statements matters. If your account is cluttered with hundreds of small automated debits for digital games, low-cost subscriptions, or daily micro-transactions, it makes the task of auditing your account more difficult and time-consuming. While you don’t need to change your lifestyle entirely, keeping your primary account clean and organized demonstrates financial maturity. Ensure that your statements are clearly labeled, that your name and account number are visible on every page, and that you have removed any unnecessary “noise” from your financial tracking.

Proactive Documentation

The best way to expedite the underwriting process is to be proactive. If you see a large deposit or an unusual transaction on your statement, do not wait for the broker to ask for an explanation. Prepare an “explanation letter” and attach the relevant documentation—such as a receipt, a bill of sale, or a transfer confirmation—immediately. By providing the answer before the question is asked, you demonstrate a level of organization that can move your file to the front of the queue.

Final Thoughts: Transparency is Key

The scrutiny of your bank statements is not intended to be an invasion of privacy; it is a necessary part of the lending process designed to protect both the bank and the borrower. By understanding that brokers are looking for consistency, a clear source of funds, and evidence of responsible debt management, you can approach the process with confidence. When you treat your bank statements with the same care as your tax returns, you eliminate the uncertainty that causes most mortgage applications to stall. Remember, the goal of the underwriter is to approve your loan; by providing clear, organized, and transparent financial history, you make it easy for them to say “yes.”

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.